|

1.

CENTRAL AND WEST AFRICA

Sector continues to operate in a cautious environment

Market conditions remain largely unchanged with limited

new developments across the region. Activity levels are

steady but subdued and there are no major shifts in

demand or pricing trends. The sector continues to operate

in a cautious environment, with most developments linked

more to political and economic conditions than to market

fundamentals.

Large-scale infrastructure plans remain a key theme across

the region, including road construction, housing

developments, rail projects and healthcare investments.

However, a common issue persists, a lack of funding.

In Gabon, major office construction projects are

underway, including high-rise developments. At the same

time, infrastructure challenges remain significant. Parts of

the national road network are still in poor condition and

the withdrawal of an Indian contractor has further delayed

improvements.

The supply of electricity continues to be a major issue.

Cameroon is experiencing nearly daily power cuts, a result

of aging infrastructure and insufficient investment in

maintenance and upgrades. Similar challenges remain in

other countries across the region, affecting both industrial

operations and general economic activity.

Recent elections in the region have resulted in leadership

continuity which is seen as providing short-term stability.

In the Republic of the Congo, President Sassou is focusing

heavily on the country’s economic situation, including

increased pressure on companies to contribute more

actively to the national economy.

The forestry sector remains relatively quiet.The overall

outlook remains stable but subdued. With Chinese demand

is stirring operations are normalising but structural

challenges particularly in infrastructure, energy supply and

financing continue to limit growth.

Gabon

The market environment remains stable with gradual

improvements in demand. Sawmills are receiving

increased orders for Okoume, particularly from the Middle

East and China. The supply situation for Okoume logs has

improved with the GSEZ log park in Nkok now holding

sufficient volumes from multiple suppliers.

Operational challenges persist, particularly in inland

logistics. The main road between Okondja and Makokou

has been blocked for over two weeks due to local disputes

with villagers demanding compensation. More than 50

trucks are reportedly stranded and despite official

intervention, no resolution has yet been reached.

Outside of this disruption, road conditions in Central

Regions such as Lastourville and Lopé, are improving due

to ongoing repairs.

Transport times to Owendo Port are currently estimated at

two to three days provided routes remain open.

Infrastructure development remains a key focus. An

Australian company continues to advance plans for the

Baniaka iron ore project in southern Gabon. This includes

proposals for consideration of a new port between Port-

Gentil and Mayumba. However, the project remains at the

study and planning stage.

Container availability remains stable with no reported

shortages. Port operations are functioning under normal

conditions and there are no major disruptions in shipping

or handling.

In a major advance for forest sustainability and timber

traceability, Gabon officially announced the launch of a

national digital timber tracking system with GPS full-

chain tracing for every log from forest to the ports. This,

says SHD Timber, is set to reshape the standard of African

timber trade and bring more secure sourcing for global

buyers”.

See: https://www.shdtimber.com/gabon-launches-gps-timber-

tracking-new-era-for-african-timber-traceability.html

The fiscal environment remains challenging for operators.

Land tax payments were due by 21 March 2026 but many

companies are negotiating instalment arrangements due to

current market pressures, cash flow issues and the

implications of increased export duties on processed

timber.

Trade sources say their understanding is that export duties

will be as follows:

first transformation: increased from 7.5% to 15%

second transformation: increased from 5% to

10%

third transformation: (finished products such as

furniture): remains at 3%

Cameroon

Timber operations in Cameroon are gradually stabilising

with production activity increasing. Weather conditions

have improved with approximately two months of the dry

season remaining. This has allowed harvesting and

transport operations to increase.

Sawmill production is picking up but overall international

demand remains mixed depending on region and species.

Demand from the Middle East remains stable particularly

for redwood species such as Sapelli and for Iroko.

Vietnam continues to show strong demand while the

Philippines market remains weak. European demand is

still slow, especially for Padouk, Azobe and Ayous. Ayous

in particular is under pressure in markets such as Italy and

the Netherlands, largely due to competition from cheaper

Brazilian pine.

Container availability is not an issue with sufficient empty

containers available across the country. However,

operations at the Port of Douala remain under pressure

with congestion leading to vessel waiting times of more

than one week before berthing. This continues to impact

shipment planning and delivery schedules.

The outlook for the timber sector in Cameroon is

cautiously positive in operational terms, supported by dry

weather and the return of Chinese buyers. However, global

demand remains uneven and pressure from competing

materials, particularly Brazilian softwoods. continues to

affect key species such as Ayous. Port congestion and

political developments will remain important factors to

monitor in the coming months.

Republic of the Congo

Harvesting activity is improving supported by the gradual

return of Chinese demand. This has provided some relief

to operators after a slow period early in the year. However,

demand remains uneven across markets. The Philippines

continue to show weak interest in Okoume, while Vietnam

maintains solid demand for species such as Tali, Padouk

and Niové. The Middle East market remains relatively

quiet, particularly for sawn Okoume.

Transport conditions are improving as repairs continue on

laterite roads facilitating better movement from forest

areas to mills and export routes. Northern operators

continue to rely on transport corridors toward Douala Port,

while southern flows are directed toward Pointe-Noire.

Overall logistics are functioning, though still dependent on

seasonal conditions and road quality.

There are no major disruptions reported in milling

operations. The supply of spare parts, particularly for

logging machinery is stable and not considered a

constraint at this time.

Port operations remain steady. Pointe-Noire is functioning

without major issues and container availability is sufficient

with no reported shortages. Shipment flows are stable and

no significant disruptions have been noted in dispatch

operations.

No major new government regulations or policy changes

have been reported during this period. However, ongoing

compliance with CITES regulations and EUTR

requirements remains a key factor influencing trade flows

and operational practices.

The outlook for Congo is moderately positive, driven by

the return of Chinese demand and improved harvesting

conditions. However, overall market sentiment remains

cautious due to continued weakness in several key export

markets. Stability in logistics and port operations provides

a solid base but demand side uncertainty will continue to

shape the market in the coming months.

US$394 million to assist development of Congo Basin

forest economies

Cameroon, the Republic of the Congo and the Central

African Republic have secured US$394.83 million (about

224.06 billion CFA francs) in new financing from the

World Bank Group to develop sustainable forest

economies under the Congo Basin Forest Economic

Programme (SCBFEP) according to a press release from

the Bank.

The package, approved for Phase 1, is designed to improve

forest management, strengthen timber value chains and

generate an estimated 220,000 jobs across the three

countries.

According to the Bank the programme targets both supply-

side and market-side constraints in the forestry sector. It

will place nearly eight million hectares under sustainable

management, while increasing the share of legally

processed timber by 15%.

In parallel, more than 500 small and medium-sized

enterprises are expected to benefit from improved access

to finance, training and value-chain infrastructure,

alongside 20,000 individuals, of whom 40% are women.

The World Bank said the investment is structured to move

beyond conservation-only models by creating economic

conditions that make sustainable forest management viable

at scale. It integrates climate and livelihoods objectives,

with an expected reduction of 17.6 million tonnes of CO₂

equivalent in annual emissions. Marginalised

communities, indigenous populations and

“This new programme marks a milestone for the

Congo Basin, where sustainable forest economies create

jobs, raise incomes, and strengthen resilience for millions

of people," said Chakib Jenane of the World Bank

See:https://www.businessincameroon.com/public-

management/0604-15973-world-bank-allocates-cfa224bn-to-

develop-congo-basin-forest-economies-create-220-000-jobs

and

https://www.worldbank.org/en/news/press-

release/2026/04/01/transform-forest-economies-and-drive-jobs-

opportunities-for-60-million-people-around-the-congo-basin

2.

GHANA

Probing timber allocation concerns

A five-member Timber Allocation Audit Technical

Committee has been inaugurated at the Ministry of Lands

and Natural Resources (MLNR) to review timber

allocations made from 2017 to 2025. Chaired by the

Deputy Minister of MLNR, Yusif Sulemana, the

Committee was directed to begin work immediately due to

growing concerns over forest resource distribution.

Speaking for the Minister, the Chief Director of MLNR,

Innocent Marcus Haligah, called the audit “timely and

necessary,” emphasising that Ghana’s forest resources are

a critical national asset requiring transparent and

accountable management.

The Committee’s mandate is a comprehensive and

impartial audit focusing on legal compliance, identifying

irregularities in allocations and reviewing accountability

processes within the Forestry Commission.

The Chairman of the Committee pledged the team would

deliver, citing members’ experience and integrity. He

urged cooperation from the Forestry Commission and

other stakeholders, noting that access to information will

be essential for the committee’s work.

See: https://mlnr.gov.gh/lands-ministry-sets-up-committee-to-

probe-timber-allocation-concerns/

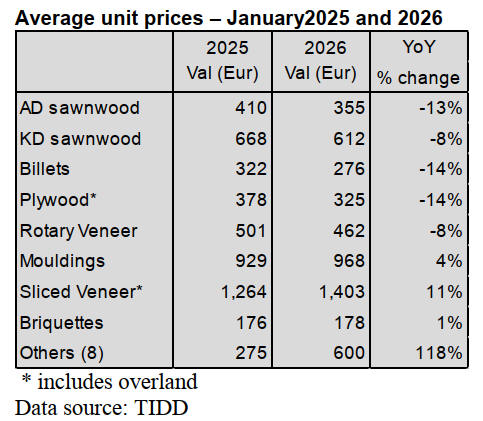

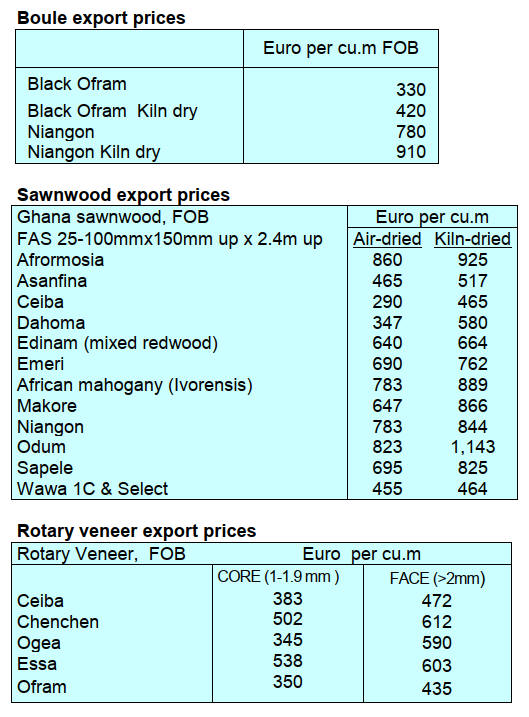

High average price for sliced veneer

The Timber Industry Development Division (TIDD)

Industry Report for January 2026 indicated that there was

drop in the average unit price (AUP) ranging from 8% -

14% for wood products shipped during the month. These

included major wood products such as rotary veneer, kiln-

dried sawnwood, plywood, billets and air-dried sawnwood

which recorded price decreases.

However, some products recorded significant increases in

average prices such as briquette (increased 1%),

mouldings (increased 4%) and sliced veneer (increased

11%). Countries that contributed to the increased demand

for these products included United Kingdom, Germany,

Estonia, Greece, Belgium and Croatia.

For the period the AUP for briquettes was up to

Eur178/cu.m compared to Eur176/cu.m in 2025. The main

destination for briquettes was the United Kingdom. The

volume of moulding export in January 2026 dropped by

18% to 309 cu.m and the export value was down by 15%

to Eur299,000. However the AUP rose by Eur39/cu.m to

Eur968/cu.m compared to Eur929/cu.m in 2025.

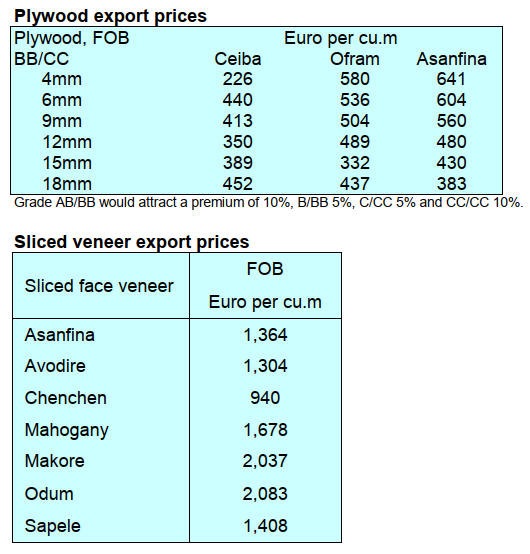

Exports of sliced veneer dropped 8% in January, from 704

cu.m (2025) to 647 cu.m (2026) but revenue increased

from Eur890,000 in 2025 to Eur908,000 in 2026. The

AUP increased from Eur264/cu.m in 2025 to

Eur1,403/cu.m in 2026. The main species of exported

veneer were asanfina, sapele, chenchen, koto and wawa.

Plywood export performance

Plywood remained one of the leading wood products

exported to regional and overseas markets in the first

month of 2026. Export volumes increased by 81% to 2,472

cu.m, from 1,369cu.m of the previous year with a

corresponding 55% increase in value for January 2026.

The United States and Gambia were the major consuming

markets of Ghana’s plywood in January 2026.

Notwithstanding, the export AUP for plywood declined

from Eur378/cu.m in January 2025 to Eur325/cu.m in

January 2026, a 14% decrease.

Wood products exports in January 2026 totalled 15,741

cu.m which earned the country Eur6.85 million. Compared

to January 2025 this resulted in decreases of 24% and 30%

in volume and value respectively.

Local timber sellers appeal for a more flexible permit

regime

Local timber sellers are calling on government for a more

flexible permit regime to facilitate the transport of timber

offcuts to support their business operations. Their

concerns are that the current permit system is restrictive

and affects their businesses making it difficult to move

offcuts efficiently.

According to the traders, the bureaucracy involved in

securing the statutory permits is frustrating and adds to the

heavy burden carried by traders. They have urged the

authorities to simplify permit process documentation to

support their small-scale timber businesses to strike a

balance between regulation and business growth.

In response to their concerns the Director of the National

Timber Monitoring Team, Alhaji Mohammed Kwaku

Doku, assured the woodworkers of government

implementing measures to strengthen the timber industry

that would enable them to contribute their quota to

national development.

See: https://www.modernghana.com/amp/videonews/634799

and

https://citinewsroom.com/2026/04/govt-implementing-measures-

to-strengthen-timber-industry-alhaji-doku/

Major step in national landscape restoration

The Forestry Commission has signed a Memorandum of

Understanding (MOU) with Terraformation Inc., a global

company specialising in biodiverse reforestation to restore

degraded mangrove ecosystems in the Keta Lagoon area

of the Volta Region of Ghana.

The partnership scales up the ongoing Keta Lagoon Blue

Carbon Project, also known as the Regenerative

Development of Anlo Wetlands (ReDAW) initiative.

Terraformation has worked in the area since 2021 with

local partners ReDAW Ltd., Agrointroductions Ghana,

landowners and communities to develop nature-based

solutions. The project targets thousands of hectares of

mangrove wetlands, aiming to sequester carbon, protect

biodiversity and strengthen coastal defenses against

erosion and flooding.

Under the deal, Terraformation will provide technical

expertise, training, technology and access to financing for

community-led restoration. The work is expected to create

jobs, particularly for women and youth, through mangrove

planting, aquaculture and beekeeping.

The Chairman of Forestry Commission (FC) Board, Isaac

Essien, described the project as a timely intervention for

Ghana’s forest degradation. While both the FC Chief

Executive Dr. Hugh C.A. Brown and Terraformation

President Jad Daley emphasised that the model aligns

ecological restoration with social and economic needs.

Meanwhile scientists from Ghana, Brazil and UK met in

Kumasi in the Ashanti Region of Ghana to discuss

tackling a biodiversity crisis with technology. The

workshop targeted postgraduate students, early-career

researchers and biodiversity conservation professionals to

introduce participants to a suite of emerging technologies

transforming conservation science, including Artificial

Intelligence (AI) for biodiversity monitoring, Species

Distribution Models (SDMs) and Environmental DNA

(eDNA) analysis.

See: https://www.modernghana.com/news/1482546/forestry-

commission-terraformation-partner-to.html

and

https://www.myjoyonline.com/scientists-from-ghana-brazil-and-

uk-gather-in-kumasi-to-tackle-biodiversity-crisis-with-cutting-

edge-technology/

3. MALAYSIA

Manufacturers face supply and energy crisis

The Malaysian manufacturing sector is facing a crisis due

to the Middle East conflict with nearly 90% of companies

reporting a direct impact or expected disruption within

four weeks as of early April 2026.

The crisis, characterised by shipping disruptions in the

Strait of Hormuz, rising energy costs and raw material

shortages has caused over 74% of manufacturing firms to

report production cost increases of at least 10%,

threatening the viability of small and medium enterprises

operating on thin margins.

The regional press has picked up on a press release from

the Federation of Malaysian Manufacturers (FMM) which

details the results of a recent survey which shows

Malaysian manufacturers are grappling with severe supply

chain and cost disruptions stemming from the ongoing

Middle East conflict and prolonged blockage of the Strait

of Hormuz and Red Sea shipping lanes.

The survey found that nine in ten companies are either

already affected or expect to be within four weeks, with

raw material shortages, skyrocketing logistics costs and

tightening diesel supplies threatening production

continuity. Sectors producing food, household goods,

packaging, chemicals and consumer products are

particularly exposed, raising the risk of product shortages

and export disruptions.

Production lines are at risk of stoppage, export orders are

being cancelled and the financial capacity of

manufacturers to sustain operations is under direct and

accelerating pressure, said FMM.

It noted that Malaysia's manufacturing relies heavily on

global supply chains, with 83% of companies sourcing

over 30% of raw materials from overseas.

Disruptions across energy, freight, fuel and materials are

affecting domestic supply chains, with knock-on effects on

retail availability and consumer prices. ven if the conflict

ended immediately, delays in restocking, insurance costs

and contract renegotiations would continue to strain

operations for months, according to the survey.

The survey highlighted that 69.5% of manufacturers

expect raw material shortages within a month, while 8%

have less than two weeks of critical stock. Plastics,

specialty chemicals, metals, food additives and rubber

processing inputs are among the most affected, creating

the potential for halted production in essential consumer

goods and industrial products.

Energy and logistics costs have also surged, compounding

operational stress. Nearly half of respondents reported

industrial energy costs rising by 10 to 30%, while 22%

said increases reached 30 to 50% and 12% experienced

hikes above 50%.

Freight and logistics costs have also escalated sharply,

with 53% of firms reporting 20 to 50% increases and 18%

seeing costs jump more than 50%, often outside contract

terms. Diesel shortages for domestic haulage further delay

cargo movement and elevate transport costs.

The impact on output is already visible, 48% of companies

have reduced production or suspended lines, while 52%

are facing export disruptions including delayed shipments,

order cancellations and buyer-initiated renegotiations.

FMM has said “the scale and breadth of disruption

highlighted in this survey requires an immediate and

coordinated Government response. The risk of production

stoppage and export contraction is real and the window to

prevent it is narrowing. FMM has identified twelve

recommendations and calls on the Government to act on

all of them without delay. They span fiscal and tax relief,

energy and fuel supply, raw materials and supply chain

security and logistics, ports, shipping and crisis

governance”.

See: https://www.fmm.org.my/Articles/Details/Press-@-

FMM_Press_Statement-

;_FMM_SURVEY_CONFIRMS_MALAYSIAN_MANUFACT

URING_FACES_ESCALATING_RISKS_FROM_WEST_ASI

A_CONFLICT/c72623f9-42d1-4e37-9ace-f4f44d95d88e

and

https://english.news.cn/20260407/79929e0493cd40f7bf8ba0701e

37c4f9/c.html

Sarawak Timber Association calls for government

support

The Sarawak Timber Association (STA) has appealed to

the government to consider support measures as the

industry continues to face mounting cost pressures and

regulatory challenges amid a volatile global economic

environment.

STA chairman, Henry Lau, said this includes a review of

royalty, cess and premium charges as well as targeted

assistance to both upstream and downstream operations

during the current period of sustained cost pressures.

When delivering his report on the Workings of STA for

2025 at the STA AGM Lau stressed that geopolitical

tensions, particularly ongoing conflicts in the Middle East,

have pushed up global oil prices and created energy

market volatility, resulting in higher diesel costs, a key

component in logging, extraction, transportation and

processing activities.

“These increases have pushed up operating costs across

the value chain, especially in fuel-intensive activities.

Some operators have had to scale down or suspend

operations and there are growing concerns that parts of the

industry may struggle to recover if these conditions

persist,” said Lau.

He noted last year was challenging for the industry, with

annual log production staying low at 1,930,351 cubic

metres. Downstream production also continued to decline,

with plywood output falling sharply from about three

million cubic metres in 2008 to approximately 550,000

cubic metres last year.

Production from planted forests also dropped significantly

from 1,903,526 cubic metres in 2024 to 540,323 cubic

metres in 2025, which he attributed to the cancellation of

Licence for Planted Forest (LPF) without due process.

See:

https://theborneopost.pressreader.com/article/281487872894850

Advance through innovations

According to the Sabah State Minister of Education,

Science and Technology, James Ratib, Sabah must adopt

modern technology and innovation to ensure its timber

industry remains competitive in the global market. He

added that the timber industry has long been a backbone of

Sabah’s economic growth but can no longer rely solely on

traditional practices.

“In today’s era of globalisation and rapid technological

advancement, a paradigm shift is necessary through the

application of modern technology and creative innovation

to ensure our downstream timber products remain

competitive,” James said.

With the adoption of the latest technologies the Minister

said he is confident the industry can grow rapidly,

contribute positively to the State’s economy and create

more job opportunities for the people of Sabah. James

expressed confidence that, with strong support from

educational institutions and industry partners, students

would emerge as future experts and leaders in the timber

sector.

See:

http://theborneopost.pressreader.com/article/281479282975340

4.

INDONESIA

Processed Wood

Processed wood products which are leveled on all four

sides so that the surface becomes even and smooth with

the provisions of a cross-sectional area of 1,000 sq.mm to

4,000 sq.mm (ex 4407.11.00 to ex 4407.99.90)

Processed wood products which are leveled on all four

sides so that the surface becomes even and smooth of

Merbau wood with the provisions of a cross-sectional area

of 4,000 sq.mm to 10,000 sq.mm (ex 4407.11.00 to ex

407.99.90) US$1,500/cu.m

See: https://jdih.kemendag.go.id/peraturan/keputusan-menteri-

perdagangan-republik-indonesia-tentang-harga-patokan-ekspor-

dan-harga-referensi-atas-produk-pertanian-dan-kehutanan-yang-

dikenakan-bea-keluar-dan-tarif-layanan-badan-layanan-umum

Almost US$750,000 potential deals at Budapest fair

Indonesian furniture and home décor products generated

potential transactions worth almost US$750,000 at the

Home Design Exhibition in Budapest reflecting rising

demand in Central and Eastern Europe.

The Indonesian Trade Promotion Center (ITPC) in

Budapest highlighted strong interest from Hungarian and

regional buyers pointing to growing trust in Indonesian

craftsmanship and design.

Four Indonesian MSMEs participated in the March 25–29

event, showcasing a diverse range of products including

teak wood furniture with traditional Javanese carvings,

contemporary premium designs, copper and fossilised

wood décor and innovative mycelium-based furniture that

blends local materials with European aesthetics.

See:https://rri.co.id/en/business/2313459/indonesian-msmes-

shine-at-home-design-2026-in-budapest

Proposal for global distribution hubs

The Indonesian Furniture Industry and Craft Association

(HIMKI) has suggested the establishment of marketing

and distribution hubs. HIMKI Chairman, Abdul Sobur,

pointed out that conflicts, such as in the Middle East,

disrupt supply chains, cause shipping delays and

undermine buyer confidence creating structural shifts

demand beyond normal market fluctuations. He stressed

that industrial resilience now depends not just on

production capacity but on the ability to adapt to global

uncertainty.

To address these challenges, HIMKI is focusing on

diversifying export markets and developing alternative

distribution channels. Key initiatives include establishing

hubs in Europe, the United States and Canada to shorten

supply chains, improve market access and boost the

competitiveness of Indonesian products.

Sobur emphasised that these efforts require government

support through policy, financing and trade diplomacy.

HIMKI views the current global pressures as an

opportunity to build a more resilient, flexible and risk-

adaptive industrial system.

See: https://www.antaranews.com/berita/5512425/himki-dorong-

pengembangan-hub-distribusi-sikapi-dinamika-global

and

https://www.merdeka.com/uang/himki-dorong-hub-distribusi-

global-perkuat-ketahanan-industri-mebel-hadapi-dinamika-

geopolitik-558873-mvk.html

Indonesia, Japan to boost forestry and carbon trading

cooperation

Indonesia and Japan have agreed to strengthen their

bilateral cooperation in forestry and climate-related sectors

according to Indonesia’s Forestry Minister Raja Juli

Antoni. The partnership will focus on initiatives such as

sustainable forest management, carbon trading and

wildlife conservation.

The collaboration also aims to enhance conservation areas,

promote knowledge exchange and increase private sector

participation in the carbon economy. Indonesia is offering

investment opportunities through its Carbon Economic

Value (NEK) scheme and voluntary carbon trading

programmes.

The collaboration will be supported by projects with the

Japan International Cooperation Agency (JICA), including

the deployment of Japanese experts to assist in mangrove

management. Indonesia also encouraged further

collaboration through the development of the World

Mangrove Center and the implementation of the Joint

Crediting Mechanism (JCM) scheme to advance shared

climate goals.

See: https://en.antaranews.com/news/410669/indonesia-japan-to-

boost-forestry-and-carbon-trading-cooperation

and

https://en.antaranews.com/news/410502/indonesia-jica-deepen-

forestry-partnership-to-support-climate-action

Carbon and social forestry project integration

Indonesia is strengthening cooperation on carbon projects

and social forestry through a strategic partnership with the

Asia Forest Cooperation Organization (AFoCO). The

Minister of Forestry, Raja Juli Antoni, met AFoCO

Executive Director, Park Chongho, in Seoul to discuss

collaboration in carbon project development, land

rehabilitation and community empowerment under social

forestry programmes.

The initiative is part of Indonesia’s broader “green

diplomacy” agenda and focuses on preparing carbon

projects and certification in national parks and concession

areas.

AFoCO praised Indonesia’s active participation since

joining the organisation in 2019 and highlighted

opportunities for international financing through its

accreditation under the Green Climate Fund.

To strengthen coordination, Indonesia proposed placing a

permanent representative at AFoCO headquarters and

invited the organisation to support the management of 1.4

million hectares of Indigenous Forests, as well as improve

early-stage funding access for social forestry communities.

See: https://www.metrotvnews.com/read/KZmCQovG-proyek-

karbon-dan-perhutanan-sosial-di-indonesia-diperkuat

and

https://www.agrofarm.co.id/2026/04/kemenhut-gandeng-afoco-

dorong-pengembangan-proyek-karbon-dan-perhutanan-sosial/

APHI reinforces dedication to sustainable forest

management

The Association of Indonesia Forest Concession Holders

(APHI) has reaffirmed its commitment to promoting

sustainable forest management, highlighting the forestry

sector’s vital role in supporting sustainable development.

APHI Chairman, Soewarso, noted that the Association is

dedicated to expanding forest cover through planting and

enrichment in both plantation and natural forests while

ensuring responsible utilisation.

He also stressed that optimising forest use through a multi-

business forestry approach, strengthening governance,

enhancing collaboration with the government and

stakeholders and fostering innovation are key strategies for

ensuring sustainable forest management now and in the

future.

See: https://www.antaranews.com/berita/5516560/aphi-perkuat-

komitmen-jaga-kelestarian-hutan

Indonesia, South Korea - strategic ties on forest fire

response

Indonesia and South Korea have agreed to deepen

strategic cooperation in forestry, with a strong focus on

sustainable forest management and forest fire response.

The partnership was formalised through the signing of two

key agreements in Seoul between Indonesia’s Minister,

Raja Juli Antoni and Korea Forest Service Minister Park

Eunsik.

The first agreement outlines collaboration on priority

forestry programmes including climate change mitigation,

mangrove and peatland rehabilitation, ecotourism

development, social forestry and strengthening forest

carbon markets. The second agreement specifically

addresses forest fire management and post-fire recovery,

promoting cooperation in prevention, preparedness,

response and recovery efforts.

See: https://rri.co.id/en/international/2306924/indonesia-and-

korea-boost-strategic-cooperation-in-forest-fire-management

Economic fundamentals steady despite global

pressures

Indonesia’s economic fundamentals remain strong despite

global challenges supported by steady growth of around

5%, controlled inflation and a consistent trade surplus.

Annual inflation reached 3.48% in March 2026 while the

country recorded a US$1.27 billion trade surplus in

February extending a streak of 70 consecutive months.

These indicators reflect stable economic performance and

solid external balances amid ongoing global uncertainty.

To sustain this momentum and avoid the middle-income

trap the government is implementing a targeted

development strategy focused on five priorities: improving

labour productivity through investments in education,

healthcare and social protection; expanding infrastructure

to enhance basic services and strengthen food and energy

security; advancing institutional reforms for more

effective governance; ensuring adaptive macroeconomic

policies; and maintaining political and security stability.

The government also emphasises prudent fiscal and

monetary management to preserve investor confidence,

with credibility seen as a key factor in successfully

executing these policies.

See: https://en.antaranews.com/news/411681/indonesias-

economic-fundamentals-steady-despite-global-pressures

5.

MYANMAR

6.

INDIA

Associations across India issue a flurry

of price

advisories

The Iran-US conflict has compelled Indian wood panel

producers to reorganise their production and sales targets

as costs rise. In a rapidly evolving and complex situation

with no endgame in sight oil prices have shot above

US$110 per barrel following the choking at Strait of

Hormuz. India’s methanol supply is among the hardest-hit

chemicals followed by PVC resin, Acrylic monomer and

imported urea.

India imports about 1.3 million tonnes of methanol

annually of which around 40% comes from the Arabian

Gulf, Iran itself is one of the world’s largest producers and

exporters of methanol and supply through the Strait of

Hormuz accounts for 30% of global methanol trade.

The conflict has disrupted shipping routes, creating

significant uncertainty in Methanol and Urea supply,

which is a critical source for wood panel decorative and

related polymer sheet industries in India. So far the cost of

producing almost every wood panel product and

decorative interior and exterior product has increased. The

rise in the production cost of plywood is estimated to be 4-

6%. Production costs for MDF and particleboard have also

risen around 5% .

Against the backdrop of developments in West Asia the

Federation of Indian Plywood and Panel Industry, South

Indian Plywood Manufacturers Association, North

Malabar Plywood & Doors Manufacturers Association

have written to Ministry of Commerce and Industry and

Department for Promotion of Industry and Internal Trade

(DPIIT) requesting a reduction in the basic Customs duty

(BCD) on key chemical imports such as Technical-grade

urea, Phenol, Melamine, Methanol used in Resin

manufacturing for plywood, MDF, particle board,

laminates and other panel products.

Various plywood and timber associations across India

have issued a flurry of price advisories in the wake of

ongoing tensions between US-Israel and Iran. It is

inevitable that manufacturers will be compelled to increase

panel prices.

The Kandla Timber Association (KTA) has advised

plywood and veneer industries to implement price

adjustments and readjust their commercial decision taking

into account current market conditions and the impact on

raw material prices.

According to the KTA, in view of the current ongoing

geopolitical situation in the Middle East, the overall cost

structure has increased by roughly 8-10% due to

significant uncertainty in the global supply chains and

freight movement and raw material supply stability.

The Haryana Plywood Manufacturers’ Association

(HPMA) has issued a trade advisory to all members in

response to the volatility in raw material import prices

amidst conflicting situations in the Middle East.

The HPMA has said the plywood industry is presently

facing a significant increase in the cost of major raw

materials including Phenol, Formaldehyde, Urea,

Melamine, Face Veneer and Core Veneer. The ongoing

conflict situation in West Asia has also disrupted global

supply chains leading to volatility and irregular

availability of several key inputs. In the face of such

developments the manufacturing cost of plywood products

has increased by around 6 %.

The Punjab Plywood Manufacturers Association (PPMA)

also suggested a price increment of 5% on the plywood

citing increased raw material cost. The Association noted

that, due to the steep increase in prices of various inputs

like timber, Formaldehyde and phenol plywood mills are

running at a loss and the viability of factories has come

under pressure.

The Wood Based Industries Association of Uttar Pradesh

has declared an increase in the price of all wood panel

products of 6% with immediate effect due to the sharp rise

in prices for raw material. The Association also cautioned

all the members to revise their prices accordingly to save

the wood panel industry from further damage.

The Rajasthan Plywood Manufacturers Association

decided to increase prices of Board and Flush Door by

Rs.24 per square foot. Whereas a 5% price increase in the

prices of plywood has been implemented in view of the

sudden increase in the prices of chemicals (Formaldehyde,

Phenol, Melamine), Face Veneer, Pine Raw Board and

Pine timber due to international circumstances.

The Particleboard Manufacturers Association of Kerala

(PBMAK) has decided to implement a price revision for

particleboard in order to sustain production quality and

ensure uninterrupted supply to the market. The PBMAK

noted that manufacturers have been facing continuous cost

increases due to global supply chain disruptions and rising

input costs.

Despite sustained efforts by manufacturers to absorb these

increases, the situation has now reached a point where a

price revision has become unavoidable.

The Gujarat Particle Board Association has suggested at

least a 15% hike on existing product prices due to the

shortage of raw materials and the continuous increase in

production costs mainly caused by the rise in prices of

resin, wood and paper raw materials.

The All India Decorative Veneer Manufacturers

Association issued an advisory on the ongoing challenges

arising from global market changes, the weakening rupee

and rising operational and overhead costs. Based on their

estimate a 12% increase should be implemented

immediately.

The Indian Laminate Manufacturers Association has

issued an advisory because the price of several raw

material used in laminate manufacturing has been

significantly increased. The prices for different varieties of

laminates will be increased in the range of INR35 to 70

per sheet.

The All India Edge band Manufacturers Association also

issued an advisory on price increases due to ongoing

Middle East conflict which has resulted in a shortage of

raw materials used in manufacturing of edge bands. In the

current scenario, members are advised to increase the

prices of edge bands by a minimum 15%.

Conflict could drive down GDP

India‘s real GDP growth for the next fiscal year could be

eroded by around 1 percentage point, while retail inflation

could rise by about 1.5 percentage points from the baseline

estimates if the Middle East conflict persists through the

next fiscal year says a report from a member firm of Ernst

& Young Global Limited (EY).

The EY Economy Watch report said that several sectors,

including employment-intensive sectors like textiles,

paints, chemicals, fertilisers, cement and tirescould be

directly impacted. Any reduction in employment or

incomes in these sectors may further dampen demand.

The report points out the Indian economy, which relies on

nearly 90% of its crude oil imports, is also highly

dependent on imports of natural gas and fertilisers and is

particularly vulnerable to such external shocks.

The ongoing conflict in the Middle East has significantly

disrupted global crude oil and energy markets. Even if the

conflict is resolved in the near term some of these

disruptions may take considerable time to normalise, it

said. The Organisation for Economic Cooperation and

Development (OECD) had only recently projected India‘s

GDP growth to moderate to 6.1% from 7.6% in the current

financial year.

See: https://www.ey.com/en_in/services/tax/economy-watch

and

https://economictimes.indiatimes.com/news/economy/indicators/i

ran-war-shock-middle-east-conflict-could-cut-1-ppt-from-indias-

fy27-gdp-outlook/articleshow/129920336.cms?from=mdr

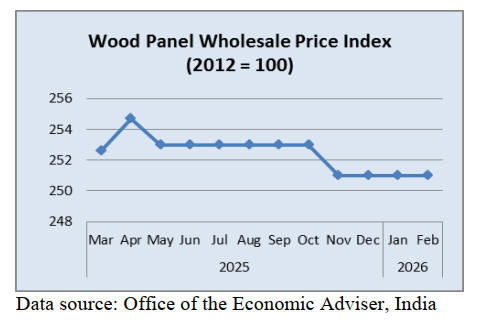

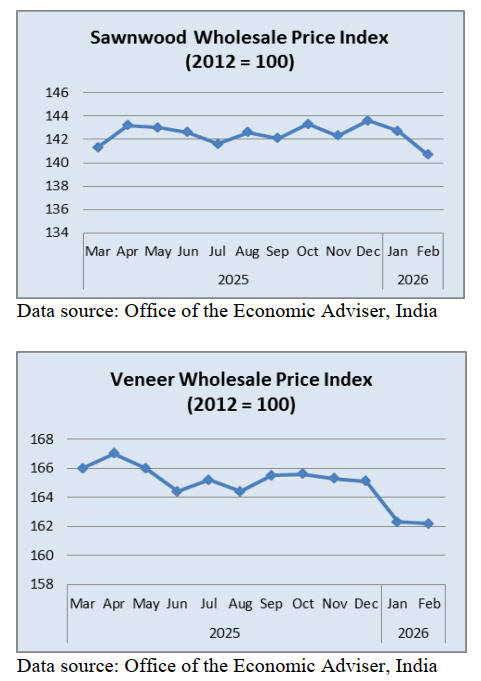

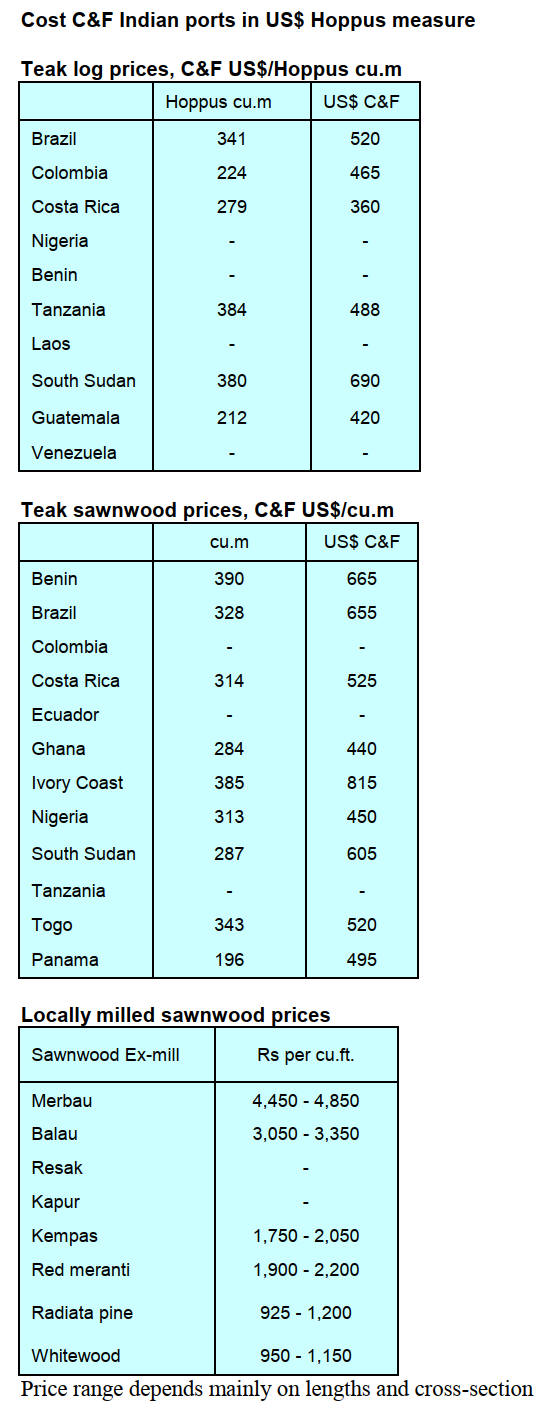

Sawnwood wholesale price nosedives

The annual inflation based on the February WPI was

2.13% (1.81% in January), the positive rate in February,

2026 was primarily due to increased prices for‚ other

manufacturing, manufacture of basic metals, non-food

articles, food articles and textiles.

The index for Manufactured Products rose from 147.5 in

January to 148.2 in February 2026. Out of the 22 NIC two-

digit groups for Manufactured Products, 16 witnessed an

price increases and 5 groups witnessed a decrease in

prices.

Some of the groups that showed month on month increases

in prices were‚ other manufacturing, manufacture, of food

products, textiles; manufacture of electrical equipment and

chemical and chemical products.

Some of the groups that recorded a decrease in price in

February were manufacture of basic metals, computer,

electronic and optical products, fabricated metal products,

except machinery and equipment, wood and products of

wood and cork and leather and related products.

See: https://eaindustry.nic.in/

and

chrome-

extension://efaidnbmnnnibpcajpcglclefindmkaj/https://eaindustry

.nic.in/pdf_files/cmonthly.pdf

7.

VIETNAM

Wood and wood product (W&WP) trade

highlights

According to data provided by Viet Nam Customs Office,

Viet nam’s W&WP exports in March 2026 reached

US$1.15 billion, up 19% compared to February 2026 but

down 22% compared to March 2025.

Of the total the WP export share was US$760 million, up

27% compared to February 2026 but down 25% compared

to March 2025.

In the first 3 months of 2026 W&WP exports earned

US$3.7 billion, down 5% over the same period in 2025 of

which WP exports were valued at US$2.4 billion, down

10% over the same period in 2025.

Viet nam’s W&WP exports to the EU in March 2026

earned US$92 million, up 24% compared to February

2026 and up 61% compared to March 2025. In the first 3

months of 2026 W&WP exports from Viet Nam to the EU

earned to US$252 million 57% over the same period in

2025.

Viet nam's poplar wood imports in March 2026 were

42,100 cu.m, worth US$14.7 million, up 21% in volume

and 25% in value compared to February 2026. Compared

to March 2025 an increase of 46% in volume and 24% in

value was observed. In the first 3 months of 2026 imports

of poplar wood were estimated at 107,200 cu.m, worth

US$37.9 million, up 51% in volume and 36% in value

over the same period in 2025.

Viet nam's imports of raw wood (logs and sawnwood)

in

February 2026 amounted to 381,400 cu.m, worth

US$128.7 million, down 39% in volume and 39% in value

compared to January 2026 and down 17% in volume and

12% in value compared to February 2025. In the first 2

months of 2026 Viet nam's imports of raw wood reached

1.0 million cu.m, worth US$338.1 million, up 16% in

volume and 24% in value over the same period in 2025.

NTFP exports in March 2026 earned around US$80

million, up 44% compared to February 2026 and 2.0%

over the same period in 2025. In the first 3 months of

2026, NTFP exports generated US$235.66 million, up

13% over the same period in 2025.

Plywood redirected to Middle East and South Asia

US tariff pressures and anti-dumping duties accelerated

plywood trade diversification toward the Middle East and

South Asia where construction is booming.

Tariffs on plywood have grown more complex. While

plywood (HTS 4412) was exempted from Section 232

duties it was not excluded from the reciprocal tariff regime

that took effect in April 2025. Vietnamese goods currently

face a 20% reciprocal tariff on US-bound shipments,

reduced from the initial 46% announced in April 2025

through bilateral negotiations concluded in August 2025.

Layered on top are the preliminary anti-dumping duties of

191.85–194.80% and countervailing duties announced in

March 2026 on hardwood and decorative plywood from

Viet Nam with final determinations scheduled for May 11,

2026.

Middle East construction absorbs redirected supply

As access to the US market becomes prohibitively

expensive for Viet namese hardwood plywood exporters

the Middle East has emerged as a critical alternative

destination. Saudi Arabia's construction sector, valued at

US$104.8 billion in 2024 and growing at 8.7% compound

annual rate toward US$174.4 billion by 2030, is the

region's demand anchor.

The kingdom imported US$2.5 billion in wood products in

2023 and envisions 1.5 million new homes by the end of

the decade.

Formwork plywood is particularly well-positioned in this

market. According to PS Market Research, Saudi Arabia's

wooden formwork systems market reached US$94.4

million in 2024, with plywood holding approximately 50%

market share. The UAE adds further scale, importing

US$2.4 billion in timber products annually. Both markets

are structurally import-dependent domestic production

covers only a fraction of demand from mega-projects like

NEOM, The Red Sea development and Abu Dhabi's

infrastructure expansion.

For Viet namese exporters of film-faced formwork

plywood for construction, this demand profile creates an

opportunity to redirect capacity from tariff-constrained US

routes toward markets where duty-free or low-duty access

combines with genuine infrastructure-driven demand

growth.

India's plywood market, valued at INR247.85 billion

(US$29.5 billion) in 2025 according to IMARC Group, is

projected to grow at a 5% compound annual rate through

2034 reaching INR391.90 billion. The construction sector

is the dominant consumer.

Freight costs add margin pressure

Logistics costs are compounding the trade route

restructuring. The Drewry World Container Index held

steady at US$2,287 per 40-foot container as of 2 April

2026 but the headline number masks emerging pressure

points.

Maersk has applied to US regulators for an emergency

bunker surcharge of US$200 per TEU on head-haul routes

and US$100 per TEU on backhaul, citing elevated fuel

costs from tensions in the Strait of Hormuz, a chokepoint

handling nearly 20% of global oil shipments.

For wood product shipments from Southeast Asia these

surcharges directly impact landed costs. A typical

plywood shipment of 25 cubic metres in a 20-foot

container absorbs the surcharge as a per-unit cost increase

of approximately US$8/cu.m for thin-margin commodity

grades but manageable for higher-value film-faced and

formwork panels.

See: https://vinawoodltd.com/blog/plywood-timber-market-brief-

april-2026

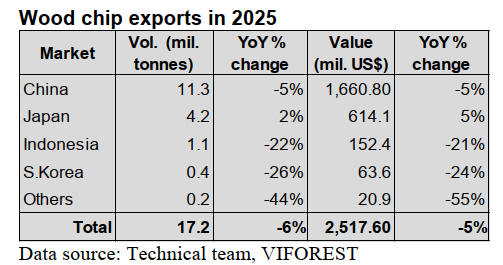

Viet nam’s wood chip exports in 2025

In 2025, Viet Nam exported 17.2 million tonnes of wood

chips, generating US$2.5 billion, down 6% in volume and

5% in value compared to 2024. Despite the decline, wood

chips still accounted for approximately 15% of the total

exports of the wood industry.

This highlights the continued importance of wood chips in

Viet nam’s wood sector while also reflecting the impact of

international market fluctuations, particularly the decline

in demand from China’s paper industry.

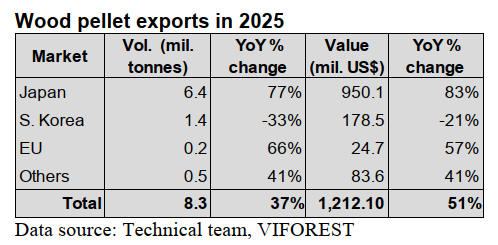

Viet nam’s wood pellet exports

Viet Nam exported nearly 8.3 million tonness of wood

pellets reaching US$1.2 billion in 2025, up 37% in volume

and 51% in value compared to 2024. The export value of

this product now accounts for approximately 7% of the

total exports of the wood industry.

Despite certain challenges in raw material supply, 2025

witnessed strong growth in both export volume and value

of wood pellets. This was driven in particular by surging

demand from Japan, as biomass co-firing power plants

participating in the new FIT/FIP mechanisms came into

operation.

8. BRAZIL

Framework for the use of native forest

biomass

The State of Mato Grosso located in the Amazon Region

has established an innovative regulatory framework for

regulating and certifying the use of biomass derived from

native wood through the Forest and Biomass Development

Plan 2025–2040.

The initiative, jointly developed by the State Secretariat

for Economic Development (Sedec) and the State

Secretariat for the Environment (Sema), sets guidelines for

traceability, legality and the efficient use of forest

biomass, consolidating this resource as a strategic input for

both industry and energy.

The plan promotes the reorganisation of the forest

production chain by transforming vegetation clearing

residues as a source of energy with an economic value,

while strengthening legal certainty and sector

standardisation which improves the investment

environment.

Structured around three pillars (expansion of planted

forests, strengthening of sustainable forest management

and development of the timber and biomass value chain) it

establishes ambitious targets, including the expansion of

planted forest areas to up to 700,000 hectares and areas

under sustainable management to 6.5 million hectares by

2040.

Additionally, the plan foresees a transition toward more

sustainable biomass sources, reducing dependence on raw

materials from authorised vegetation clearing and

encouraging the use of planted forests and industrial

residues.

This measure is expected to enhance the State’s

competitiveness in energy-intensive sectors while

contributing to the reduction of greenhouse gas emissions

thus aligning with the consolidation of a low-carbon

economy.

See: https://matogrossoeconomico.com.br/economia/em-acao-

inedita-no-pais-mt-regulamenta-uso-de-biomassa-de-madeira-

nativa-e-incentiva-a-economia-verde/

Native species silviculture gains momentum

The Brazilian Development Bank (BNDES), in

partnership with the Southern Bahia Science and

Technology Park (PCTSul) and the Brazil Climate, Forests

and Agriculture Coalition has established a strategic

initiative to expand native species silviculture in Brazil.

The agreement provides for an investment of BRL24.9

million in the Research and Development Program on

Native Species Silviculture (PP&D-SEN), operating in the

Atlantic Forest and Amazon biomes over a five-year

period.

The programme will be carried out across 14 research

sites, covering 30 native species, under the technical

coordination of the Federal University of São Carlos

(UFSCar) in the Atlantic Forest and by Embrapa in the

Amazon, while financial and administrative management

led by the Foundation for Institutional Support to

Scientific and Technological Development (FAI).

The initiative aims to boost the sustainable production of

tropical timber, increasing Brazil’s share in the global

market (currently estimated at 10%). The programme

integrates investment, public policies and regulatory

instruments promoting diversification in silviculture with

species such as cumaru, Brazil nut, copaiba, ipê and

andiroba.

In addition, the PP&D-SEN directly contributes to

achieving the goals of the National Plan for the Recovery

of Native Vegetation (Planaveg) by generating

environmental, economic and social benefits. Key

expected outcomes include the restoration of degraded

areas, carbon sequestration and job creation.

In this context, the initiative seeks to establish native

species silviculture as a strategic activity by expanding

scale, productivity, competitiveness and positioning Brazil

as a reference in sustainable production and innovation in

the forestry sector.

See: https://www.portaldoagronegocio.com.br/florestal/mercado-

florestal/noticias/silvicultura-de-especies-nativas-recebe-r-24-9-

milhoes-do-bndes-e-ganha-impulso-no-brasil#17314bbe-0823-

48bc-9e9a-2f24e5093217

Global instability reshaping timber exports

International economic instability, combined with

exchange rate volatility and geopolitical tensions, is

reshaping the dynamics of Brazilian timber exports. This

context increases uncertainty in negotiations and directly

affects companies’ operational planning, particularly

regarding timelines, pricing and logistics.

In response, exporters have been intensifying market

diversification strategies, especially based on progress in

expanding the European Union and Mercosur Agreement

which is expected to open new trade opportunities.

On the other hand, this process also imposes stricter

requirements in terms of competitiveness, organisation and

regulatory compliance, particularly regarding legality

requirements under the EUDR, the regulation on

deforestation-free products.

At the same time, there is a shift in commercial strategies

with greater emphasis on building long term relationships

between partners. Strengthening structured partnerships,

enhancing information exchange, ensuring alignment

between parties and promoting transparency have become

central elements for risk mitigation and increasing the

predictability of operations.

These moves reflect a broader transformation in

international trade in which companies simultaneously

seek transaction security and strategic positioning to

capture new opportunities, reinforcing the need for

resilience and adaptability among Brazilian exporters.

See: https://www.remade.com.br/noticias/21330/cenario-externo-

instavel-muda-dinamica-das-exportacoes-de-madeira-em-2026

US tariff hike and Middle East conflict impacts timber

exports

The increase in tariffs imposed by the United States has

affected timber sector exports in the state of Rio Grande

do Sul. In August of last year, tariffs reached as high as

50%, disrupting negotiations and reducing the

competitiveness of Brazilian products.

Later, in February this year, they were reduced to around

10% for most items but the international environment

remains unstable and uncertain.Players in the timber sector

have sought to diversify its markets to sustain operations.

However, the contraction of the U.S. market has led to

excess supply putting a downward pressure on prices and

margins despite the finding of new buyers.

At the same time, the conflict in the Middle East has

disrupted logistics which, in some cases, has resulted in

order cancellations, route changes and increased costs.

This combination of factors affects not only companies but

also the regional economy particularly in municipalities

where the timber industry represents the main economic

base and a significant provider of employment.

See:

https://gauchazh.clicrbs.com.br/pioneiro/economia/noticia/2026/

04/tarifaco-dos-eua-e-conflito-no-oriente-medio-pressionam-

exportacoes-do-setor-madeireiro-na-serra-

cmnq0886u00j201jyswnqwp6h.html

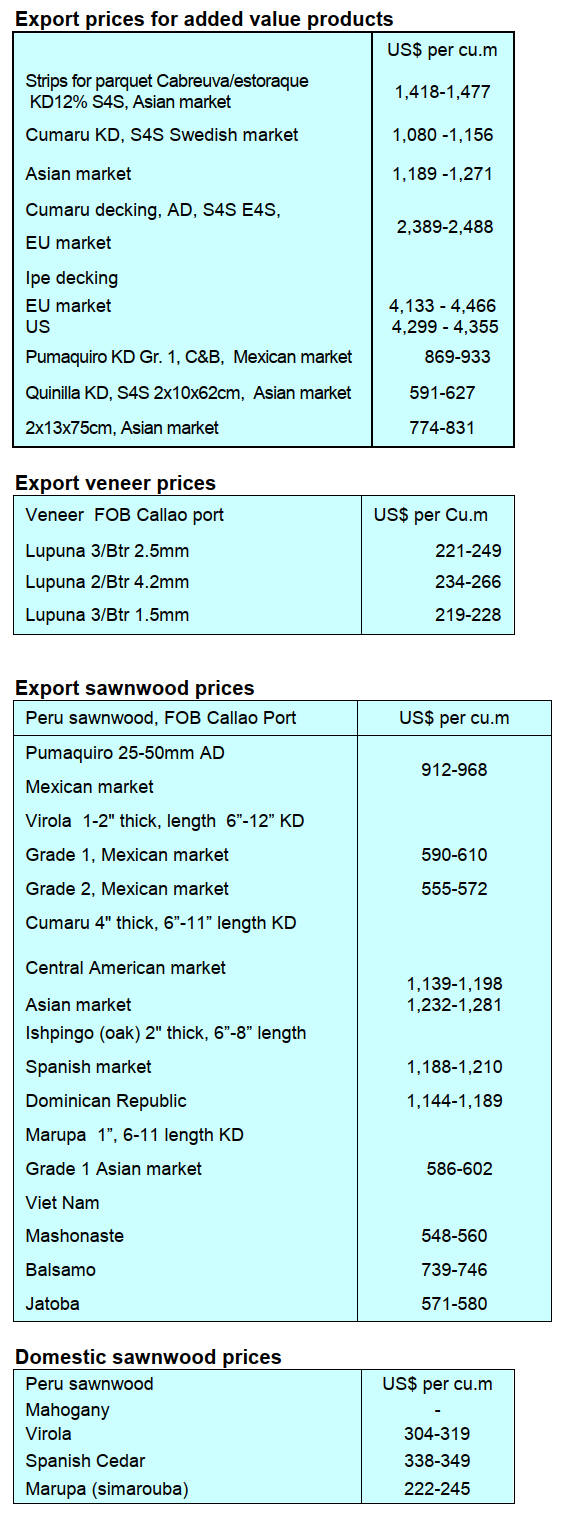

9. PERU

Timber sector experiencing worst crisis in past 25

years - ADEX

Beginning February the Wood and Wood Industries

Committee of the Association of Exporters (ADEX) has

been holding bi-weekly meetings with the National Forest

and Wildlife Service (SERFOR) as the timber sector is

experiencing a crisis.

In 2025, its exports totalled almost US$70 million, a

contraction of around 18% compared to the US$85 million

of 2024.

This situation, marked by over-regulation that has

increased business costs and excessively extended the

forestry business cycle to the point that various

administrative processes can take more than a year, is

generating growing concern. This weakens

competitiveness compared to other tropical countries,

affects profitability and jeopardises operational continuity

and formal employment.

Some iconic companies in the sector have already

ceased

operations, says ADEX and there is a risk that others will

follow suit if urgent measures are not taken.

The regular meetings aim to address the main bottlenecks,

respond to the adverse situation and contribute to the

recovery of the Peruvian timber industry.

Among the priority issues is the need to implement

incentives to reactivate investment, including tax benefits,

financial mechanisms, guarantees for new plantations and

better coordination with the regulations of the Agrarian

Law and the Amazon Law (Law No. 27037) in order to

provide greater legal certainty in tax matters.

On its part, SERFOR presented the Concessions 2.0

strategy, aimed at modernising forest management. The

new model proposes larger-scale concessions with

operators, who demonstrate technical and financial

capacity, integrating timber, non-timber forest products

and ecosystem services.

It also incorporates digital traceability, remote monitoring,

certification, value-added production and greater

collaboration between forestry and industry, including the

participation of communities as strategic partners.

The Timber and Wood Industries Committee highlighted

the importance of establishing a differentiated regime for

these types of concessions, streamlining the approval of

management instruments and complementing the system

with remote monitoring and performance evaluation

mechanisms.

Finally, the Committee expressed its concern regarding the

implementation of the European Union Deforestation

Regulation (EUDR), emphasising the need to strengthen

cooperation with producing countries to ensure a balanced

application of the regulations to promote sustainability

without affecting trade.

Strengthening technological capacity to combat forest

crimes

In the Amazon, technology has become a key ally in

combating environmental crimes allowing for the

detection of subtle changes in the forest dover.

For this reason, the Supervisory Agency for Forest

Resources and Wildlife (OSINFOR) strengthened the

capacities of 30 justice departments and forest resource

administrative authorities in the use of technologies that

enhance investigations into illegal logging in the

department of Ucayali.

“Technological tools provide us with real-time

information but it is up to us to transform these alerts into

concrete decisions and actions. The next step is to work in

a coordinated manner; to share information and build trust

among institutions to confront increasingly complex

crimes,” stated the Head of OSINFOR.

He also thanked the National Forest Conservation Program

of the Ministry of the Environment and the Peruvian Space

Agency (CONIDA) for their role as facilitators.

See: https://www.gob.pe/institucion/osinfor/noticias/1373645-

ucayali-operadores-de-justicia-y-autoridades-administrativas-

fortalecen-sus-capacidades-tecnologicas-para-enfrentar-delitos-

forestales

San Martín forest zoning updated

As part of the update to the Forest Zoning information in

San Martín, the Ministry of Agrarian Development and

Irrigation, through the National Forest and Wildlife

Service (SERFOR) and the Regional Government of San

Martín reported over 70% progress toward completing this

process which will strengthen the sustainable management

of the territory.

As part of this activity, the team from SERFOR's

Sustainable Productive Forests Program and the San

Martín Regional Environmental Authority are working on

finalising the physiognomic map, a tool that allows for the

identification and classification of different types of

vegetation cover in the territory.

See: https://www.gob.pe/institucion/serfor/noticias/1370294-san-

martin-actualizacion-de-la-informacion-de-la-zonificacion-

forestal-avanza-en-mas-del-70-por-ciento

|