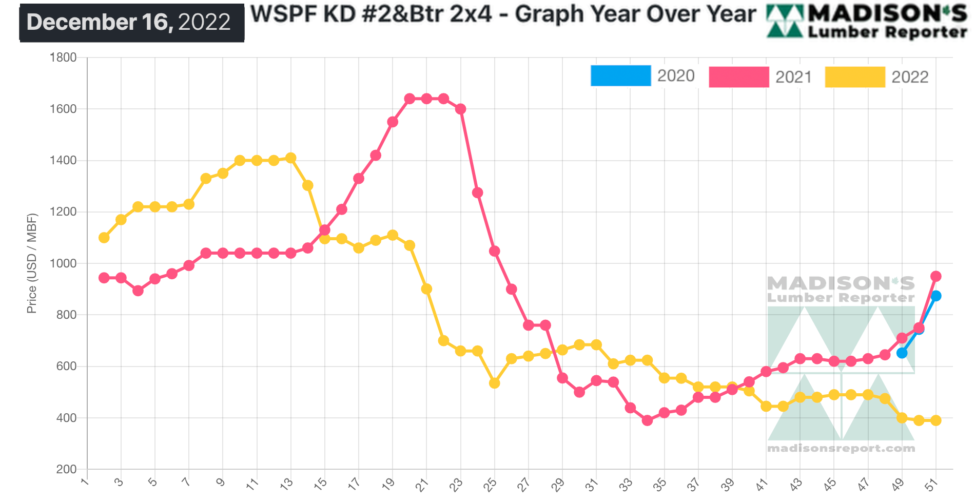

This year ended with lumber prices wavering around what can be considered

the “new normal”. The unprecedented volatility of the previous two years

does seem to be behind us. For the second half of 2022, the price of

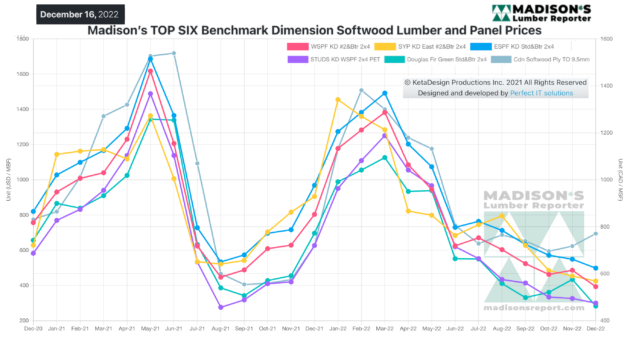

benchmark softwood lumber item Western Spruce-Pine-Fir KD 2×4 #2&Btr ranged

between US$630 and US$390 mfbm, providing an indication of where the future

seasonal price cycle will be. No one thought that these prices would stay at

the incredible high of US$1,600 mfbm in spring 2021; however folks should be

aware that the previous 10-year low of US$200 mfbm is equally unlikely. This

is because cost-of-production has changed completely, essentially doubling,

across the continent.

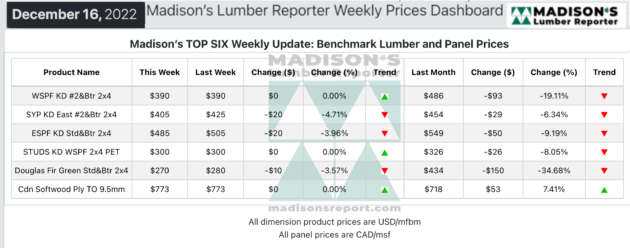

In the week ending December 15, 2022, the price of benchmark softwood lumber

item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$390 mfbm, which is

flat from the previous week. This is down by $96, or 20 per cent, from one

month ago when it was $486.

An embargo by CN Rail in the Vancouver, B.C., region has apparently resulted

in major service delays, putting more pressure on trucking availability. For

now, low transit volumes helped to downplay this development’s effect on the

transportation sector.

“

Suppliers and buyers alike quietly wound down their activity as the

Christmas holiday break approached.” — Madison’s Lumber Reporter

Demand for Western S-P-F commodities in the United States closed out the

year not with a bang, but with a whimper. Buyers remained silent, electing

to ride their lean inventories into 2023, making virtually no participation.

Most prices stayed at the previous week’s levels, with a couple more

commonly-traded items hovering on either side of up-or-down. Producers noted

dampened inquiry and continued to gear down operations ahead of scheduled

shutdowns for the holiday break. Reports indicated sawmill order files

anywhere from prompt to the week of January 2nd.

The curtailment announcement from a large B.C. producer the previous week

generated no momentum of Western S-P-F sales. Buyers sat on their hands,

barely even bothering to short-cover amid languishing demand and deepening

winter weather. Sawmills held most of their asking prices static, with a few

R/L bread-and-butter narrows trading on either side of last week’s levels.

With the majority of buyers fixing to close out the year with

nearly-depleted inventories, many suppliers expressed optimism that 2023

will start off strong. Time will tell. Meanwhile, producers did some

housekeeping to prepare for holiday shutdowns, with offer lists getting

slimmer by the day.

“

Demand for Western S-P-F studs dragged along according to suppliers in

Western Canada. Buyers remained cautious, feeling no pressure to cover any

more than short-term needs despite their depleted inventories. For their

part, producers held their asking prices at the previous week’s levels as

they continued to wind down operations in advance of the approaching Holiday

break. Prompt offerings on more plentiful trims like 2×4- and 2×6-8’s were

slim, but demand was correspondingly slow. Stud mill order files on tighter

items such as 2×4- and 2×6-9’s were up to three weeks out. ” — Madison’s

Lumber Reporter

Compared to the same week last year, when it was US$950 mfbm, the price of

Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending December 16,

was down by $560, or 59 per cent. Compared to two years ago when it was

$874, that week’s price is down by $484, or 55 per cent.

More Reports: