Japan

Wood Products Prices

Dollar Exchange Rates of 25th

June

2026

Japan Yen 161.79

Reports From Japan

Inflation steady as subsidies restrain energy costs

Japan’s key inflation measure in May was little changed

from a month earlier due largely to government subsidies

that capped energy costs.

The Ministry of Internal Affairs and Communications

reported core consumer prices (excluding fresh food) rose

1.4% from a year earlier. .A measure that excludes both

fresh food and energy rose 1.8% from a year earlier.

The figures show how effective the government support

programmes have been in containing the cost of living,

largely through fuel subsidies. Recently the government

prepared an extra budget that will help continue to cushion

the impact of rising costs.

Even though the United States-Iran interim peace deal has

taken effect, oil prices are still elevated and importers say

it will take months, if not longer, for volumes of oil and

liquefied natural gas passing through the critical Strait of

Hormuz to return to normal.

The core consumer price index, excluding fresh food in

Japan was up 1.4% year on year in May. Hideo Kumano,

Chief Economist at Daiichi Life Research Institute warned

that the pass-through was not over: “Companies have yet

to fully pass on higher crude oil costs, meaning that price

increases will continue for a while, particularly further

down the supply chain.”

Kumano said restoring energy flows is also expected to be

difficult. Ensuring safety in the Strait of Hormuz and

removing mines would take time, while a tanker round trip

to bring crude oil to Japan would probably require around

six weeks.

See:

https://www.japantimes.co.jp/business/2026/06/19/economy/japa

n-inflation-holds-steady/

Investment plan for next 14 years unveiled

The government has unveiled a long-term vision for

economic development featuring massive investment in

artificial intelligence and semiconductors as well as other

key sectors including defense, space and shipbuilding.

This, says the government, will call for a combination of

public and private investment.

This new plan has shifted the fiscal focus toward reducing

the debt-to-GDP ratio, moving away from using a primary

balance target that had guided government policy for more

than two decades.

The debt-to-GDP metric is generally considered

easier to

improve during periods of inflation.

See:

https://www.japantimes.co.jp/business/2026/06/24/economy/inve

stment-plan-unveiled-14-years/

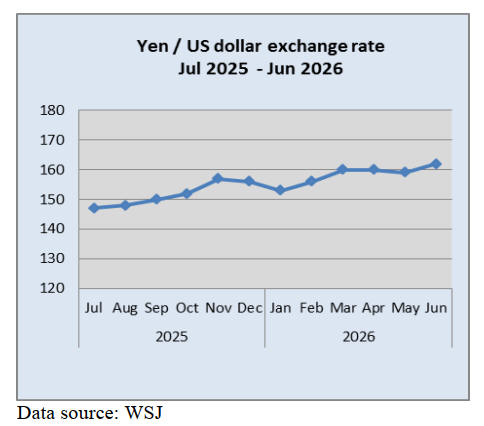

Yen at 162 to the US dollar, - intervention would not be

very effective now say experts

The yen crossed the ¥161 to the US dollar in late June

coming close to levels not seen since the 1980s. Finance

Minister, Satsuki Katayama, said “When we act, we will

act decisively.” Although the yen was back near levels that

triggered intervention in April and May recent verbal

warnings from the Minister were considered less

threatening than those ahead of the intervention earlier this

year.

Soichiro Tateishi, an economist at the Japan Research

Institute, suggested financial officials in Japan may have

assessed that intervention would not be very effective now

compared to the last time. The Finance Ministry spent a

total of almost ¥12 trillion to support the yen between

April 28 and May 27.

Recently the Bank of Japan (BoJ) lifted interest rates to

1%, the highest level since 1995, the first rate increase

since the end of 2025.

However, the BoJ’s decision did little to boost the yen as

the market had already fully priced in the decision,

according to analysts. Although exchange rates are not

within the BoJ’s policy target scope, currency fluctuations

are now more likely to affect prices compared to the past,

so exchange rates will be consider at future meetings, said

the BoJ Governor.

See:

https://www.japantimes.co.jp/business/2026/06/19/markets/yen-

market-june-19-2026/

Home mortgage holders face increased rates

Interest rates for Japan’s popular ‘Flat 35’ long-term

fixed-rate mortgages rose to 3.21% in June, raising the

hurdles to homeownership. Flat 35 is a commonly used

long-term fixed-rate mortgage loan in Japan with a

maximum term of 35 years, offered through a partnership

between private financial institutions and the Japan

Housing Finance Agency. In June, the minimum interest

rate for Flat 35 rose to 3.21%, surpassing the 3% level for

the first time in 17 years.

These rates are influenced by the Bank of Japan’s

monetary policy which is to raise the benchmark interest

rate gradually. At present, variable-rate mortgages are

roughly two percentage points lower than fixed-rate

mortgages. About 80% of mortgage borrowers choose

variable-rate mortgages.

Kobayashi Masahiro, a visiting researcher at the NLI

Research Institute, notes that “it is difficult to know what

lies ahead” with regard to short-term variable rates “now

that long-term interest rates are on the rise ahead of other

rates and inflation is expected to intensify, along with the

uncertainty about the situation in Iran.”

See: https://www.nippon.com/en/japan-data/h02807/

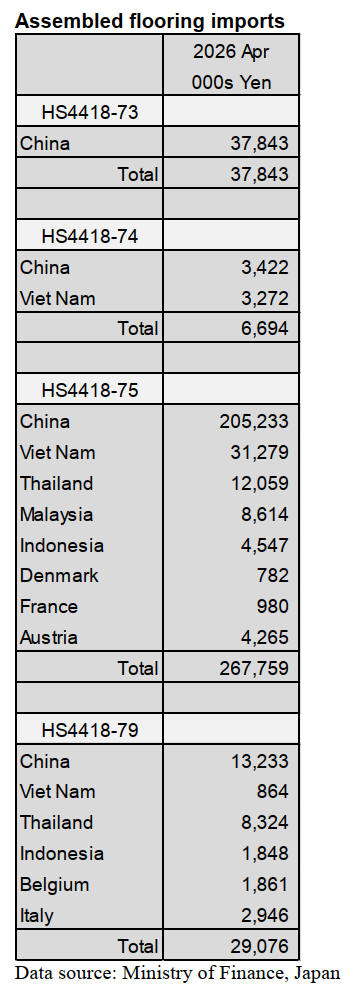

Import update

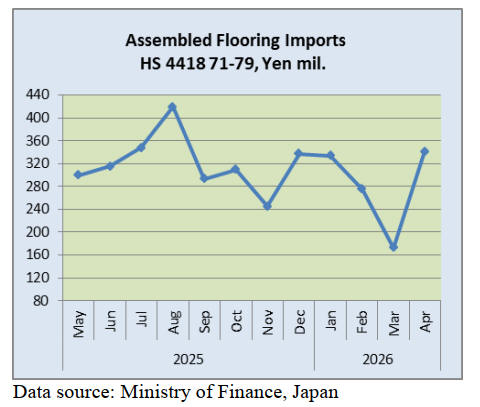

Assembled wooden flooring

In April 2026, shippers in China account for most of

Japan’s imports of assembled flooring and shipments. All

imports of HS4418-73 and 76% of HS4418-74 originated

in China, just 2% was from Austria. China was the main

shipper of HS4418-75 followed by Viet Nam and

Thailand. For HS4418-79 the main suppliers in April were

China and Thailand.

Imports of assembled wooden flooring (HS441871-79)

dropped sharply in February and March but there was a

significant upward adjustment in April and this was by

more than can be explained by the continual weakness in

the yen US dollar exchange rate.

Of the various categories of assembled flooring imports in

April, 76% was of HS4418-75 (63% in March),11% was

of HS4418-73 (23% in March), an almost halving of the

value of this category, 8% was of HS4418- 79, with the

balance being HS4418-73.

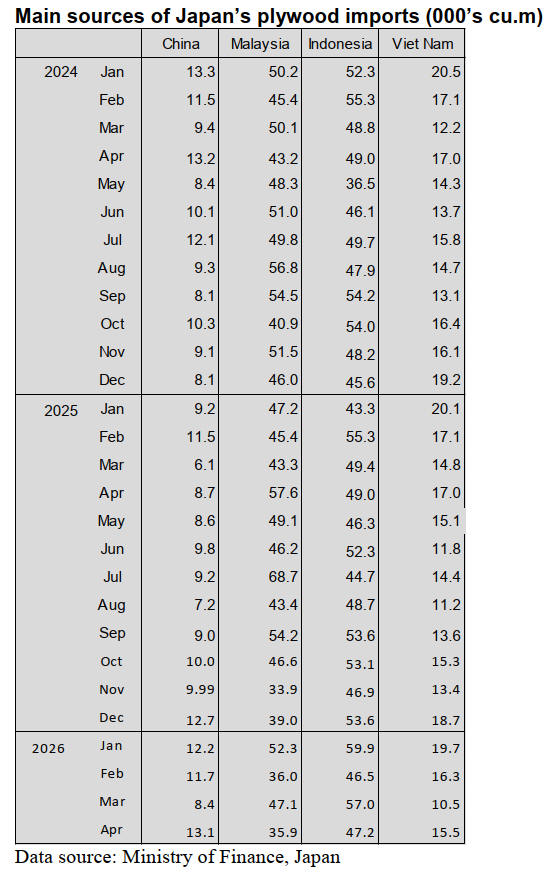

Plywood imports

The combined volume of shipments from the two main

shippers in April 2026 (Indonesia and Malaysia)

accounted for 72% of total imports (84% in March). April

shipments from Malaysia dropped compared to a month

earlier as did shipments from Indonesia.

The other main shippers of plywood to Japan in April

were Viet Nam and China. April arrivals from Viet Nam

were around 50% higher than in March and arrivals from

China were at 13,000 cu.m, the highest in the past 18

months.

In April 2026 arrivals of HS441210-39 were reported at

114,838 cu.m (123,896 cu.m in March). As in previous

months, of the various categories of plywood imported in

January 2026, HS4412-31 accounted for most (80%)

followed by HS4412-33(8.5%), HS4412-34 (6%) with the

balance being HS4412-39 and HS4412-10.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

Japan prepares shift to new training and employment

programme

The number of foreign technical trainees in the forestry

sector reached 127 roughly one year after the occupation

was added to Japan’s Technical Intern Training Program

in September 2024. Labor shortages remain severe in

western Japan, including Kyushu and Shikoku, and more

operators in regions such as Chugoku and Kanto are now

planning to accept new trainees. Japan’s Immigration

Services Agency reported that as of the end of 2025, the

forestry category counted 127 trainees and the wood-

processing category 541, up from 299 a year earlier,

showing steady nationwide growth.

Attention is now turning to the new “Training and

Employment Program,” which will replace the Technical

Intern Training Program and take effect on April 1, 2027.

Operational guidelines released in February outline a shift

toward securing a stable workforce.

The new program sets a standard stay of three years

(extendable to four), and workers who pass the required

skills and N4-level language tests may transition to

Specified Skilled Worker (i). It also allows worker-

initiated job changes and caps fees paid to sending

organizations. Regional areas will be permitted larger

intakes, and transitional measures will allow current

trainees to complete their existing terms.

Orders for house builders

Orders received in April by major housing manufacturers

and builders were generally strong, exceeding the levels

recorded in the same month last year. Although a few

companies posted slight year-on-year declines, some

reported increases of around 30 percent compared with the

same month last year.

In addition to higher per-unit prices pushing up overall

order values, some prospective homebuyers moved to

purchase earlier than planned due to uncertainty stemming

from instability in the Middle East. Orders at major

housing manufacturers and builders remained strong in

April, following solid results in March.

Adhesive shortages push up wood product prices

Amid a surge in demand for petroleum-based chemical

products triggered by the effective closure of the Strait of

Hormuz, adhesive suppliers have begun imposing price

hikes and supply restrictions on structural laminated

timber manufacturers. In response, manufacturers have

started moving to raise prices on shipments from May.

In western Japan, adhesive suppliers notified

manufacturers at the end of March that they would impose

volume restrictions on adhesives used heavily in softwood

plywood production. As a result, manufacturers were

already forced to cut output by April. As a result,

speculative buying by distributors worried about potential

shortages has tightened supply, prompting manufacturers

to begin raising prices.

Meanwhile, inquiries from distributors concerned about

potential supply disruptions prompted several structural

laminated timber manufacturers to state in mid-April that

adhesive supplies had not yet been restricted, mirroring the

situation seen in the plywood market. However, by late

April, adhesive manufacturers began issuing notices that

supply restrictions would be implemented.

Japan calls for stable housing-material supply

Japan’s METI, MLIT and the Forestry Agency have asked

distributors and homebuilders to help maintain a stable

supply of housing materials amid concerns over naphtha-

related product shortages. While key chemical supplies

remain generally stable the ministries warn that excessive

ordering could tighten the market.

They outlined three cooperation measures—ordering only

immediate-need volumes, improving communication

across the supply chain, and using a newly established

Housing Sector Information Desk. The government has

also launched a task force to secure critical materials

affected by Middle East developments.

Plywood

Prices for domestic plywood continue to rise as

manufacturers push through increases, with structural

panels leading since April. Middle East tensions have

raised costs for adhesives and other materials, and mills—

already struggling with weak markets— implemented

further hikes. Buyers, concerned about supply, continued

securing inventory, and by May structural plywood (12

mm, 3×6) settled around ¥1,300 per sheet, ¥200 higher

than in April. In June, major producers are seeking another

10%, pushing prices toward ¥1,400.

Imported tropical hardwood plywood from Indonesia and

Malaysia is also firm. While mills report no major

production issues, costs for adhesives, logs, coatings, and

freight continue rising.

Malaysian producers in Sarawak raised May offers by

about US$20 per m³ (C&F). Export prices have

strengthened, with coated formwork plywood at US$610–

630, formwork plywood at US$520–540, and structural

plywood at US$530–550. Indonesian ordinary plywood

trades around US$970–1,000 for 2.4 mm, with 3.7 mm at

US$880 and 5.2 mm at US$850.

Domestic prices remain on an upward trend. Coated

formwork plywood is around ¥1,920 per sheet, with some

deals at ¥2,000. Formwork plywood is

¥1,650–1,700, and structural plywood—still tight—is

centered around ¥1,700. Indonesian ordinary plywood

remains firm at ¥780 for 2.5 mm, ¥930 for 4 mm, and

¥1,150 for 5.5 mm.

Domestic logs and lumber

Prices of domestically produced lumber rose in May,

mainly for cedar items supplied to precutting plants. With

supplies tightening, sawmills have begun passing on

increases for cedar posts, studs, and 90 mm cedar and

cypress squares. Imported lumber and laminated cedar

posts—key competitors—had risen by about ¥5,000

between March and April, creating room for domestic

prices to move higher. From late 2024, precutting plants

and builders accelerated their shift from imports to

domestic materials, but for more than a year domestic

prices rose only to the lower end of competing imports.

This spring, as imported lumber increased again, domestic

lumber followed.

Cedar 105 mm KD premium posts for precutting plants

rose ¥2,000–4,000 to ¥55,000–58,000 per cubic meter,

while market prices at ¥57,000–60,000 now exceed

precutting plant levels once delivery costs are included.

Cedar KD premium studs increased ¥2,000–3,000 to

¥60,000–63,000.

Log prices show contrasting trends: cedar remains firm,

while cypress continues to weaken. In the Chugoku

region, cypress logs for posts and sills have found a

tentative bottom at ¥17,000 per cubic meter, though mid-

sized logs may fall below ¥16,000 depending on lamina

demand.

In Kyushu, cypress logs for posts remain at ¥17,000 and

sills at ¥17,500, narrowing the gap with cedar post logs at

¥16,000 and raising concerns about harvesting motivation.

Some areas in Shikoku have seen cypress sill logs fall to

¥16,000.

Cedar logs remain relatively resilient. In northern Kanto,

post logs fell ¥500 to ¥15,000 but remain ¥1,000 above

last year’s sharp decline. In Kyushu, cedar post logs stay

at ¥16,000, while mid-sized logs rose ¥500 to ¥15,500. In

Akita, mid-sized cedar logs remain unchanged at ¥15,000

|