Due To Ongoing Harsh Winter Weather, February Drew To A Close With Logistics

Issues Still A Top Priority.

North American softwood lumber buyers and sellers alike spent time chasing

down wood on the way somewhere throughout the supply chain. While rail cars

and trucks became more available, orders continued to take longer to

actually arrive than is usual.

Overall lumber supply was weak as customers still were reluctant to increase

inventories, not wanting to get caught if prices fell.

Altogether, for the first two months of this year, the price trend line for

most items was quite even compared to the past two years.

This offers a good stability for both sawmills and builders to make their

plans once spring building season actually arrives.

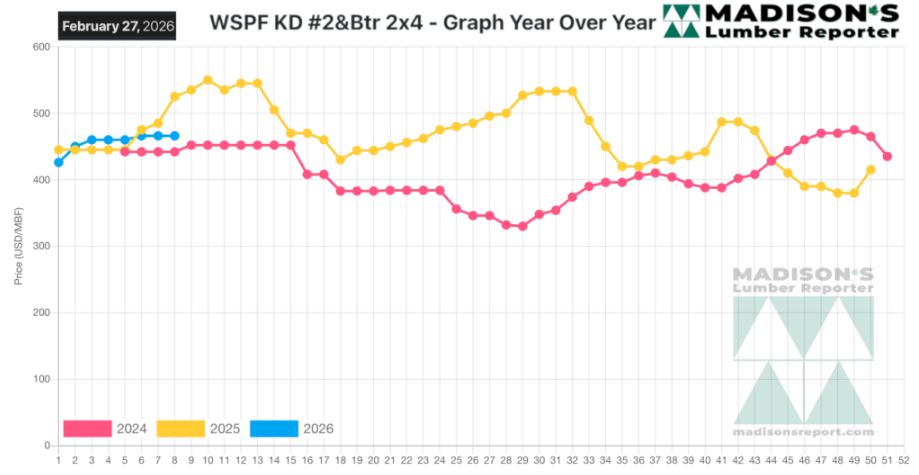

In the week ending February 27, 2026, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$466 mfbm. This was

flat from the previous week when it was $466, said weekly forest products

industry price guide newsletter Madison’s Lumber Reporter.

That week’s price was up +$17, or +4%, from one month ago when it was $449.

Compared To The Same Week Last Year, When It Was Us$525 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending February 27,

2026 Was Down -$59, Or -11%.

Compared To Two Years Ago When It Was $442, That Week’S Price Was Up +$24,

Or +5%.

Most commodity prices were largely flat as sawmills hoped to lean on

order files until the weather breaks and demand presumably improves.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

An increasingly frequent topic of conversation for sellers of Western-SPF in

the US was the overall lack of supply in the pipeline.

Several sources noted how tight Canadian supply was.

Inconsistent product mixes were evident, with scant availability of low

grade and industrial items while supply of mid- and high-grade offerings

were ample.

Buyers of Canadian Western-SPF kept their inventories tight as they still

felt uncertain about the direction of the market.

Demand for Eastern-SPF weakened further as month-end approached and snowy

weather continued to batter the region.

Sawmills in the East were not aggressively looking to move significant

volumes.

Transportation issues abounded, as dealers could only offer loose

guesstimates about delivery timelines.

The recent drop-off in Southern Yellow Pine demand and takeaway resulted in

wood steadily piling up in sawmill and distributor yards.

Regardless, SYP sellers expected to see a significant spate of spring buying

from treaters before long.

Eastern Stocking Wholesalers in the tri-state area were united in their

condemnation of ongoing harsh winter weather.

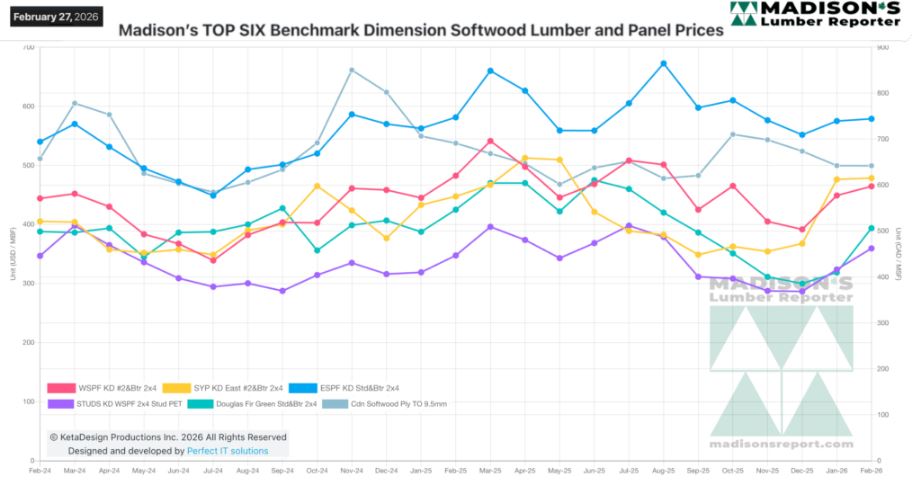

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: