US Dollar Exchange Rates of

25th

June

2026

China Yuan 6.80

Report from China

Housing market continues to struggle

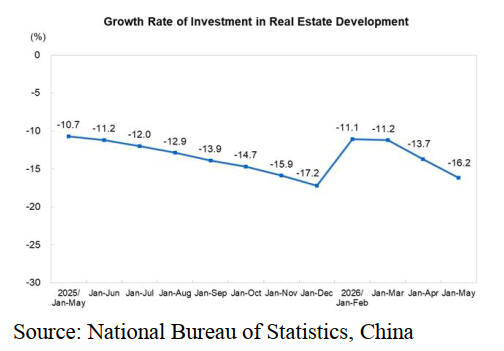

The National Bureau of Statistics (NBS) has reported

investment in real estate development from January to

May 2026 saying there was a year-on-year decrease of

16.2%, of which the investment in residential buildings

was down 15.6%.

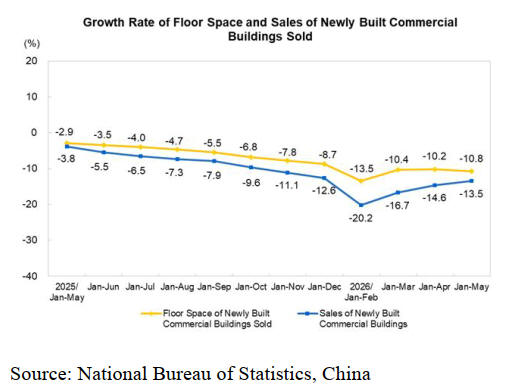

From January to May, the floor space of newly built

commercial buildings sold was 313.20 million square

metres, a year-on-year decrease of 10.8%, of which the

floor space of residential buildings sold decreased by

12.1%. Sales of newly built commercial buildings were

2,936.6 billion yuan, down 13.5%.

See:

https://www.stats.gov.cn/english/PressRelease/202606/t2026061

7_1963968.html

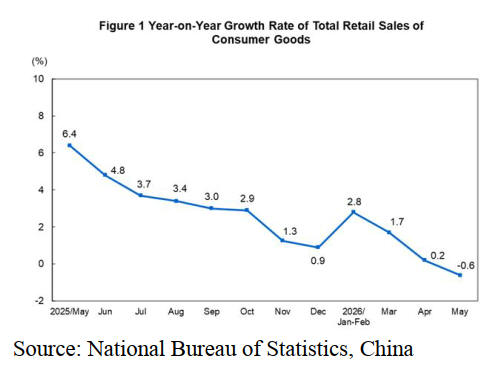

The NBS has also

reported total retail sales of consumer

goods. From January to May total retail sales of consumer

goods reached 20,603.1 billion yuan, up 1.4% year on

year. Specifically, retail sales of consumer goods

excluding automobiles reached 19,002.2 billion yuan, up

by 2.7%.

In May, retail sales of consumer goods reached 4,109.0

billion yuan, down by 0.6% year on year. Specifically, the

retail sales of consumer goods excluding automobiles

reached 3,778.1 billion yuan, up by 1.1%. Retail sales of

furniture between January and May declined 3%.

Rise in annual

timber production

It has been reported that China's forest harvest volume will

have approached 21 billion cubic metres in 2025, an

annual increase of over 1 billion cubic metres and the total

output value of forestry and grassland industries will reach

nearly RMB11 trillion (approximately US$1.6 trillion). As

of 2025 annual timber production has increased by nearly

36% compared to 2020.

Decline in wooden furniture exports to USA

According to China Customs, the value of China’s wooden

furniture exports to US dropped 13% in the first quarter of

2026. The US was the largest destination for China’s

wooden furniture exports. 25% of China’s wooden

furniture was exported to US in the first quarter of 2026

but the share of the US market continues to decline.

Exports of wooden furniture from China to the US have

decreased mainly due to the impact of US tariffs as well as

anti-dumping and anti-subsidies on China’s wooden

furniture.

Chinese wooden furniture has lost competitiveness and

companies are reluctant to take large orders from US

buyers, preferring to reduced their business in the US. As

a result, buyers in the US are increasingly turning to

Vietnam and Mexico. The tariffs applied to these two

countries are only around 10% giving them a significant

cost advantage over China.

The US market for wooden furniture has experienced a

sharp decline while the European Union has seen a steady

increase which has mainly benefitted SE Asian shippers.

China's wooden furniture exports have rapidly diversified.

Despite the drop in the value of China’s wooden furniture

exports to the US, total wooden furniture exports in the

first quarter 2026 rose 2% to US$5.4 billion over the same

period in 2025 due to the rise in exports to UK, Germany

and the Netherland.

The value of China’s wooden furniture exports to UK,

Germany and Netherland grew 18%, 36% and 28%

respectively. In addition, exports to both Australia and

France rose 9% in the first quarter of 2026.

In contrast, China’s wooden furniture exports to Japan,

South Korea and Saudi Arabia fell 6%, 5% and 1%

respectively in the first quarter of 2026.

China’s wooden furniture is exported to more than 200

countries. The value of China’s furniture exports to the top

10 countries accounted for only 65% of the national total

wooden furniture exports in the first quarter of 2026.

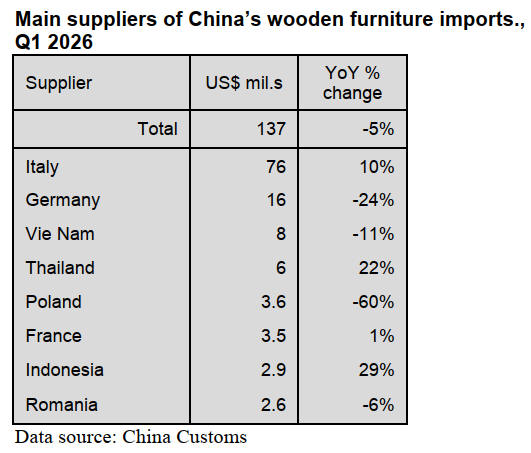

Decline in wooden furniture imports

China Customs data shows the value of China’s wooden

furniture imports in the first quarter of 2026 fell 5% to

US$137 million over the same period of 2025.

The main reasons for the decrease in the import of Chinese

wooden furniture are as follows:

New housing projects have started in China but

the demand for renovating old houses is sluggish.

The domestic demand for full-house

customisation and solid wooden furniture is

weak.

Factories are reducing inventory and not stocking

up on wooden furniture materials.

The wooden furniture factory significantly

reduced production and imports of logs and wood

panels both contracted simultaneously.

Domestic solid wood and panel furniture has seen

an improvement in quality and a reduction in

price, while the consumption of high-end

imported furniture has cooled down.

Italy and Germany are the top 2 suppliers of China’s

wooden furniture imports. 66% of China’s wooden

furniture were imported from these two countries and rose

10% from Italy but from Germany dropped 24% in the

first quarter of 2026.

The value of China’s wooden furniture imports from

Vietnam, Poland and Romania dropped 11%, 60% and 6%

respectively in the first quarter of 2026.

In contrast, the value of China’s wooden furniture imports

from Thailand and Indonesia rose 22% and 29%

respectively in the first quarter of 2025.

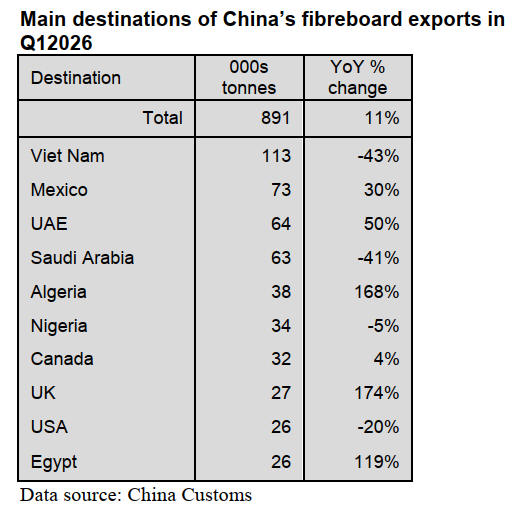

Rise in fibreboard exports

According to China Customs, fibreboard exports rose 11%

to 891,000 tonnes in the first quarter of 2026. Although

China’s fibreboard exports to Vietnam, as the largest

market in the first quarter of 2026, dropped 40% to

113,000 tonnes over the same period of 2026.

China’s fibreboard exports to Mexico and the UAE, as

second and third largest destination countries in the first

quarter of 2026 rose 30% and 50%.

In addition, China’s fibreboard exports to Algeria, UK and

Egypt surged over 160%, 170% and almost 120%

respectively in the first quarter of 2026.

The increases offset the decrease in the export of

fiberboard to Vietnam resulting in an overall 11% increase

in China's total fibreboard exports in the first quarter of

2026.

In contrast, in the first quarter of 2026, China’s fibreboard

exports to Saudi Arabia, Nigeria and US dropped 41%, 5%

and 20% respectively over the same period of 2025.

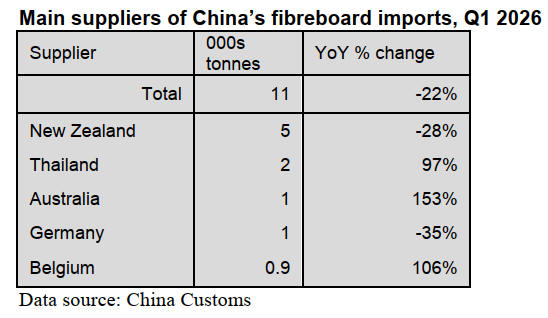

Decline in fibreboard imports

China Customs data indicates fibreboard imports totalled

11,000 tonnes in the first quarter of 2026, down 22% over

the same period of 2025. Imports from New Zealand in the

first quarter of 2026 dropped 28% from the same period of

2025.

It is worth noting that China’s fibreboard imports from

Thailand, Australia and Belgium in the first quarter of

2026 surged 97%, 153% and 106% over the same period

of 2025. In contrast, China’s fibreboard imports from

Germany in the first quarter of 2026 fell 35% year on year.

The main reason for the significant decline in China's

fiberboard imports in the first quarter of 2026 was the

abundant domestic supply which led to a substitution of

imports by domestic products.

The domestic capacity for fiberboard production is huge

and the self-sufficiency rate is continuously increasing.

China is the world's largest producer of fiberboard with a

total production capacity exceeding 40 million cubic

metres. Ordinary fibreboard and decorative fiberboards are

fully self-sufficient, while only a small amount of high-

quality speciality fibreboards are imported.

In the first quarter of 2026 there was a concentrated

logging of reserve forests and plantation and the supply of

wood chips for fibreboard increased significantly. The

production of fibreboard factories remained stable and the

inventory was sufficient.

Leading home furnishing enterprises are building their

own production lines upstream and reducing the purchase

of imported boards. Customised home furnishing leaders

such as OPPEIN and SOGAL have built fibreboard

workshops on their own, prioritising the use of domestic

non-toxic, F4-star environmentally friendly fibreboard.

The domestic supply chain has been advanced

significantly reducing the amount of overseas decorative

fiberboard purchases.

After adding shipping costs, tariffs and exchange rate costs

prices of imported fiberboard are generally higher than

those of similar domestic products.

May 2026 GTI report

Customs data shows that China’s timber imports reached

around 4.86 million cubic metres in April this year, up 4%

month-on-month. Of this volume, log imports stood at

approximately 2.98 million cubic metres, a 7.9% increase

from the previous month, while sawnwood imports edged

down 1.7% to about 1.88 million cubic metres.

During the same month, China imported 185,000 cubic

metres of timber from the United States, representing a

year-on-year increase of 23.6% and a sharp 44.5% rise

month-on-month, signaling tentative signs of recovery in

bilateral timber trade.

At present, China is actively promoting the development

of plantation forests such as eucalyptus and teak, in an

effort to achieve synergies between ecological

preservation and economic returns.

The latest data indicate that China’s annual eucalyptus

timber output exceeds 30 million cubic metres,

significantly reducing the country’s external dependence

on timber and securing raw material supplies for industries

such as construction, papermaking, furniture and

packaging.

In other news, data from the National Bureau of Statistics

of China shows that furniture manufacturers above the

designated size nationwide recorded a total profit of 2.67

billion yuan in the January–April period.

Currently, the furniture industry is showing a development

structure characterised by "export recovery but

manufacturing under pressure. Furniture enterprises are

maintaining their order volumes through price adjustments

and are in the "trading price for volume" stage.

In May 2026, the GTI-China index registered 47.8%, a

decrease of 5.7 percentage points from the previous month

and below the critical value (50%) again after two months.

Regarding the twelve

sub-indexes, five indexes (inventory

of finished products, purchase quantity, import, inventory

of main raw materials and delivery time) were above the

50% critical value, while the remaining seven indexes

(production, new orders, export orders, existing orders,

purchase price, employees and market expectation) were

below the critical value.

Compared to the previous month, the indexes for import

and inventory of main raw materials increased by 1.8 to

4.9 percentage points; the index for delivery time was

unchanged from the previous month and the remaining

nine indexes declined by 0.9 to 23.0 percentage point(s).

See: https://www.itto-

ggsc.org/static/upload/file/20260615/1781506386105682.pdf

|