|

Report from

Europe

Slow start to the year for UK tropical imports

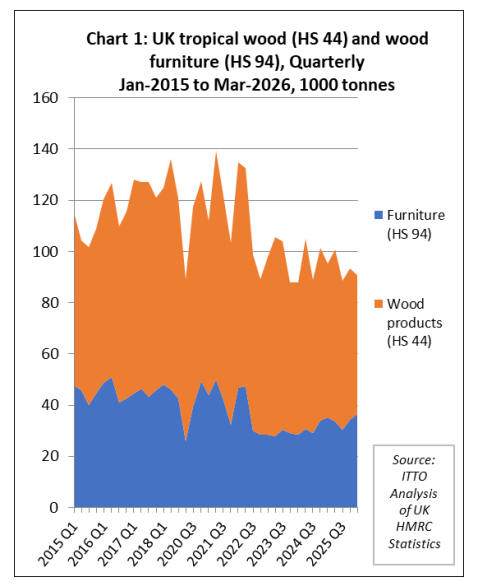

UK imports of tropical wood products have started this

year very slowly, continuing at the low level maintained

since the end of the COVID pandemic in 2022 and remain

around 15% below the pre-pandemic level. Prospects for

any significant uptick in 2026 remain very muted as the

economy is struggling to shift into a higher gear and

supply is also a constraint.

In the first four months of this year, the UK imported

123,000 tonnes of tropical wood and wooden furniture

products, 6% less than the same period in 2025.

Import value in the first four months was US$351 million,

1% less in nominal terms and over 3% less in real terms

(i.e. taking account of inflation) than the same period in

2025. On a quarterly basis, import tonnage in Q1 2026

was 7% down on previous quarter and 4% down compared

to Q1 last year (Chart 1).

The quantity of tropical wooden furniture imported into

the UK increased by 2% to 48,700 tonnes in the first four

months this year compared to the same last year.

There were also good percentage gains in imports of some

smaller volume products including mouldings/decking

(+23% to 3,800 tonnes), flooring (+8% to 1,100 tonnes),

and kitchenware (+30% to 1,000 tonnes). However

tropical plywood was down 25% to 22,500 tonnes, joinery

was down 12% to 23,000 tonnes, and sawnwood was

down 4% to 18,100 tonnes.

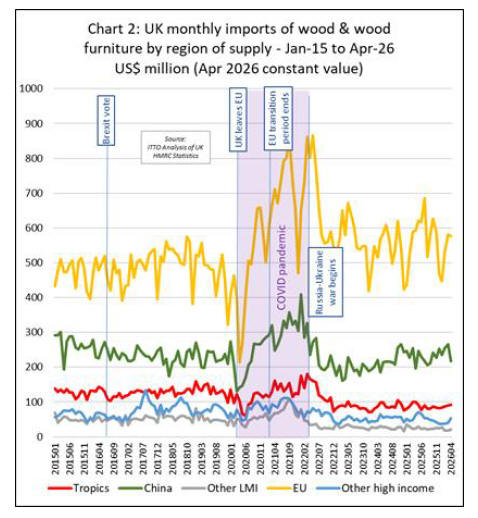

UK accounts for around one quarter of all tropical

imports into Europe

Chart 2 sets UK imports from the tropics (red line) in the

wider context of UK wood and wooden furniture trade. It

highlights the relatively small, but still significant, role

played by tropical products in this market.

The UK alone now accounts for about a quarter of the total

value of all tropical wood and wooden furniture product

imports into European countries.

Unlike UK imports from the EU and China, which saw

massive, unsustainable peaks during the 2020–2022

pandemic peak, UK imports from the tropics have

remained relatively flat over the long term if measured in

real dollar terms (adjusted for inflation). Since the start of

2021, they have bumped along at around US$90 million a

month (in April 2026 constant value). This, however, is a

significant downward step change from a figure of around

US$130 million per month in the five years leading up to

the COVID pandemic.

The EU (yellow line) is consistently the UK's largest

supplier of wood and wooden furniture, a dominant

position not only maintained, but enhanced despite Brexit

in the recent years of highly volatile trading conditions.

Between 2025 and early 2026, UK imports from the EU

have stabilized at a higher baseline (averaging around

US$550 million per month) than pre-pandemic levels

(when they averaged around US$450 million).

In contrast, imports from China (green line), after

experiencing rapid gains during the immediate post

COVID boom, have since levelled out at close to their

historical average of around US$200–US$250 million per

month.

In the first four months of this year, UK import value of

wood and wooden furniture from all supply regions

totalled US$3.72 billion, 1% less in real terms compared

to the same period in 2025.

The share of tropical wood and wooden furniture products

in total UK import value was 9.5% during the first four

months of this year, down from 9.8% in the same period in

2025. The long term slide in share is continuing for now,

down from share of 11.4% in 2022 and close to 14%

typical before the COVID pandemic.

UK growth constrained by rising interest rates

Prospects for a significant short-term surge in the UK

market for wood products remain muted as the economy

struggles to shift into a higher gear.

According to recent consensus reports, City analysts are

forecasting a highly gradual trajectory for GDP, tempered

by sticky inflation risks.

While early-year fears of a dramatic economic contraction

have faded into a pattern of stagnation, there remains little

room for substantial fiscal or government intervention due

to persistent global supply uncertainties stemming from

ongoing tensions in the Middle East.

Independent forecasts show the limits of the current

recovery. The IMF recently lowered its UK GDP growth

forecast for 2026 to 0.8%, while the OECD projects a

similarly modest expansion of 0.9% for the year, noting

that geopolitical risks continue to stoke inflationary

pressures. Oxford Economics points to a consumer

squeeze, forecasting that real income growth will slow to

0.6% as tighter fiscal policies take hold.

Though Consumer Price Index (CPI) inflation fell to 2.8%

in May—a notable drop from earlier spikes—it continues

to hover stubbornly above the Bank of England's 2.0%

target. In response, the Bank of England’s Monetary

Policy Committee (MPC) voted 7–2 at its June 2026

meeting to maintain the base interest rate at 3.75%.

Although some analysts had earlier hoped for a steady

sequence of rate cuts by mid-year, two hawkish MPC

members actually voted for a hike to 4.0%, citing

structural inflation risks.

Financial markets have capitulated on hopes for swift

monetary relief, with the consensus now indicating that

borrowing costs—which remain anchored at near-two-

decade highs—will stay at 3.75% for the foreseeable

future, severely capping real estate and commercial

financing flexibility.

The latest data from the UK construction sector directly

mirrors this tight credit environment, offering a mixed but

generally challenging outlook for industrial wood demand.

According to the June 2026 data from the Office for

National Statistics (ONS), total construction output rose

by 1.6% in the three months to April 2026. This rolling

three-month growth was overwhelmingly driven by a

3.4% surge in repair and maintenance activity, whereas

new work grew by a marginal 0.3%.

On an annual basis, the picture is considerably more

troubling for primary timber consumption. Total year-on-

year construction output for April 2026 dropped by 1.0%,

led by a sharp 4.8% contraction in overall new work. At

the sector level, new housing remains the primary drag on

the industry; private housing output plunged by 8.2% year-

on-year, and public housing collapsed by 12.6%.

Monthly construction output edged up by just 0.1% in

April 2026, marking a sharp deceleration from the 1.5%

growth seen in March. Crucially for the hardwood sector,

this minimal monthly expansion came solely from a 0.6%

increase in repair and maintenance, which continues to

provide some relief for joinery and refurbishment

products.

In contrast, monthly volume for new build projects fell by

0.3%, highlighting that high borrowing costs continue to

suppress the breaking of new ground across the UK

housing market.

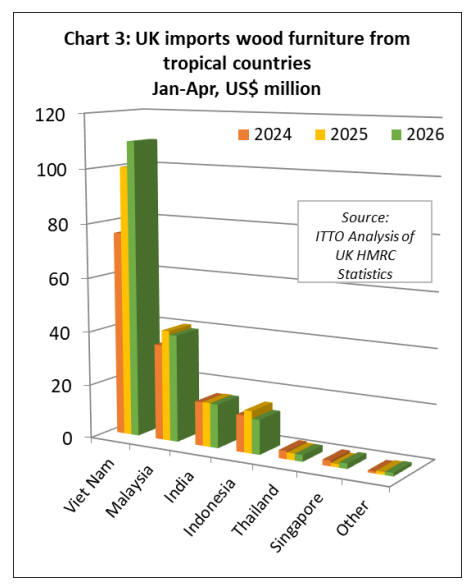

Sharp rise in UK imports of wooden furniture from Viet

Nam

In the first four months of this year, UK import value of

wooden furniture from tropical countries increased 3% to

US$184 million while import quantity increased 2% to

48,700 tonnes. The growth so far this year has been

strongly concentrated in furniture products imported from

Viet Nam (+9% to US$191 million).

Imports of wooden furniture declined from other major

supply countries, including Malaysia (-3% to US$40

million), India (-1% to US$16 million), Indonesia (-18%

to US$13 million), and Thailand (-2% to US$2.5 million).

However, imports from Singapore increased by 60% from

a small base, to US$2.0 million. UK wooden furniture

imports were negligible from all other tropical countries

during the first four months of this year (Chart 3).

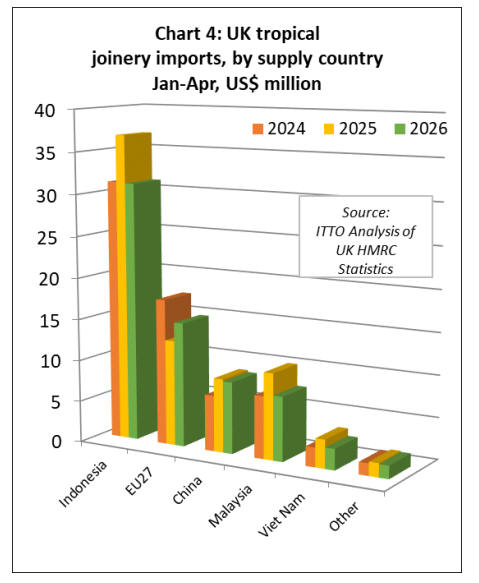

Decline in UK imports of joinery

In the first four months of this year, UK import value of

wood joinery from tropical countries decreased 10% to

US$67 million. The decline during the period was

widespread among major Asian suppliers, particularly

affecting Indonesia (-15% to US$31.2 million), Malaysia

(-25% to US$7.7 million) and Viet Nam (-26% to US$2.5

million). Imports from China fell slightly by 3% to US$8.6

million.

In contrast, tropical wood joinery imports from the EU27

bucked the trend, rising 18% to US$15 million. Wood

joinery imports were negligible from all other tropical

countries during the first four months of this year (Chart

4).

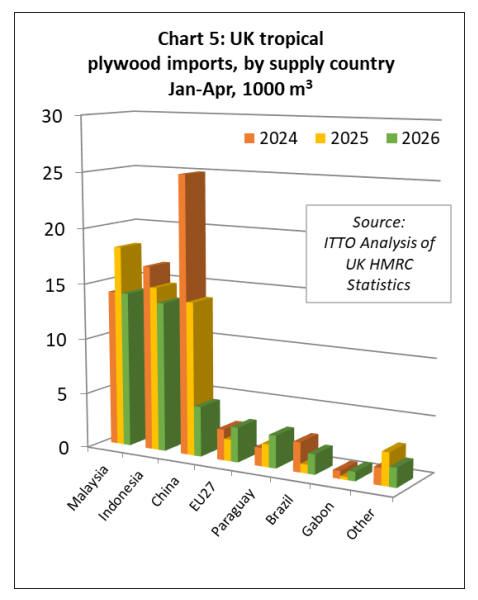

Collapse in UK imports of plywood from China

In the first four months of this year, UK import volume of

plywood from tropical countries decreased 23% to 42,400

cu.m. The reduction so far this year has been heavily

driven by a collapse in shipments from China (-67% to

4,500 cu.m).

Imports also contracted from major traditional suppliers,

including Malaysia (-23% to 14,000 cu.m) and Indonesia

(-9% to 13,500 cu.m). However, imports of tropical

hardwood plywood from the EU27 increased by 60% to

3,100 cu.m, and imports from Paraguay continued to

grow, up 43% to 2,900 cu.m. Notable gains from small

bases were also recorded for Brazil (+128% to 1,800 cu.m)

and Gabon (+212% to 800 cu.m), while imports from

other tropical regions remained low (Chart 5).

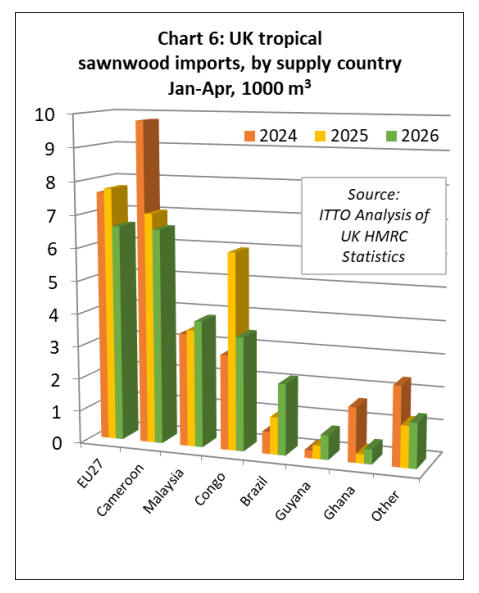

UK tropical sawnwood imports as Congo slip

In the first four months of this year, UK import volume of

tropical sawnwood decreased 8% to 25,300 cu.m. The

contraction so far this year was significantly influenced by

a sharp correction in imports from the Republic of Congo

(-42% to 3,500 cu.m). Shipments from Cameroon also

eased slightly, down 7% to 6,600 cu.m. There was also a

15% drop in imports from the EU27 to 6,600 cu.m.

The EU nevertheless remained the largest single supply

region for tropical hardwood sawnwood to the UK, much

of the wood coming from the Netherlands and Belgium.

On the positive side, imports from Malaysia grew 8% to

3,900 cu.m, while shipments from South American

suppliers rose steeply, with Brazil expanding 90% to 2,200

cu.m and Guyana jumping 84% to 700 cu.m. Ghana also

rebounded from a very low base, increasing 60% to 500

cu.m (Chart 6)

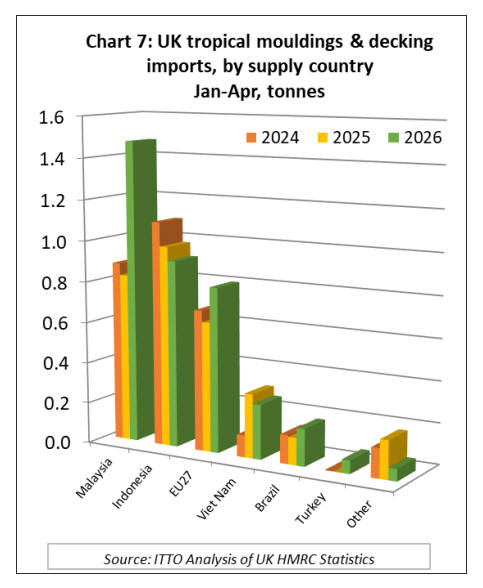

Robust growth in UK tropical decking and mouldings

imports led by Malaysia

In the first four months of this year, UK import volume of

tropical decking and mouldings increased 23% to 3,760

tonnes. The expansion so far this year has been

predominantly driven by a major surge in shipments from

Malaysia (+80% to 1,480 tonnes).

Imports from the EU27 also advanced strongly, rising

27% to 800 tonnes, while Brazil increased 37% to 180

tonnes. In contrast, imports slowed from Indonesia (-7% to

910 tonnes) and Viet Nam (-15% to 270 tonnes).

Meanwhile, imports from Turkey have just appeared on

the radar, rising from zero last year to reach 60 tonnes

(Chart 7).

UK announces intent to align closely with EUDR

On 23 June 2026, the UK government announced a

strengthened legislative approach to combatting global

deforestation in import supply chains with significant

implications for the wood and timber industries. Under the

new strategy the government plans to introduce

regulations for Great Britain (GB) in 2027 that will build

upon and strengthen the existing UK Timber Regulation

(UKTR). The new measures are specific to GB, i.e. that

portion of the UK not including Northern Ireland, which is

already part of the EU single market and therefore subject

to EUDR when implementation begins on 31 December

2026.

The upcoming framework will require GB businesses with

an annual turnover exceeding £1 million to conduct

mandatory due diligence on forest risk commodities,

explicitly including wood and derived products like

furniture. To prove compliance with local laws, affected

operators must establish verification systems, submit

activity reports and collect precise origin geolocation data.

Crucially for the market, the GB framework is designed to

align closely with the EUDR. This deliberate alignment

aims to minimise regulatory divergence, protect the UK

internal market and ease trading burdens for businesses

operating across both jurisdictions.

Because the UK is classified as a low-risk country,

businesses exporting GB-produced wood products to the

EU or moving them to Northern Ireland will benefit from

simplified due diligence requirements. That, however,

does not exempt UK suppliers from providing geolocation

data with their shipments into the EU internal market.

The evolving regulatory landscape raises complex

operational questions regarding how EU-derived timber

and products will be treated upon entering GB.

The EUDR underwent significant structural amendments

in December 2025 which not only postponed the

application dates but also significantly reduced due

diligence obligations for downstream operators in the EU.

As GB structures its independent 2027 framework to

broadly match EU data and traceability standards market

analysts are closely watching how the UK will evaluate

compliance for imports from the EU that benefit from

these newly amended, simplified European rules and

whether any reciprocal regulatory shortcuts will be

codified between the UK and EU.

Additionally, the 2027 framework raises questions around

treatment of the UK’s Voluntary Partnership Agreements

(VPAs) under the Forest Law Enforcement, Governance

and Trade (FLEGT) framework. Currently, the UK

FLEGT regime provides a streamlined "green lane" for

timber originating from VPA partner countries, most

notably Indonesia and Ghana, whereby a valid FLEGT

license serves as automatic proof of legality, bypassing

standard UKTR due diligence.

However, because the upcoming UK regulations shift

focus from merely stopping illegal logging to ensuring

broader deforestation-free supply chains, questions arise

around how these bilateral agreements will be integrated.

If the new 2027 rules mirror the EUDR's stance - where a

FLEGT license satisfies legality criteria but does not

exempt an importer from mandatory geolocation and

deforestation-free verification - the commercial advantage

enjoyed by FLEGT licensed products in the UK tropical

wood market could be altered.

There are also wider geopolitical issues raised by the UK’s

announcement. Last year the UK imported, from China,

US$3.7 billion of forest products that would be subject to

the new regulations. UK importers seeking to comply with

the new UK regulations will therefore need to navigate

both those requirements and China’s Decrees 834 and 835

which regulates foreign entities from conducting certain

due diligence and supply chain information-gathering

activities within China.

Last year, the UK also imported US$2.3 billion of forest

products from the US. This includes US$1.75 billion of

wood pellets which are important to the UK's current net-

zero strategy as they constitute the vast majority of

industrial biomass used for baseload electricity and is a

necessary component for negative emissions technologies

like Bioenergy with Carbon Capture and Storage

(BECCS).

The UK is also now by far the US largest export market

for solid hardwood products, with a total value of US$250

million last year. Nearly all these products derive

ultimately from innumerable small harvest sites distributed

amongst family forest owners in the Eastern US.

This has created obstacles to conformance with the

property level geolocation requirements of EUDR. The US

administration is calling for an exemption to the EUDR

requirements for this reason and can be expected to call

for a similar exemption in the UK.

|