Construction Activity In The Us South Jumped To Life At The Beginning Of

April, Sending Lumber Prices Slightly Higher.

Important regions like Texas and California came in to the market with

volume buys. Lumber manufacturers were more focussed on booking orders than

on raising prices. As such, sawmill order files stretched out toward the end

of April.

Transportation was more of a headache than even the previous week; as the

collision of jumping freight rates and competition from seasonal items made

sourcing rail cars and trucks difficult. Operators spent more time chasing

down deliveries than making sales.

Prices continue to hover nicely to between levels at the same time last year

and in 2024, providing industry good stability and ability to plan.

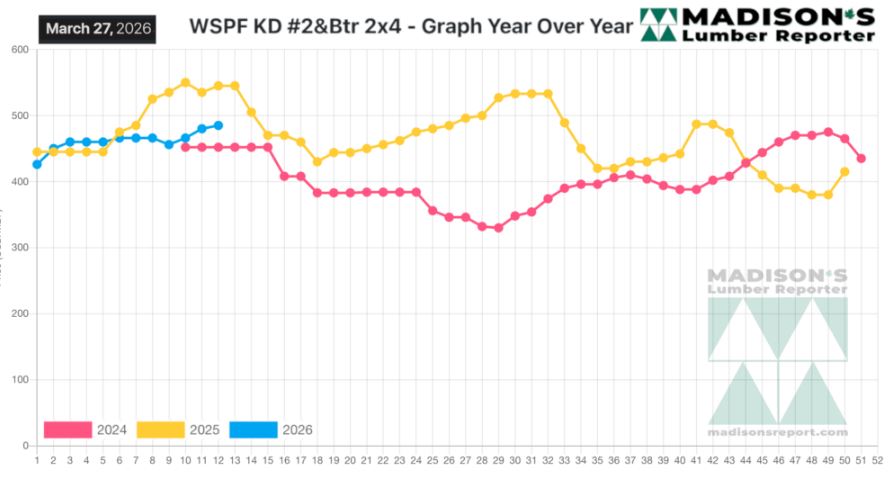

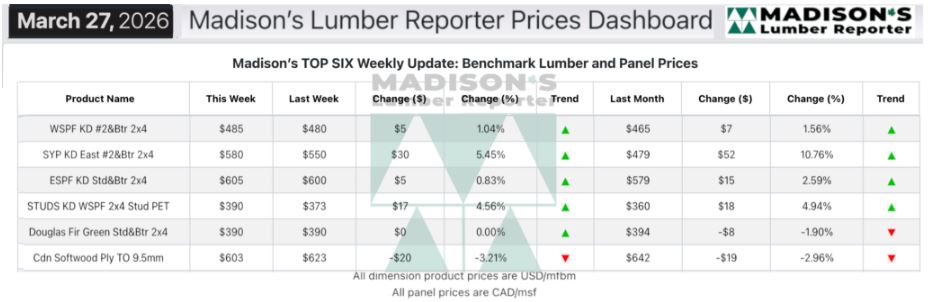

In the week ending April 3, 2026 the price of Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was US$490 mfbm, which was up +$5, or +1%, from the previous

week when it was $485, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.

That week’s price was up +$18, or +4%, from one month ago when it was $472.

Compared To The Same Week Last Year, When It Was Us$545 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending April 3, 2026

Was Down -$55, Or -10%.

Compared To Two Years Ago When It Was $452, That Week’S Price Was Up +$28,

Or +6%.

It was a a mix of contemplative digestion on this holiday-shortened

week, while Southern Yellow Pine prices continued to show strength. The

hemlock/fir complex finally joined the party.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Sellers of Western-SPF in the US were inundated with orders and inquiry,

such that they just had to focus on covering what demand they could.

Improving spring weather fully activated construction in Texas, and started

to percolate into the Central and Northern states.

Limited mill-availability continued to be exposed by even small jumps in

demand as reduced supply among secondary suppliers surfaced.

Buyers of Western-SPF in Canada stepped back to evaluate their positions

heading into the Easter holiday long weekend break.

Demand remained seasonally subpar as the calendar turned to April.

Secondary suppliers showed adequate inventory levels and a willingness to

negotiate.

Canadian sawmills in the West maintained order files at around two- to

three-weeks.

All regions were affected by tightening truck supply and soaring freight

rates.

Customers of Eastern-SPF showed how underbought they were by calling back

incessantly about where their latest order was in transit.

Suppliers of Southern Yellow Pine tried to fulfill orders amid a rising

market and severe ongoing freight challenges.

In the US northeast, Douglas-fir suppliers boosted their asking prices as

sawmills moved order files into late-April.

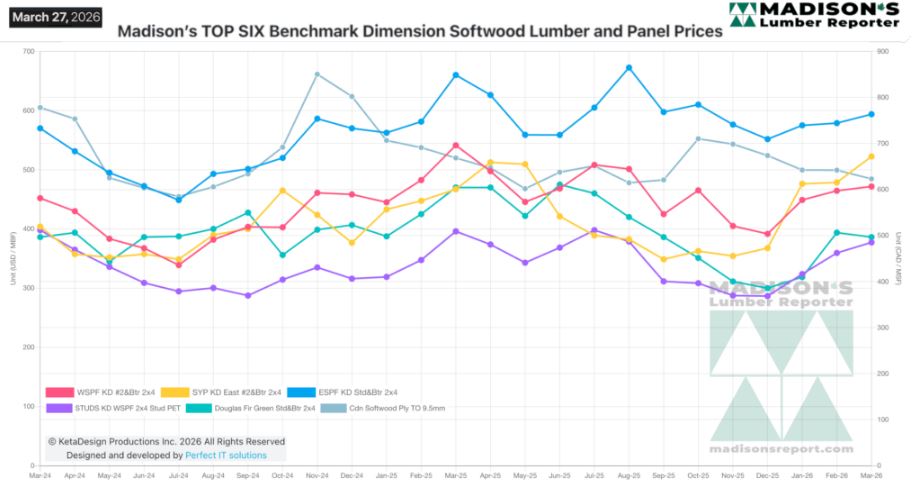

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: