| Home: Global Wood |

|

Industry News & Markets |

|

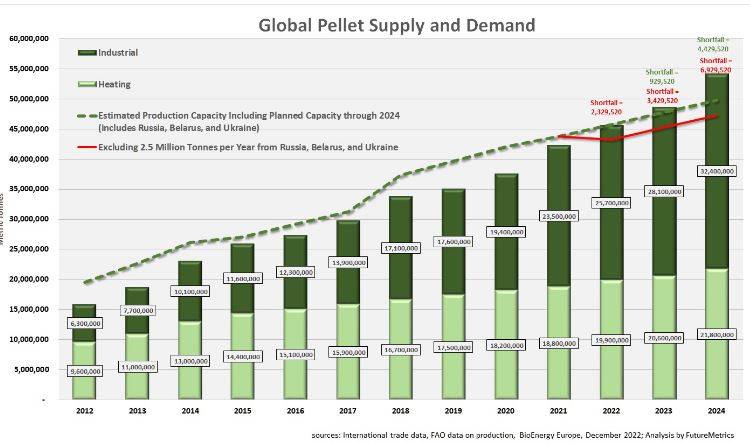

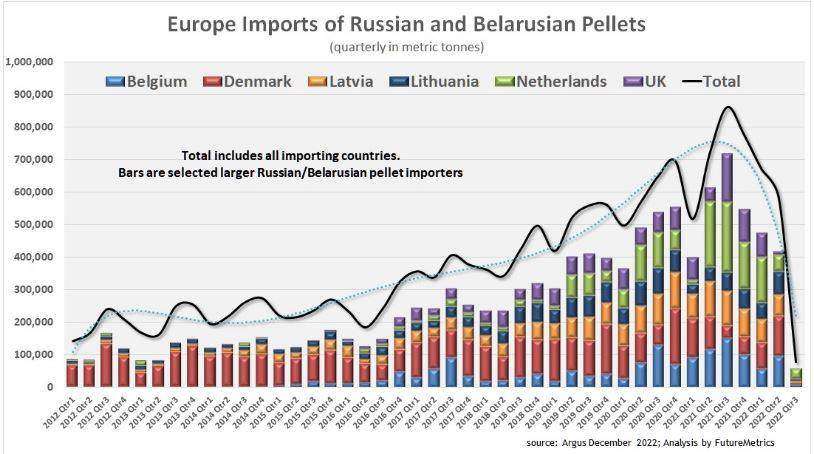

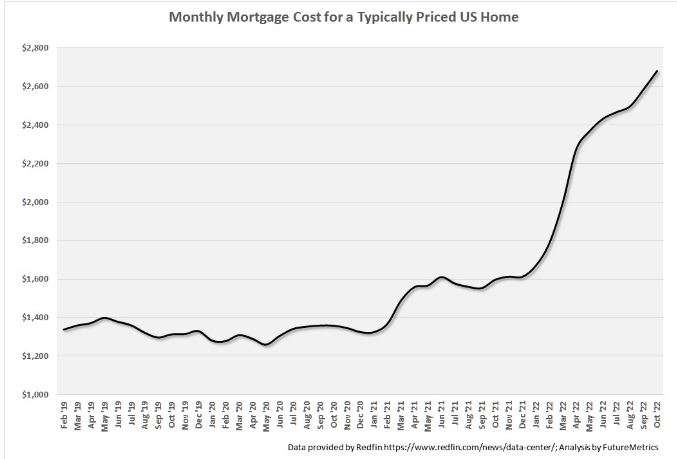

A look at the challenges and opportunities ahead for wood pellet markets in 2023.  The wood pellet sector is facing two critical challenges this year: the impact of inflation on the pellet fuel supply chain, and the impacts of the Russian invasion of Ukraine on global supply and demand. While this article focuses on economic and geopolitical forces, it should be noted that policy matters too. As the frequency and severity of the consequences of climate change increase, the goal of decarbonizing the energy sector will drive policymaking. Pragmatic and rational policy will recognize the value of sustainably sourced renewable solid fuel for heat and power as a necessary support mechanism for the off-ramp to a decarbonized future. And while this article focuses on near-term challenges, FutureMetrics strongly believes that the benefits derived from replacing some fossil fuels with renewing carbon beneficial pellet fuel will support continued robust demand at least for the next few decades. Challenge: higher wood costs  High inflation is creating challenges in every sector. For pellet manufactures, there are obvious concerns about labour costs, consumables costs, and power costs. However, the largest cost to producing wood pellets is the cost of the delivered woody feedstock. Pellet factories, as FutureMetrics has stated in a number of presentations, are “bottom feeders”. They depend on the residuals from sawmills and from managed working forest harvests. Pellet plants cannot pay sawlog pricing for feedstock. Thus, the demand by primary users of forest products, i.e., sawmills, impacts the supply of the sawmill and forest by-products. (On average, about 60 per cent of a sawlog becomes lumber or other finished products. The rest is sawdust, edge slabs, and bark.) Part of the current pellet feedstock challenges in North America derive from the U.S. federal government’s response to high inflation. Higher interest rates make the cost of home ownership higher. The monthly mortgage cost for a typical home in the U.S. has doubled in the past 18 months.  As a result, starts for new private homes in the U.S. have declined significantly since earlier this year. The drop in demand for lumber has led to a slowdown in sawmilling output. This is most acute in Western Canada. According to the Forisk Blog (forisk.com) “…in Western Canada, there has been at least 1.7 BBF of announced capacity curtailments in 2022, mostly motivated by increased log prices and falling lumber prices, which reduces or eliminates margins.” Less output by sawmills cascades into less sawmill residuals. And lower demand for sawlogs lowers the production of forest residuals. Adding to the cyclical downturn in the housing market are high diesel fuel prices. A significant proportion of the cost of feedstock delivered to a pellet factory is embodied in the cost of the diesel fuel used for transportation. The larger the draw radius of the pellet factory (i.e., the larger the factory, or the slower the forests grow at higher latitudes), the more sensitive is the factory to changes in diesel fuel costs. Pellet producers in almost all locations, not just in North America, are experiencing similar challenges. Housing markets are traditionally cyclical and eventually housing starts will revert to trend. Diesel fuel costs may reset at a higher “new normal” which would mean higher costs in every sector in which transportation is needed. View the full article here -->> |