| Home: Global Wood |

|

Industry News & Markets |

|

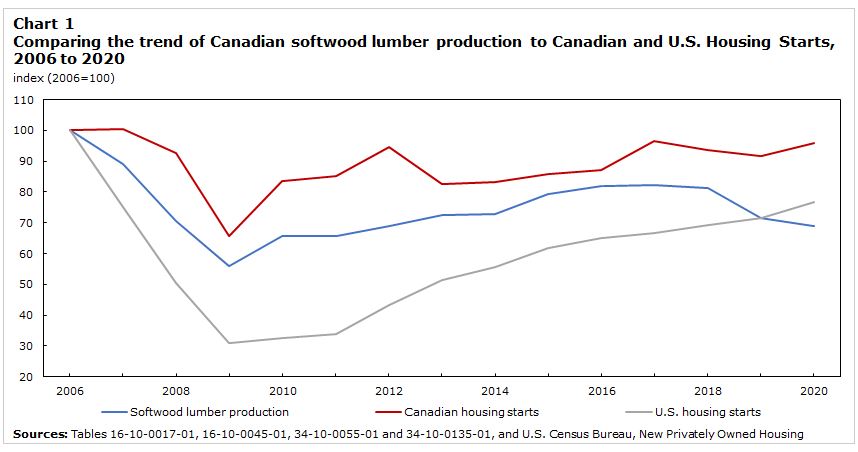

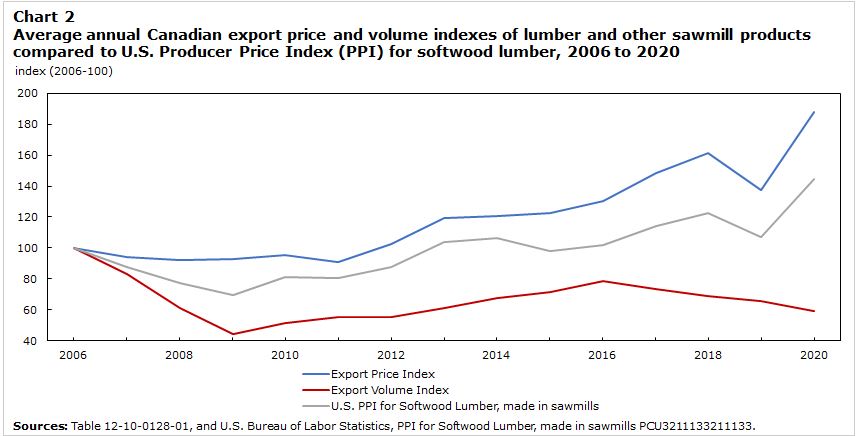

Analysis in Brief The purpose of this research paper is to highlight the impact of the many challenges faced over time by the sawmill industry on its development and its role as an economic lever for many Canadian communities. The sawmill industry produces softwood and hardwood lumber, as well as various by-products, such as wood chips and sawdust, that are used as inputs in other industries. Softwood lumber represented 98% of all lumber production in 2020. As one of the world's largest producers and exporters of softwood lumber, demand for Canadian lumber is largely driven by U.S. imports. In 2020, 67% of Canada's softwood lumber production was exported, 84% of which was to the U.S. Dimension softwood lumber is the main material used in home construction, whether it be for the framing and roofing of new housing or for rebuilding and renovating existing homes. Therefore, Canadian sawmills rely on growth in both the domestic and the U.S. housing markets to stimulate production and capital investment. Significant changes in the economic state of either country as well as in trade policy can affect the viability of the Canadian sawmill industry. The forestry sector has had its share of challenges that have impacted the demand for lumber and the supply chain: the financial crisis in 2008/2009, trade conditions imposed by the U.S. on Canadian lumber imports, ongoing fibre supply challenges in western Canada due to wildfires, damage caused by mountain pine beetle, changes to land use regulations, as well as rail car availability issues. These challenges combined with the high cost of logs, pulpwood and other forestry products in recent years have led to a number of mills curtailing production in 2019, with some closing indefinitely. In 2020, the COVID-19 pandemic exacerbated market conditions with excess demand, resulting in skyrocketing lumber prices. The role of the wood industry in Canada Revenue from goods manufactured in the wood product industry contributed 5% to total revenue from goods manufactured in 2006, of which sawmill and wood preservation represented about half. In 2020, the wood product industry contributed 6% to revenue from goods manufactured of a value of $635.1 billion. In 2020, the sawmill and wood preservation industry employed an annual average of 32,124 workers. Most likely driven by a modernization shift that impacted infrastructure, equipment and production processes, employment was down 41.0% (or 22,330 employees) compared with 2006, while employee productivity improved 17.2% over the same period. In 2020, over three-quarters of sawmill and wood preservation industry workers were employed in British Columbia, Quebec and Alberta. When comparing 2020 with 2006, the average Canadian weekly earnings for the sawmill and wood preservation industry increased 44.4% to about $1,241, compared with a 27.7% increase seen for the manufacturing sector as a whole. British Columbia, Quebec and Alberta produced 81% of Canada's softwood lumber in 2020. Since 2006, Alberta gained 8 percentage points of the Canadian market, while British Columbia lost 13 percentage points. While sawmills (except shingle and shake mills) manufacturing is important to themany provinces' economies, it was the largest manufacturing industry in British Columbia in 2020, with a 12% share of the province's total revenue from goods manufactured. However, this represents a drop from 16% in 2006. Exports of softwood lumber accounted for 14% of British Columbia's total domestic merchandise exports in 2020.  Impact of the financial crisis Most manufacturing industries were adversely impacted by the financial crisis in 2008/2009, with total revenue from goods manufactured in Canada falling 17.8% (-$106.6 billion) from 2007 to 2009. The impact was more severe for sawmills, with revenue from goods manufactured falling 40.3% (-$4.6 billion) over the same period. Canada exported 44% of the total quantity of softwood lumber it produced to the U.S. in 2009, a 11 percentage-point reduction from 2007. Demand for Canadian softwood lumber was significantly impacted in 2008-2009 due to sharp declines in Canadian and U.S. new housing starts. In 2009, housing starts in Canada were at their lowest since 1999 (149,081 units). From 2009 to their latest peaks in 2017, softwood lumber production and new housing in Canada both trended upward. However, in 2020, both were still below pre-financial crisis levels. U.S. total housing starts recorded a steeper decline, falling 69.2% from 2006 to 554,000 units in 2009, the lowest level since 1959. The market has been slowly recovering since 2009, as U.S. housing starts grew to reach 1,379,600 units in 2020. Canadian lumber production began contracting in 2017, even though housing starts were still increasing. Impact of the expiration of the Softwood Lumber Agreement While the U.S. has long been the largest importer of Canadian softwood lumber, their share fell 12 percentage points (to 70%) over the span of the most recent Softwood Lumber Agreement (2006 to 2015). During this period, Canada expanded to other markets, such as China. The Softwood Lumber Agreement expired in October 2015 and, since then, the U.S. regained 14.0 percentage points of the share (to 84%) of Canada's $10.0 billion in exportations in 2020. Although the demand for softwood lumber from the U.S. housing market has been gradually improving, and Canadian exportations to the U.S. have increased in dollar value, the quantity of lumber and other sawmill products exported to the U.S. has been steadily declining since 2016. According to U.S. Census Bureau data, the share of U.S. imports of softwood lumber from Canada had fallen 11 percentage points in 2020, mostly lost to the European Union. Chart 2 Average annual Canadian export price and volume indexes of lumber and other sawmill products compared to U.S. Producer Price Index (PPI) for softwood lumber, 2006 to 2020  The decrease in production of Canadian wood products was also reflected by the 10 percentage-point drop in the average industrial capacity utilization rate for wood product manufacturing from 2016, down to 78% in 2020. Canada's export prices have grown 87.9% over the past 15 years, while U.S. domestic prices have risen by 44.4% over the same period. Click here to view the full article-->> Source: Statistics Canada |