|

Lumber and panel market weekly report ----

Week 43, 2022 |

|

By Madison's Lumber Reporter

In mid-November the annual North American

Wholesale Lumbermen’s Association gathering took

many traders away from their desks to hob-nob

with their colleagues, often determining between

themselves the condition for lumber sales to the

end of the year. As such, sales were slow but

somewhat consistent, and prices remained steady.

True winter weather came on in many parts of

North America, causing the usual stall to

construction activity and indeed sawmill

manufacturing volumes. The past two years ended

with some serious surprises, which propped up

prices significantly at an unusual time of year.

Will something similar happen this year? Only

time will tell.

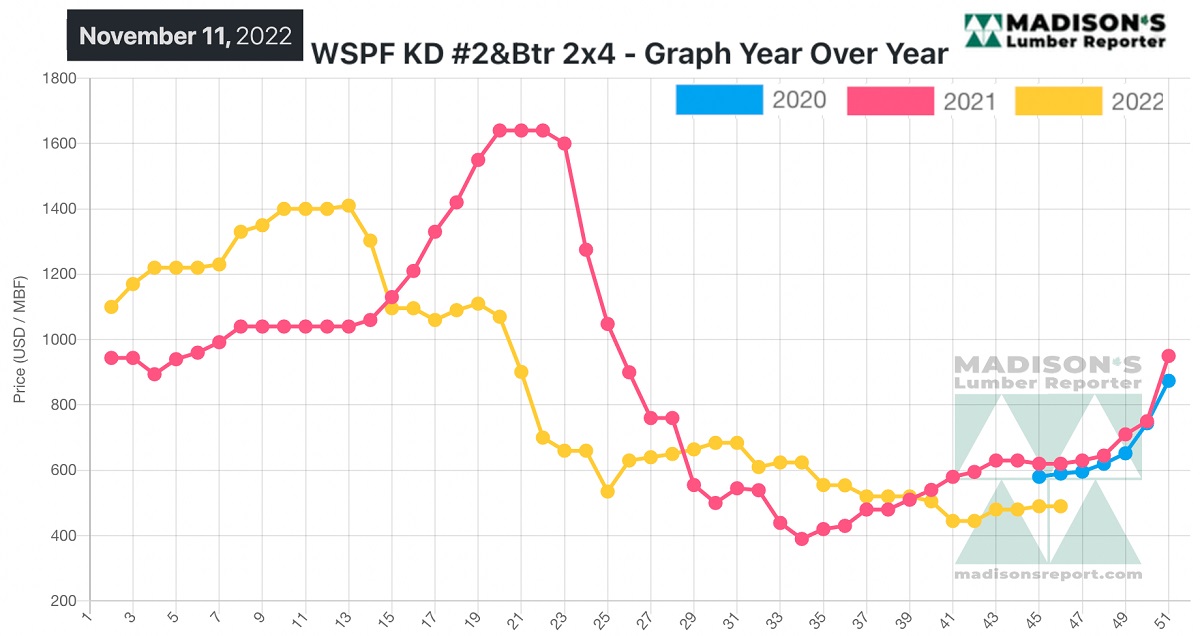

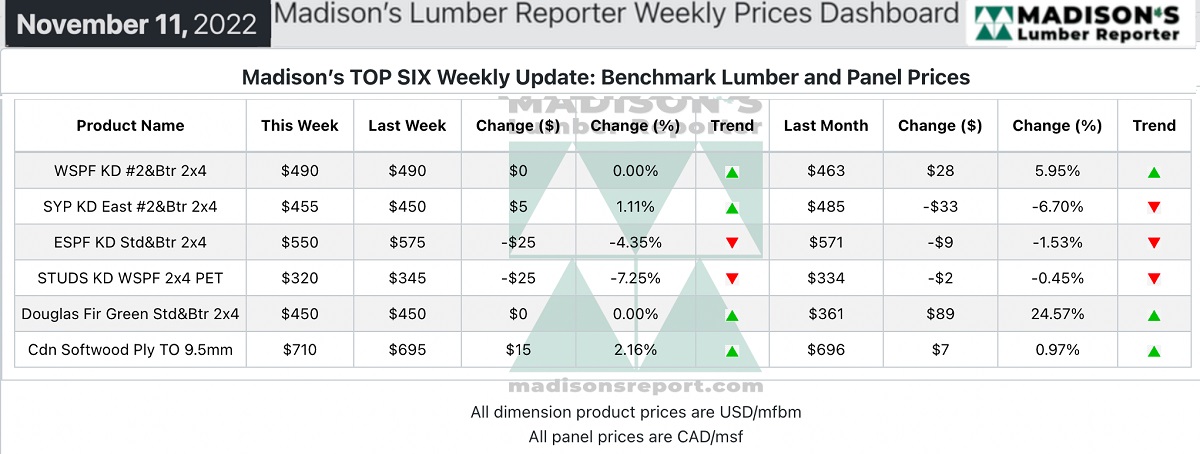

Remaining flat from the previous week, in the

week ending November 11, the price of benchmark

softwood lumber item Western Spruce-Pine-Fir 2×4

#2&Btr KD (RL) was again US$490 mfbm. This is up

by $28, or 6.0 per cent, from one month ago when

it was $463.

Adding to the quietude was a significant

contingent of players absconding to Arizona to

hobnob at the North American Wholesale

Lumbermen’s Association Trader’s Market.

“Overall demand took another step back this week

as frigid weather patterns descended and many

players absconded to Phoenix, AZ, for the NAWLA

Trader’s Market.” — Madison’s Lumber Reporter

Lacklustere demand for Western S-P-F lumber and

studs diminished further as the week wore on,

according to traders in the United States.

Buyers anticipated a softening market and held

off, waiting to see where numbers would land

after the NAWLA Trader’s Market wrapped up. The

U.S. mid-term elections provided another

distraction from the lumber game. Field

inventories remained extremely low, and sawmills

showed limited availability of most dimension

items and nine-foot studs. One veteran trader

was convinced the market was sneaky strong due

to that combination of scant supply and depleted

inventories. Sawmill order files were into the

week of November 21st.

Suppliers of Western S-P-F in Canada described a

market that was subdued by a sudden and fierce

snap of cold weather across the Western

provinces. Buyers were already showing next to

no urgency as the previous week wrapped up, and

demand tapered off even further. Distributers

reported meagre takeaway. Pickup and delivery

timelines suffered for the first time in awhile

as winter weather affected road conditions and

rail service readiness.

“ Demand for Western S-P-F studs was

unremarkable as buyers scurried to the sidelines

in response to inclement weather. Most appeared

to be waiting until after the NAWLA Trader’s

Market to make any decisions about short-term

coverage. Weak demand barely kept stud mills

ahead of showing prompt availability, with order

files in the range of two- or three-weeks. Those

buyers who were still active leaned on the

distribution network, where they reported decent

delivery times even as weather conditions

worsened.” — Madison’s Lumber Reporter

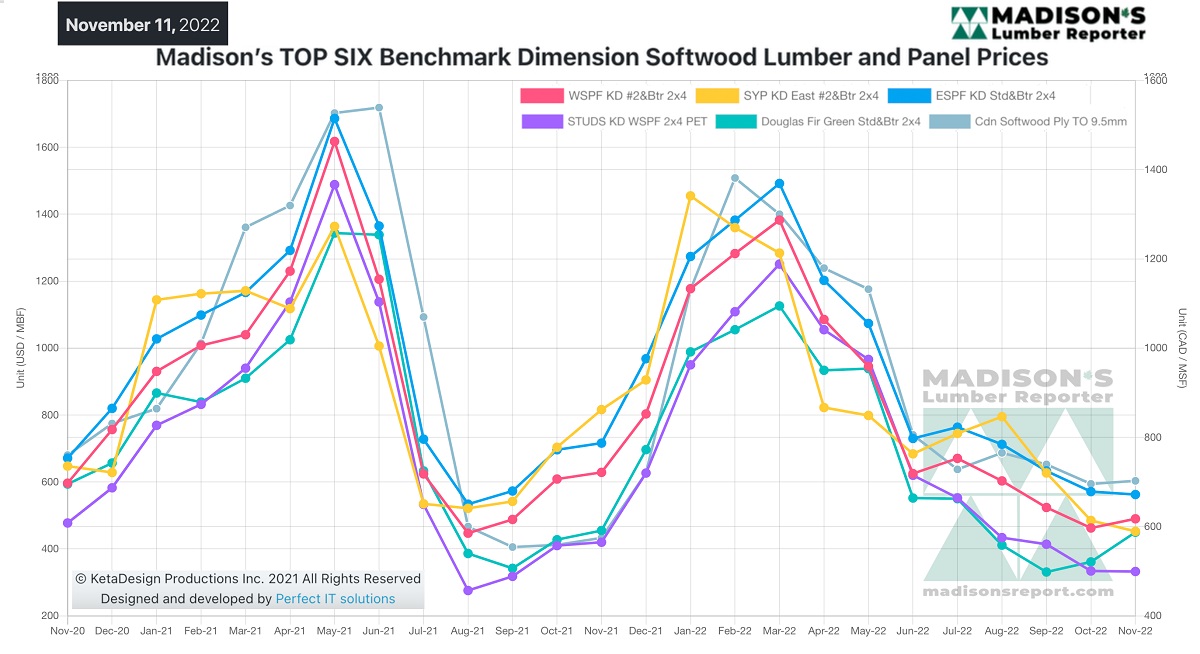

Madison’s Benchmark Top-Six Softwood Lumber and Panel

Prices: Monthly Averages

Compared to the same week last year, when it was US$620 mfbm, the price

of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) for the week ending

November 11, was down by $130, or 21 per cent. Compared to two years ago

when it was $590, that week’s price is down by $100, or 17 per cent.

-

U.S. & Canada softwood and panel markets - week

42 2022 (Nov

15

2022)

-

U.S. & Canada softwood and panel markets - week

41 2022 (Nov

08,

2022)

-

U.S. & Canada softwood and panel markets - week

40 2022 (Nov

02,

2022)

-

U.S. & Canada softwood and panel markets - week

39 2022 (Oct

11,

2022)

-

U.S. & Canada softwood and panel markets - week 38 2022 (Oct

04,

2022)

-

U.S. & Canada softwood and panel markets - week 37 2022 (Sep

28,

2022)

-

U.S. & Canada softwood and panel markets - week 36 2022 (Sep

20,

2022)

-

U.S. & Canada softwood and panel markets - week 35 2022 (Sep

13,

2022)

-

U.S. & Canada softwood and panel markets - week 34 2022 (Sep

06,

2022)

-

U.S. & Canada softwood and panel markets - week 33 2022 (Aug

30,

2022)

-

U.S. & Canada softwood and panel markets - week 32 2022 (Aug

23,

2022)

-

U.S. & Canada softwood and panel markets - week 31 2022 (Aug

16,

2022)

-

U.S. & Canada softwood and panel markets - week 30 2022 (Aug

09,

2022)

-

U.S. & Canada softwood and panel markets - week 29 2022 (Aug

02,

2022)

-

U.S. & Canada softwood and panel markets - week 28 2022 (Jul

26,

2022)

-

U.S. & Canada softwood and panel markets - week 27 2022 (Jul

19,

2022)

-

U.S. & Canada softwood and panel markets - week 26 2022 (Jul

12,

2022)

-

U.S. & Canada softwood and panel markets - week 25 2022 (Jul

05,

2022)

-

U.S. & Canada softwood and panel markets - week 24 2022 (Jun

29,

2022)

-

U.S. & Canada softwood and panel markets - week 23 2022 (Jun

22,

2022)

-

U.S. & Canada softwood and panel markets - week 22 2022 (Jun

15,

2022)

-

U.S. & Canada softwood and panel markets - week 21 2022 (Jun

08,

2022)

-

U.S. & Canada softwood and panel markets - week 20 2022 (Jun

01,

2022)

-

U.S. & Canada softwood and panel markets - week 19 2022 (May

25,

2022)

-

U.S. & Canada softwood and panel markets - week 18 2022 (May

18,

2022)

-

U.S. & Canada softwood and panel markets - week 17 2022 (May

11,

2022)

-

U.S. & Canada softwood and panel markets - week 16 2022 (May

04,

2022)

-

U.S. & Canada softwood and panel markets - week 15 2022 (Apr

26,

2022)

-

U.S. & Canada softwood and panel markets - week 14 2022 (Apr

19,

2022)

-

U.S. & Canada softwood and panel markets - week 13 2022 (Apr

12,

2022)

-

U.S. & Canada softwood and panel markets - week 12 2022 (Apr

05,

2022)

-

U.S. & Canada softwood and panel markets - week 11 2022 (Mar

29,

2022)

-

U.S. & Canada softwood and panel markets - week 10 2022 (Mar

22,

2022)

-

U.S. & Canada softwood and panel markets - week 9 2022 (Mar

15,

2022)

-

U.S. & Canada softwood and panel markets - week 8 2022 (Mar

08,

2022)

-

U.S. & Canada softwood and panel markets - week 7 2022 (Mar

01,

2022)

-

U.S. & Canada softwood and panel markets - week 6 2022 (Feb

22,

2022)

-

U.S. & Canada softwood and panel markets - week 5 2022 (Feb

15,

2022)

-

U.S. & Canada softwood and panel markets - week 4 2022 (Feb

08,

2022)

-

U.S. & Canada softwood and panel markets - week 3 2022 (Feb

01,

2022)

-

U.S. & Canada softwood and panel markets - week 2 2022 (Jan

25,

2022)

-

U.S. & Canada softwood and panel markets - week 1 2022 (Jan

18,

2022)

-

U.S. & Canada softwood and panel markets - week 47 2021 (Dec

22,

2021)

-

U.S. & Canada softwood and panel markets - week 46 2021 (Dec

15,

2021)

-

U.S. & Canada softwood and panel markets - week 45 2021 (Dec

08,

2021)

-

U.S. & Canada softwood and panel markets - week 44 2021 (Dec

01,

2021)

-

U.S. & Canada softwood and panel markets - week 43 2021 (Nov24,

2021)

-

U.S. & Canada softwood and panel markets - week 42 2021 (Nov17,

2021)

-

U.S. & Canada softwood and panel markets - week 41 2021 (Nov10,

2021)

-

U.S. & Canada softwood and panel markets - week 40 2021 (Nov

03,

2021)

-

U.S. & Canada softwood and panel markets - week 39 2021 (Oct

27,

2021)

-

U.S. & Canada softwood and panel markets - week 38 2021 (Oct

20,

2021)

-

U.S. & Canada softwood and panel markets - week 37 2021 (Oct

13,

2021)

-

U.S. & Canada softwood and panel markets - week 36 2021 (Oct

06,

2021)

-

U.S. & Canada softwood and panel markets - week 35 2021 (Sep

29,

2021)

-

U.S. & Canada softwood and panel markets - week 34 2021 (Sep

22,

2021)

-

U.S. & Canada softwood and panel markets - week 33 2021 (Sep

8,

2021)

-

U.S. & Canada softwood and panel markets - week 32 2021 (Sep

1,

2021)

-

U.S. & Canada softwood and panel markets - week 31 2021 (Aug

25,

2021)

-

U.S. & Canada softwood and panel markets - week 30 2021 (Aug

18,

2021)

-

U.S. & Canada softwood and panel markets - week 29 2021 (Aug

11,

2021)

-

U.S. & Canada softwood and panel markets - week 28 2021 (Aug

04,

2021)

-

U.S. & Canada softwood and panel markets - week 27 2021 (Jul

28,

2021)

-

U.S. & Canada softwood and panel markets - week 26 2021 (Jul

21,

2021)

-

U.S. & Canada softwood and panel markets - week 25 2021 (Jul

14,

2021)

-

U.S. & Canada softwood and panel markets - week 24 2021 (Jul

07,

2021)

-

U.S. & Canada softwood and panel markets - week 23 2021 (Jun

30,

2021)

-

U.S. & Canada softwood and panel markets - week 22 2021 (Jun

23,

2021)

-

U.S. & Canada softwood and panel markets - week 21 2021 (Jun

10,

2021)

-

U.S. & Canada softwood and panel markets - week 20 2021 (Jun

03,

2021)

-

U.S. & Canada softwood and panel markets - week 19 2021 (May

26,

2021)

-

U.S. & Canada softwood and panel markets - week 18 2021 (May

19,

2021)

-

U.S. & Canada softwood and panel markets - week 17 2021 (May

12,

2021)

-

U.S. & Canada softwood and panel markets - week 16 2021 (May

5,

2021)

-

U.S. & Canada softwood and panel markets - week 15 2021 (Apr

28,

2021)

-

U.S. & Canada softwood and panel markets - week 14 2021 (Apr

21,

2021)

-

U.S. & Canada softwood and panel markets - week 13 2021 (Apr

15,

2021)

-

U.S. & Canada softwood and panel markets - week 12 2021 (Apr

8,

2021)

-

U.S. & Canada softwood and panel markets - week 11 2021 (Apr

1,

2021)

-

U.S. & Canada softwood and panel markets - week 10 2021 (Mar

25,

2021)

-

U.S. & Canada softwood and panel markets - week 09 2021 (Mar

17,

2021)

-

U.S. & Canada softwood and panel markets - week 08 2021 (Mar

10,

2021)

-

U.S. & Canada softwood and panel markets - week 07 2021 (Mar

03,

2021)

-

U.S. & Canada softwood and panel markets - week 06 2021 (Feb

24,

2021)

-

U.S. & Canada softwood and panel markets - week 05 2021 (Feb

16,

2021)

-

U.S. & Canada softwood and panel markets - week 04 2021 (Feb

04,

2021)

-

U.S. & Canada softwood and panel markets - week 03 2021 (Jan

29,

2021)

-

U.S.&nb303& Canada softwood and panel markets - week 02 2021 (Jan

22,

2021)

-

U.S. & Canada softwood and panel markets - week 01 2021 (Jan

15,

2021)

-

U.S. & Canada softwood and panel markets - week 49 2020 (Dec

16,

2020)

-

U.S. & Canada softwood and panel markets - week 48 2020 (Dec

09,

2020)

-

U.S. & Canada softwood and panel markets - week 47 2020 (Dec

02,

2020)

-

U.S. & Canada softwood and panel markets - week 46 2020 (Nov

25,

2020)

-

U.S. & Canada softwood and panel markets - week 45 2020 (Nov

18,

2020)

-

U.S. & Canada softwood and panel markets - week 44 2020 (Nov

11,

2020)

-

U.S. & Canada softwood and panel markets - week 43 2020 (Nov

4,

2020)

-

U.S. & Canada softwood and panel markets - week 42 2020 (Oct

28,

2020)

-

U.S. & Canada softwood and panel markets - week 41 2020 (Oct

21,

2020)

-

U.S. & Canada softwood and panel markets - week 40 2020 (Oct

14,

2020)

-

U.S. & Canada softwood and panel markets - week 39, 2020 (Oct

07,

2020)

-

U.S. & Canada softwood and panel markets - week 38, 2020 (Sep

30,

2020)

-

U.S. & Canada softwood and panel markets - week 37, 2020 (Sep

23,

2020)

-

U.S. & Canada softwood and panel markets - week 36, 2020 (Sep

16,

2020)

-

U.S. & Canada softwood and panel markets - week 35, 2020 (Sep

09,

2020)

-

U.S. & Canada softwood and panel markets - week 34, 2020 (Sep

02,

2020)

-

U.S. & Canada softwood and panel markets - week 33, 2020 (Aug

26,

2020)

-

U.S. & Canada softwood and panel markets - week 32, 2020 (Aug

19,

2020)

-

U.S. & Canada softwood and panel markets - week 31, 2020 (Aug

12,

2020)

-

U.S. & Canada softwood and panel markets - week 30, 2020 (Aug

05,

2020)

-

U.S. & Canada softwood and panel markets - week 29, 2020 (Jul

29,

2020)

-

U.S. & Canada softwood and panel markets - week 28, 2020 (Jul

22,

2020)

-

U.S. & Canada softwood and panel markets - week 27, 2020 (Jul

17,

2020)

-

U.S. & Canada softwood and panel markets - week 26, 2020 (Jul

10,

2020)

-

U.S. & Canada softwood and panel markets - week 25, 2020 (Jul

02,

2020)

-

U.S. & Canada softwood and panel markets - week 24, 2020 (Jun

25,

2020)

-

U.S. & Canada softwood and panel markets - week 23, 2020 (Jun

17,

2020)

-

U.S. & Canada softwood and panel markets - week 22, 2020 (Jun

10, 2020)

-

U.S. & Canada softwood and panel markets - week 21, 2020 (Jun

3, 2020)

-

U.S. & Canada softwood and panel markets - week 20, 2020 (May 27,

2020)

-

U.S. & Canada softwood and panel markets - week 19, 2020 (May 21,

2020)

-

U.S. & Canada softwood and panel markets - week 18, 2020 (May 15,

2020)

-

U.S. & Canada softwood and panel markets - week 17, 2020 (May 8,

2020)

-

U.S. & Canada softwood and panel markets - week 16, 2020 (May 1,

2020)

-

U.S. & Canada softwood and panel markets - week 15, 2020 (Apr

23,

2020)

-

U.S. & Canada softwood and panel markets - week 14, 2020 (Apr

17, 2020)

-

U.S. & Canada softwood and panel markets - week 13, 2020 (Apr

08, 2020)

-

U.S. & Canada softwood and panel markets - week 12, 2020 (Mar

31, 2020)

-

U.S. & Canada softwood and panel markets - week 11, 2020 (Mar

24,

2020)

-

U.S. & Canada softwood and panel markets - week 5, 2020 (Feb

11,

2020)

-

U.S. & Canada softwood and panel markets - week 4, 2020 (Feb

4, 2020)

-

U.S. & Canada softwood and panel markets - week 3, 2020 (January

27,

2020)

-

U.S. & Canada softwood and panel markets - week 2, 2020 (January

20,

2020)

-

U.S. & Canada softwood and panel markets - week 1, 2020 (January

13,

2020)

-

U.S. & Canada softwood and panel markets - week 50, 2019 (December

17,

2019)

-

U.S. & Canada softwood and panel markets - week 49, 2019 (December

10,

2019)

-

U.S. & Canada softwood and panel markets - week 48, 2019 (December

3, 2019)

-

U.S. & Canada softwood and panel markets - week 47, 2019 (November

26, 2019)

-

U.S. & Canada softwood and panel markets - week 46, 2019 (November

19, 2019)

-

U.S. & Canada softwood and panel markets - week 45, 2019 (November

12, 2019)

-

U.S. & Canada softwood and panel markets - week 44, 2019 (November

5, 2019)

-

U.S. & Canada softwood and panel markets - week 43, 2019 ( October

29, 2019)

-

U.S. & Canada softwood and panel markets - week 42, 2019 ( October

22, 2019)

-

U.S. & Canada softwood and panel markets - week 41, 2019 ( October

15, 2019)

-

U.S. & Canada softwood and panel markets - week 40, 2019 ( October

8, 2019)

-

U.S. & Canada softwood and panel markets - week 39, 2019 ( October

1, 2019)

-

U.S. & Canada softwood and panel markets - week 38, 2019 ( September 24,

2019)

-

U.S. softwood and panel markets - week 37, 2019 ( September 17,

2019)

-

U.S. softwood and panel markets - week 36, 2019 ( September 10,

2019)

-

U.S. softwood and panel markets - week 35, 2019 ( September 3,

2019)

-

U.S. softwood and panel markets - week 34, 2019 ( August 23,

2019)

-

U.S. softwood and panel markets - week 33, 2019 ( August 16,

2019)

-

U.S. softwood and panel markets - week 32, 2019 ( August 09,

2019)

-

U.S. softwood and panel markets - week 31, 2019 ( August 02,

2019)

-

U.S. softwood and panel markets - week 30, 2019 ( July

26, 2019)

-

U.S. softwood and panel markets - week 29, 2019 ( July 19,

2019)

-

U.S. softwood and panel markets - week 28, 2019 ( July 12,

2019)

-

U.S. softwood and panel markets - week 27, 2019 ( July 03,

2019)

-

U.S. softwood and panel markets - week 26, 2019 ( June 28,

2019)

-

U.S. softwood and panel markets - week 25, 2019 ( June 21,

2019)

-

U.S. softwood and panel markets - week 24, 2019 ( June 14,

2019)

-

U.S. softwood and panel markets - week 23, 2019 ( June 07,

2019)

-

U.S. softwood and panel markets - week 22, 2019 ( May 31,

2019)

-

U.S. softwood and panel markets - week 21, 2019 ( May 24,

2019)

-

U.S. softwood and panel markets - week 20, 2019 ( May 17,

2019)

-

U.S. softwood and panel markets - week 19, 2019 ( May 10,

2019)

-

U.S. softwood and panel markets - week 18, 2019 ( May 03,

2019)

-

U.S. softwood and panel markets - week 17, 2019 ( April 26,

2019)

-

U.S. softwood and panel markets - week 16, 2019 ( April 19,

2019)

-

U.S. softwood and panel markets - week 15, 2019 ( April 12,

2019)

-

U.S. softwood and panel markets - week 14, 2019 ( April 05,

2019)

-

U.S. softwood and panel markets - week 13, 2019 ( March

29, 2019)

-

U.S. softwood and panel markets - week 12, 2019 ( March

22, 2019)

-

U.S. softwood and panel markets - week 11, 2019 ( March

15, 2019)

-

U.S. softwood and panel markets - week 10, 2019 ( March

08, 2019)

-

U.S. softwood and panel markets - week 9, 2019 ( March

01, 2019)

-

U.S. softwood and panel markets - week 8, 2019 ( February.

22, 2019)

-

U.S. softwood and panel markets - week 7, 2019 ( February.

15, 2019)

-

U.S. softwood and panel markets - week 6, 2019 ( February.

08, 2019)

-

U.S. softwood and panel markets - week 5, 2019 ( February.

01, 2019)

-

U.S. softwood and panel markets - week 4, 2019 (January. 25,

2019)

-

U.S. softwood and panel markets - week 3, 2019 (January. 18,

2019)

-

U.S. softwood and panel markets - week 2, 2019 (January. 11,

2019)

-

U.S. softwood and panel markets - week 1, 2019 (January. 04,

2019)

|

|

|