Into The Middle Of February Most Lumber Industry Players Were Focussed On

Receiving Wood Already Ordered.

Sawmills reported muted demand for new sales, as traders were occupied with

logistics and supply chain; getting solid wood products actually delivered.

As such, prices remained quite level over the previous week. Customers who

were hunting around for the best deals tried to push back on sellers with

counter-offers. It seemed like a situation of who would blink first.

Mills protected their existing order files of barely two weeks by agreeing

to strategic sales only. Ongoing curtailments and reduced production volumes

bore out this effort, as the actual field inventories continued quite

depleted.

There was more time spent by both customers and suppliers on sourcing trucks

and rail cars than on booking new orders.

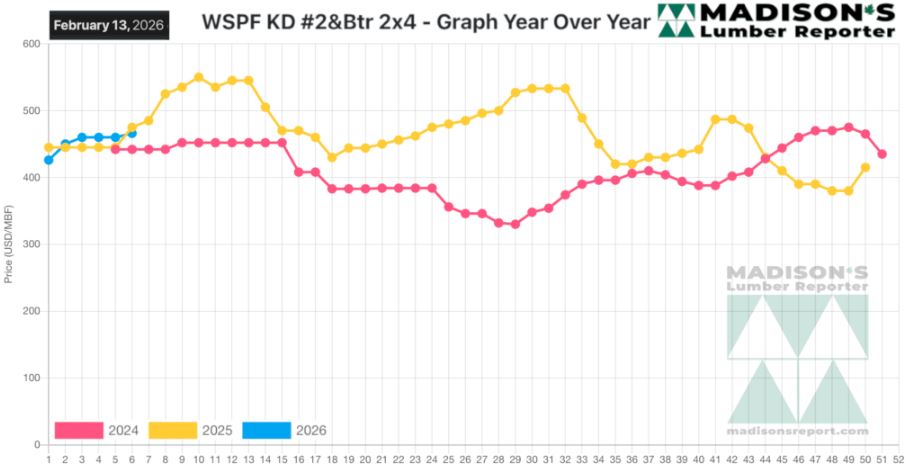

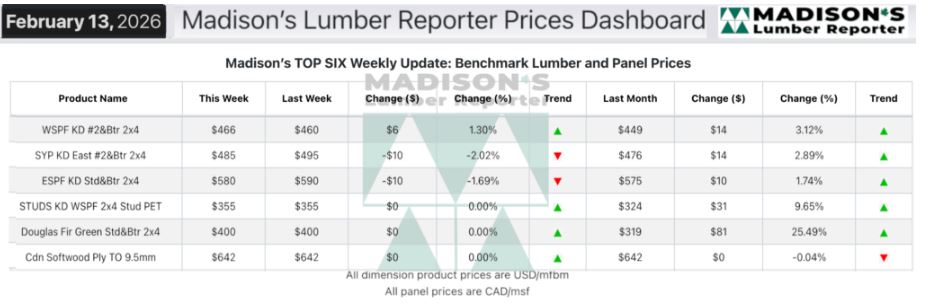

In the week ending February 20, 2026 the price of Western Spruce-Pine-Fir

2×4 #2&Btr KD (RL) was US$466 mfbm, which was flat from the previous week

when it was $466, said weekly forest products industry price guide

newsletter Madison’s Lumber Reporter.

That week’s price was up +$17, or +4%, from one month ago when it was $449.

Compared To The Same Week Last Year, When It Was Us$485 Mfbm, The Price Of

Western Spruce-Pine-Fir 2×4 #2&Btr Kd (Rl) For The Week Ending February 20,

2026 Was Down -$19, Or -4%.

Compared To Two Years Ago When It Was $442, That Week’S Price Was Up +$24,

Or +5%.

North American sawmills maintained firm pricing and decent order

files, while buyers digested their current positions and pondered their next

moves.

KEY TAKE-AWAYS:

KEY TAKE-AWAYS:

Some Western-SPF traders in the US were discouraged by weak buyer

activity, hoped spring would bring better bustle their way.

Producers maintained extended order files and firm pricing as they tried to

out-wait purchasers and force them to blink first.

The supply-demand balance for Western-SPF sellers in Canada appeared to be

even, on the surface.

Overall activity in Eastern-SPF continued dampened by ongoing and

far-reaching effects of severe winter weather.

Sawmills in the East continued to show limited supply of low grade material

as demand for those items gained ground.

Prices of Southern Yellow Pine entered a sideways grind amid retreating

demand.

Mills in the US South showed more abundant material on their lists in

certain grades and widths than in previous weeks.

For stocking wholesalers on the US Eastern Seaboard, buyers and sellers

alike were in tough trying to manage orders and deliveries.

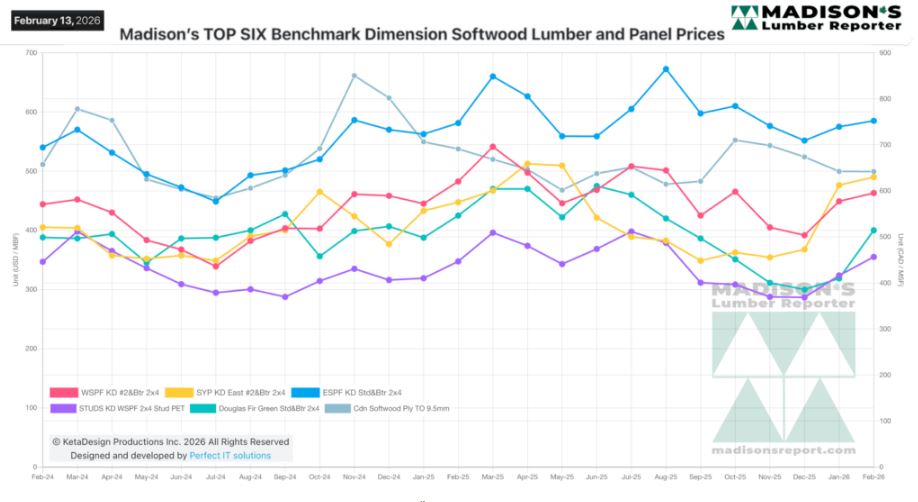

MADISON’S BENCHMARK TOP-SIX SOFTWOOD LUMBER AND PANEL PRICES: MONTHLY

AVERAGES

Source: madisonsreport.com

More Reports: