|

Report from

Europe

EU tropical wood imports at a low ebb in the first

quarter of 2026

At a time when global supply conditions for tropical

hardwood products are very tight and the economic

outlook extremely uncertain, EU27 import volume during

the opening months of 2026 remained very low by long-

term historical standards.

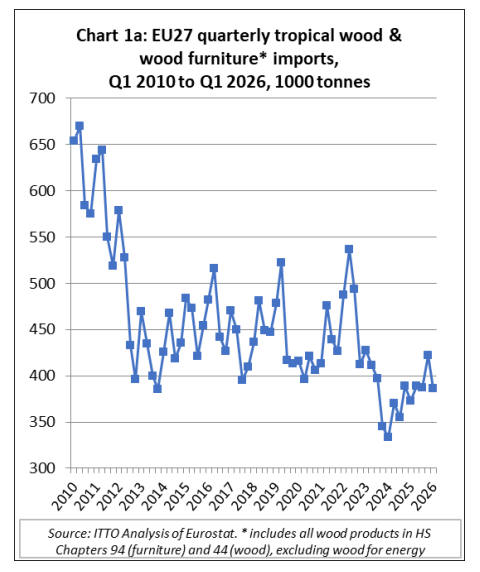

Imports of 386,000 tonnes of tropical wood and wood

furniture in the first quarter of 2026, while 4% more than

the same quarter in 2025, were down nearly 9% compared

to the previous quarter. (Chart 1a).

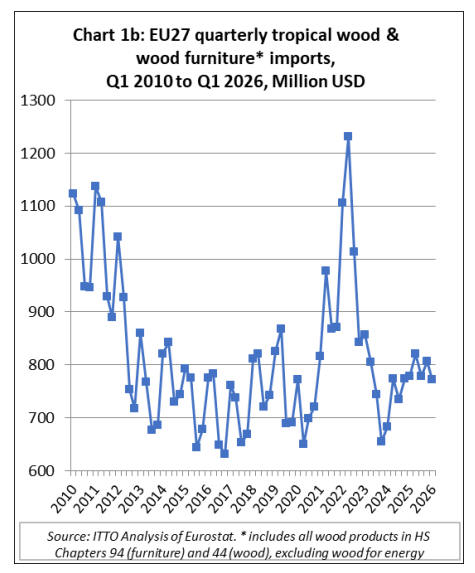

Total EU27 tropical wood and wood furniture import

value in the first quarter of 2026 was US$772 million, 1%

less than the same period last year and 4% down on the

previous quarter. In nominal terms (not accounting for

inflation), import value in the first quarter of 2026 was

more closely aligned with the pre-pandemic 2013-2019

period (Chart 1b). However, when inflation and exchange

rate changes are accounted for, the real value of EU

imports now is down around 30% compared to 2019.

Subdued European economy dampens demand

The wider European economic environment remained

subdued during the opening months of 2026. While

inflation continued to ease and household purchasing

power improved modestly, economic growth across the

eurozone slowed significantly amid weaker global trade,

persistent geopolitical tensions, and higher energy costs.

Preliminary Eurostat data shows that euro area GDP

increased by only 0.1% in the first quarter of 2026

compared to the previous quarter, down from 0.2% growth

in the final quarter of 2025.

Recent forecasts from major international institutions have

become increasingly cautious regarding the eurozone

outlook for 2026. The ECB’s latest macroeconomic

projections published in March 2026 reduced expected

euro area GDP growth in 2026 to 0.9%, while the OECD

lowered its 2026 euro area growth forecast to 0.8%.

Slow eurozone construction puts the brakes on wood

consumption

The weakness of the European construction sector

continues to be a particularly significant drag on demand

for timber and wood products. Forward-looking indicators

suggest that eurozone construction activity deteriorated

further during the first quarter and early second quarter of

2026. The S&P Global Eurozone Construction PMI fell

from 44.6 in March to 41.7 in April 2026, signalling the

sharpest contraction in construction activity since August

2024 and extending the current downturn in the sector to

four years. Any reading below 50 indicates contraction in

activity.

According to the latest survey data, the downturn was

broad-based across the eurozone construction sector, with

particularly weak performance in France and Germany.

Commercial construction activity recorded the steepest

decline, while residential construction and civil

engineering activity also remained firmly in contraction

territory. New orders weakened further amid elevated

financing costs, weak housing investment, rising energy

prices, and continuing economic uncertainty.

These conditions continue to weigh heavily on European

demand for tropical wood products, particularly higher-

value interior and construction-related product groups

such as furniture, joinery products, mouldings, and

decking. While imports of plywood and flooring products

increased strongly during the first quarter of 2026, overall

market conditions for tropical timber products in the EU

remained fragile.

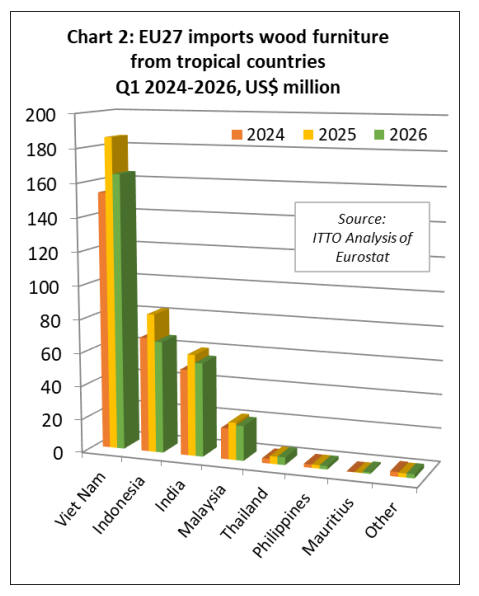

10% decrease in EU27 wooden furniture imports from

tropical countries in Q1 2026

The EU27 imported 76,000 tonnes of wooden furniture

from tropical countries with a total value of US$318

million in the first quarter of 2026. Import quantity and

value were down 10% and 12% respectively compared to

the same period in 2025.

In the first quarter of 2026, EU27 import value of wooden

furniture decreased from all major supply countries

including Vietnam (-11% to US$164.6 million), Indonesia

(-19% to US$66.9 million), India (-8% to US$56.1

million), and Malaysia (-7% to US$20.8 million).

However, there was a small 2% increase in imports from

Thailand to US$4.6 million (Chart 2).

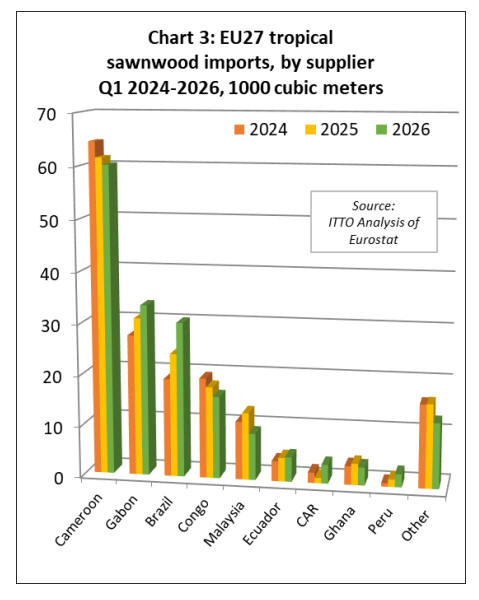

EU27 imports of tropical sawnwood just surpassed

record lows

The EU27 imported 176,000 cu.m of tropical sawnwood

with a total value of US$167.7 million in the first quarter

of 2026, respectively 1% and 5% more than the same

period in 2025 when imports were close to record lows.

Tropical sawnwood imports increased from Gabon (+8%

to 33,400 cu.m), Brazil (+25% to 30,200 cu.m), Peru

(+76% to 2,600 cu.m), and the Central African Republic

(+255% to 3,700 cu.m). However, imports declined from

the Republic of Congo (-10% to 16,100 cu.m), Malaysia (-

31% to 9,100 cu.m), Cameroon (-2% to 60,100 cu.m),

Ghana (-16% to 3,500 cu.m) and the Democratic Republic

of Congo (-35% to 1,200 cu.m) (Chart 3).

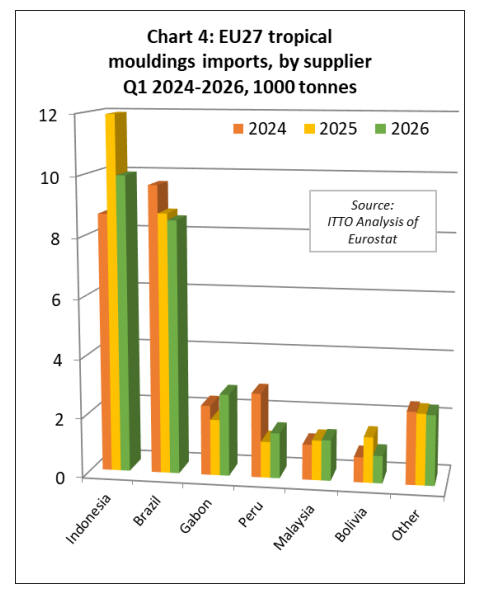

The EU27 imported 27,400 tonnes of tropical mouldings

and decking products with a total value of US$49.4

million in the first quarter of 2026, respectively 6% and

3% less than the same period in 2025. Imports declined

from Indonesia (-17% to 10,000 tonnes), Bolivia (-40% to

900 tonnes), and Brazil (-3% to 8,500 tonnes).

However, imports increased from Gabon (+46% to 2,800

tonnes), Peru (+26% to 1,500 tonnes), and Malaysia (+2%

to 1,400 tonnes) during the period (Chart 4).

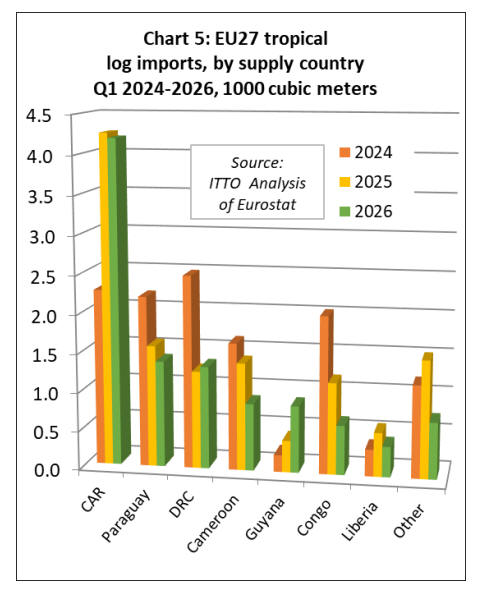

The EU27 imported 10,400 tonnes of tropical logs in the

first quarter of 2026, 15% less than the same period in

2025. Import value was stable at US$6.2 million.

Imports declined from Cameroon (-38% to 900 tonnes),

the Republic of Congo (-46% to 600 tonnes), Paraguay (-

13% to 1,400 tonnes), and Liberia (-31% to 400 tonnes).

However, imports increased from Guyana (+110% to 900

tonnes) and the Democratic Republic of Congo (+5% to

1,300 tonnes).

Imports from the Central African Republic, the largest

supplier during the quarter, were broadly stable at 4,200

tonnes (Chart 5).

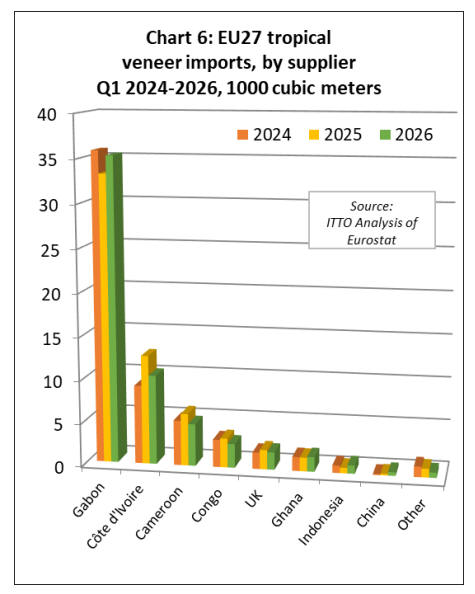

The EU27 imported 58,900 cu.m of tropical veneer in the

first quarter of 2026, 3% less than the same period in

2025. However, import value was up 7% to US$43.7

million.

Import quantity increased from Gabon (+6% to 35,300

cu.m), Indonesia (+53% to 1,000 cu.m), Ghana (+7% to

1,700 cu.m), and China (+140% to 400 cu.m). However,

import quantity declined from Côte d'Ivoire (-18% to

10,300 cu.m), Cameroon (-19% to 4,900 cu.m), the

Republic of Congo (-18% to 2,800 cu.m), and the UK (-

10% to 2,000 cu.m) (Chart 6).

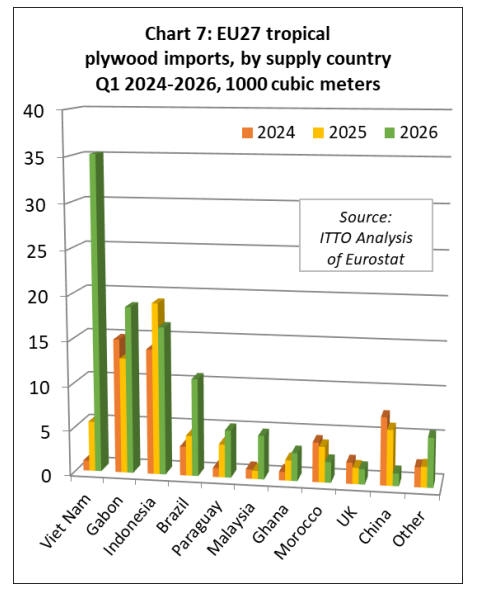

Sharply rising imports of tropical hardwood plywood

in response to anti-dumping measures

The EU27 imported 105,500 cu.m of tropical plywood

with a total value of US$67 million in the first quarter of

2026, up 67% and 48% respectively compared to the same

period in 2025.

This leap is driven primarily by Vietnam, from which

imports in the first quarter of this year, at 35,200 cu.m,

were up 528% compared to the same period in 2025. This

figure is all the more remarkable because it excludes an

additional 44,200 cu.m of plywood faced with non-tropical

hardwood species imported by the EU from Vietnam in

the same period, a rise from just 3,800 cu.m in the first

quarter of last year.

This is readily explained by the EU anti-dumping duties

on imports of hardwood plywood from China, set since 19

November 2025 at 86.8% for all products except those

from one company that provided additional information

during the EC investigation (set at 43.4% duty).

There were also significant gains in EU27 first quarter

imports of tropical hardwood plywood from Brazil

(+142% to 10,900 cu.m), Malaysia (+428% to 4,900

cu.m), Paraguay (+43% to 5,300 cu.m), Ghana (+37% to

3,100 cu.m), and Gabon (+45% to 18,600 cu.m). However,

imports declined from China (-77% to 1,400 cu.m),

Morocco (-42% to 2,300 cu.m), Indonesia (-14% to 16,500

cu.m), and the UK (-7% to 1,700 cu.m) (Chart 7).

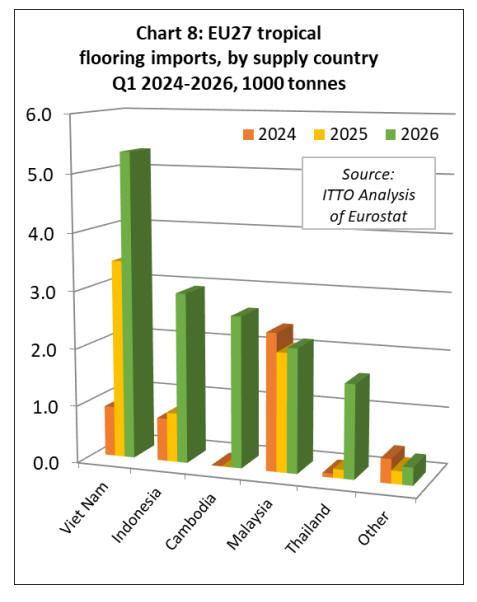

The EU27 imported 15,000 tonnes of tropical wood

flooring with a total value of US$40.3 million in the first

quarter of 2026, up 122% and 160% respectively

compared to the same period in 2025.

Imports increased from all major supply countries

including Indonesia (+244% to 3,000 tonnes), Vietnam

(+54% to 5,300 tonnes), Thailand (+951% to 1,600

tonnes), Malaysia (+4% to 2,200 tonnes), and Cambodia

which supplied 2,600 tonnes compared to negligible

imports during the same period in 2025 (Chart 8).

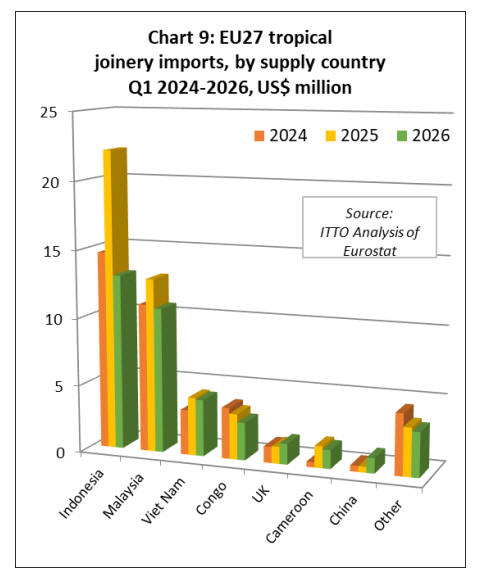

EU27 import value of other joinery products from tropical

countries - mainly laminated window scantlings, kitchen

tops and wood doors – was US$49.3 million in the first

quarter of 2025, 26% more than the same period last year.

Import quantity was up 31% to 21,800 tonnes in the same

period. Import value increased from Indonesia (+51% to

US$22.1 million), Malaysia (+17% to US$12.8 million),

and Vietnam (+29% to US$4.3 million).

EU import value of laminated joinery products increased

from Cameroon in the first quarter this year, rising 324%

to US$1.6 million. However, imports from the Republic of

Congo began this year more slowly than last, being down

11% at US$1.6 million. Indirect imports from the UK also

fell, by 2% to US$1.2 million (Chart 9).

Outlook for 2026

The first quarter trade figures suggest that the EU tropical

wood market remains fragile despite modest improvement

in some sectors. Gains in plywood and flooring imports

were offset by weaker demand for furniture and higher-

value secondary processed products. Much will depend on

whether the wider European economy and construction

sector recover more decisively during the remainder of

2026.

For now, the map of European growth in 2026 is being

redrawn around the southern and eastern periphery rather

than around the bloc's traditional industrial heartland.

Among the four largest eurozone economies, Spain is once

again the clear outperformer, with GDP growing 0.6%

quarter-on-quarter and 2.7% year-on-year in the first

quarter of 2026, slightly accelerating from 2.6% in the

fourth quarter of 2025.

The contrast with the rest of the eurozone heavyweights is

striking. Germany expanded just 0.3% year-on-year over

the same period, France 1.1%, and Italy 0.7%. Spain alone

is matching the United States on the annual measure.

Some countries in Eastern Europe are also performing

reasonably well economically this year, including Poland,

Bulgaria and Hungary, although it has to be said none are

traditionally significant markets for tropical wood.

Elsewhere, a lot is being pinned on expectations of a

strong recovery in Germany this year now that a massive

€500 billion infrastructure and climate package and €100

billion defence fund are being deployed. Real wage

growth and falling inflation are also expected to boost

household spending in Germany this year.

|