|

Report from

Europe

EU tropical wood procuct imports increased in 2025

but remained at historically low levels

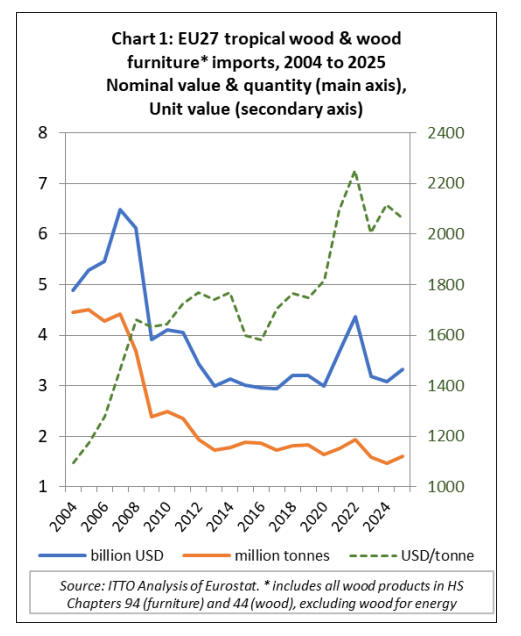

The EU imported 1,608,800 tonnes of tropical wood and

wood furniture in 2025, 10% more than in 2024. Import

value was up 7% to US$3.32 billion in 2025 (Chart 1).

Although a positive trend, the reality is that the gains last

year only just raised EU import quantity above the all-time

low recorded in 2024, while the 7% increase in the

nominal dollar value of imports is less impressive when

set against EU annual inflation of 2.4% in 2025 and 2.7%

the previous year.

Taking account of inflation, the real value of imports last

year was significantly less than during the static trading

years between 2012 and 2019.

It is also very uncertain whether the gains will be

sustained into 2026 as they may be more indicative of

efforts to build stocks in advance of EUDR enforcement,

which was due to start on 30 December 2025 only for the

EU to agree another 12 month delay on 18 December.

There was a significant surge in imports in the weeks

immediately before that announcement, much of it focused

on plywood and wood furniture from Vietnam. The EU’s

decision to impose anti-dumping duties on hardwood

plywood from China in the second half of last year was

another factor driving increased imports of plywood from

tropical countries, again most notably from Vietnam, in

the second half of 2025.

Nominal unit prices (not adjusted for inflation) for tropical

wood and wood furniture imported into the EU decreased

from US$2116 per tonne in 2024 to US$2026 in 2025. As

such they now sit in the middle of the range between the

peak of the post-COVID boom in 2022 and the bust in

2023.

Average unit prices of tropical wood product imports into

the EU are now much higher than before the COVID

pandemic when they never exceeded US$1800 per tonne.

This was partly owing to inflation and partly to a structural

shift in the tropical wood product groups imported into the

EU with a higher proportion now comprising higher value

finished furniture and joinery products rather than

sawnwood, mouldings and logs.

The increase in EU imports of higher value tropical

composite wood products has been one of the few bright

spots for the tropical wood industry in the EU market in

recent years. It remains to be seen if this shift will be

maintained when EUDR is eventually implemented, now

scheduled for 30 December 2026.

The geolocation requirements of EUDR are particularly

challenging for more complex products such as furniture

for which wood is necessarily aggregated from a wide

variety of different sources, including secondary processed

waste streams. Many wood furniture manufacturing

companies in Southeast Asia are SMEs and often

dependent on wood supplies from smallholders,

complicating supply chains even further. They will likely

need significant technical and marketing support to ensure

their conformance to EUDR.

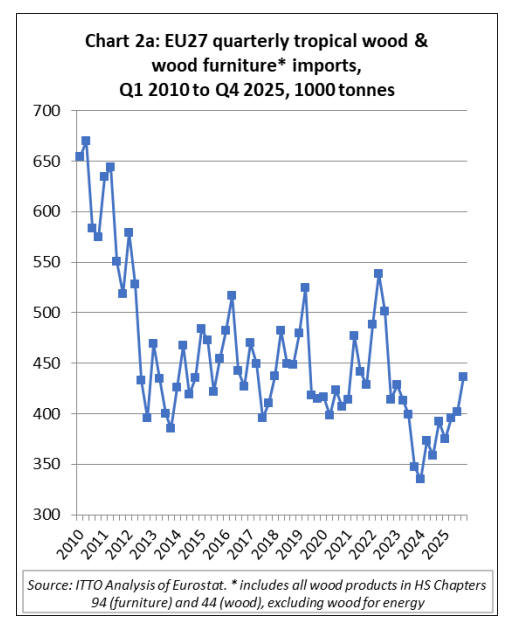

Rise in EU tropical wood imports in last quarter boosts

2025 figures

EU import quantity of tropical wood and wood furniture in

the fourth quarter of 2025 was 436,600 tonnes, 9% more

than the previous quarter and 11% more than the same

quarter the previous year. The surge in trade at the end of

last year took import tonnage during the fourth quarter of

2025 to close the long-term quarterly average of around

450,000 tonnes since 2013 (Chart 2a).

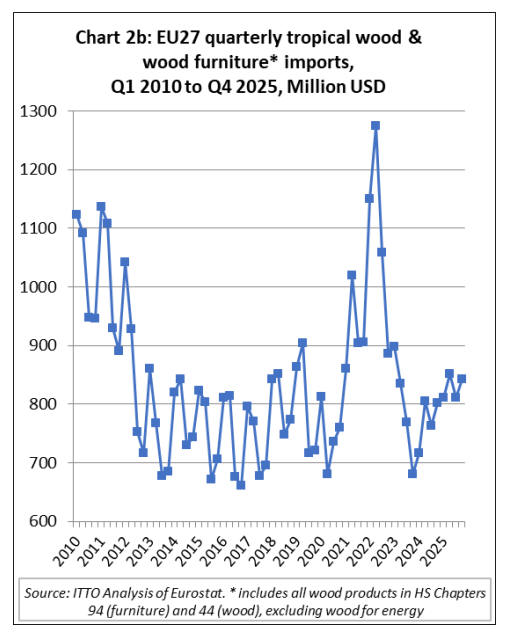

EU import value of tropical wood and wood furniture in

the fourth quarter of 2025 was US$843 million, 4% more

than the previous quarter and 5% more than in the same

quarter in 2024. In nominal US$ value terms (i.e. not

accounting for inflation), import value during the last

quarter of 2025 was well above the pre-pandemic 2013-

2019 quarterly average of around US$750 million (Chart

1b).

EU forecast of continued slow economic growth

In the fourth quarter of 2025, seasonally adjusted GDP

increased by 0.3% in both the euro area and the EU,

compared with the previous quarter, according to a

preliminary flash estimate published by Eurostat, the

statistical office of the European Union. In the third

quarter of 2025, GDP had increased by 0.3% in the euro

area and by 0.4% in the EU. Eurostat preliminary estimate

for the whole of 2025, based on quarterly seasonally and

calendar adjusted data, is that GDP increased by 1.5% in

the euro area and by 1.6% in the EU.

Economic performance varied widely between member

states. Among those for which data are available for the

fourth quarter of 2025, Lithuania (+1.7%) recorded the

highest increase compared to the previous quarter,

followed by Spain and Portugal (both +0.8%). Growth in

other large EU economies was slow in the second half of

last year: Germany posted 0.3% in the last quarter of 2025

after 0% growth the previous quarter; growth in France

was 0.2% in the last quarter after 0.6% the previous

quarter; in Italy, growth was 0.3% in Q4 after 0.2% in Q3.

However, Ireland (-0.6%) was the only Member State that

recorded a decrease in the last quarter of 2025 compared

to the previous quarter. The year-on-year growth rate was

positive for 14 countries and stable for one country.

According to KPMG’s latest European Economic Outlook

published in February, economic growth across Europe is

expected to remain modest over the next two years, with

euro area GDP forecast to grow by 1.1% in 2026 and 1.5%

in 2027. The KPMG forecast for 2026 is lower than the

EC estimate of 1.4% issued in November. KPMG expect

domestic demand to be the main driver of growth as

Europe navigates a more uncertain global trading

environment and continues to realign its trade

relationships.

With external headwinds intensifying, Europe’s growth

outlook increasingly depends on household consumption.

While savings rates remain elevated and consumer

confidence subdued, resilient labour markets and strong

nominal wage growth are expected to support real

disposable incomes and sustain modest consumption

growth through 2026. However, a sharp acceleration in

spending appears unlikely, with households expected to

remain cautious amid lingering economic uncertainty.

Consumer prudence could persist into the second half of

2026, with savings rates remaining elevated.

Although recent trade agreements with India and Mercosur

are important strategic steps for the EU after many years

of talks, they won’t have an immediate significant

economic impact. The amount of trade between countries

is still relatively small and it will take time for existing

tariffs to be removed. As a result, any real boost to

economic growth is likely to happen slowly and over a

longer period.

See:

https://kpmg.com/uk/en/media/press-releases/2026/02/eurozone-

gdp-forecast-to-grow.html

and

https://ec.europa.eu/eurostat/web/products-euro-indicators/w/2-

30012026-ap

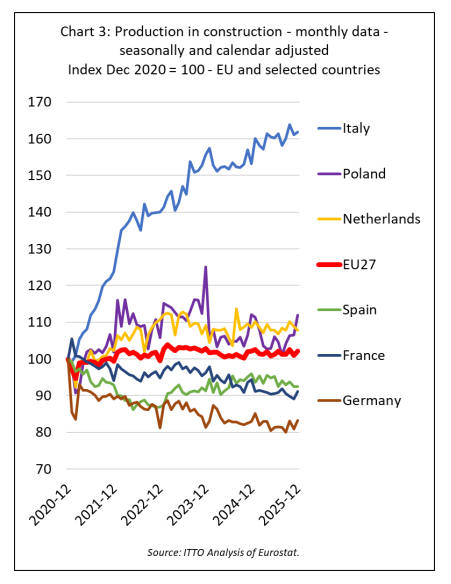

Flat EU construction sector shows some signs of life

Latest Eurostat data for EU construction production shows

that region-wide activity has remained broadly flat over

the last four years, although performance varied widely

between EU countries and the latest signals suggest there

may be some improvement ahead (Chart 3).

In the immediate post-COVID period, there was very

strong growth in construction activity in Italy, driven by

generous government incentives for renovation and energy

efficiency upgrades, but the pace slowed in 2024 and 2025

as these were removed. It should be said that the growth in

Italian construction activity after 2020 followed many

years of very slow activity so there was much ground to

make up. Italian construction activity is now growing

more slowly but the core of the industry remains robust,

particularly in infrastructure, industrial construction, and

the fast-growing digital economy.

Construction sector activity in France and Germany was

sliding throughout most of 2024 and 2025. This trend is

widely expected to continue in France but there are more

positive signs emerging in Germany. The confidence

indicator for the construction sector in France remains low

and is not improving. The issuance of housing permits

improved slightly at the beginning of 2025 in France but

has shown signs of decline since August.

According to ING, the Dutch financial services

corporation, the German construction industry is projected

to return to growth in 2026. German construction activity

contracted by more than 10% between 2020 and 2025, but

is expected to grow by 2.5% in 2026, driven by a gradual

recovery in the new residential market and increased

infrastructure investment.

Spain is also showing positive developments. The Spanish

construction sector faced a significant decline between

2019 and 2022, losing more than 25% of its volume.

However, the Spanish market has been recovering since

2023. ING forecast 2.5% growth in 2026. In recent years,

the number of building permits issued in Spain has surged.

Additionally, contractor confidence in Spain is strong, and

the construction industry is benefiting from robust GDP

growth.

The Netherlands has been one of the more buoyant

European construction markets in recent years, but ING

now expect Dutch building volumes to increase by just

0.5% in both 2025 and 2026. Housing construction is

particularly weak. ING highlight several structural

bottlenecks including a shortage of building land, lengthy

and complex permitting requirements, objection

procedures and grid congestion.

Source: https://think.ing.com/articles/2026-outlook-growth-

returns-to-the-european-construction-sector/

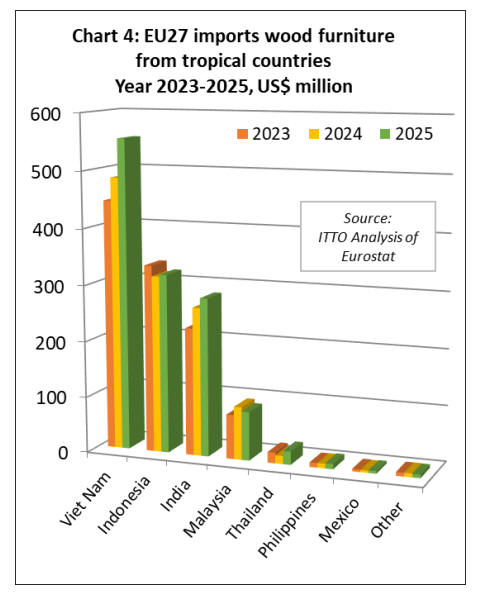

Vietnam leads growth in EU tropical wood furniture

imports in 2025

The EU imported 306,200 tonnes of wood furniture from

tropical countries with a total value of US$1286 million in

2025. Import quantity and value were up 7% and 8%

respectively compared to 2024.

Last year, EU import value of wood furniture increased

from the three largest supply countries: Vietnam (+14% to

US$554.2 million), Indonesia (+1% to US$319.1 million),

and India (+7% to US$281.8 million).

There were also large percentage gains in imports from

several smaller suppliers including Thailand (+65% to

US$23.7 million), the Philippines (+12% to US$9.3

million), and Mexico (+21% to US$4.7 million).

However, imports from Malaysia decreased 8% to

US$86.7 million. EU wood furniture imports from all

other tropical countries were negligible last year (Chart 4).

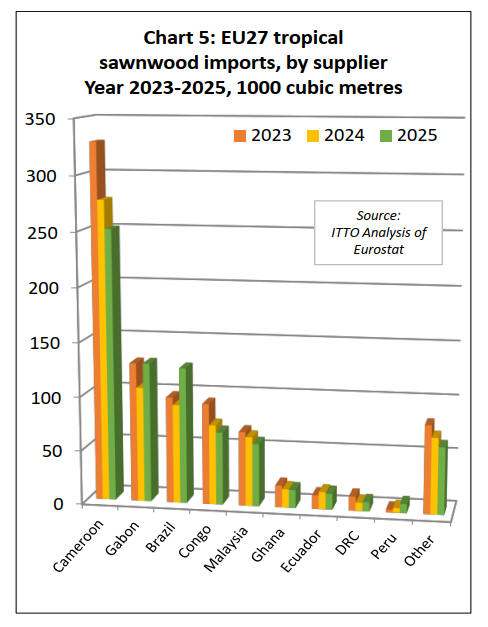

EU imports of tropical sawnwood last year barely

above 2024 record low

The EU imported 741,500 cu.m of tropical sawnwood

with a total value of US$679.6 million in 2025. Quantity

was up 2% while value was unchanged compared to the

record low recorded in 2024.

Tropical sawnwood imports were down in 2025 from

Cameroon (-9% to 250,800 cu.m), the Republic of Congo

(-9% to 67,500 cu.m), Malaysia (-9% to 58,200 cu.m),

Ghana (-3% to 16,700 cu.m), Ecuador (-17% to 10,400

cu.m), and Surinam (-25% to 5,400 cu.m).

However, these declines were offset by rising imports

from Gabon (+21% to 128,900 cu.m), Brazil (+38% to

125,600 cu.m), the Democratic Republic of Congo (+11%

to 8,500 cu.m), Peru (+91% to 8,300 cu.m), Indonesia

(+10% to 6,900 cu.m), and the Central African Republic

(+19% to 6,600 cu.m), (Chart 5).

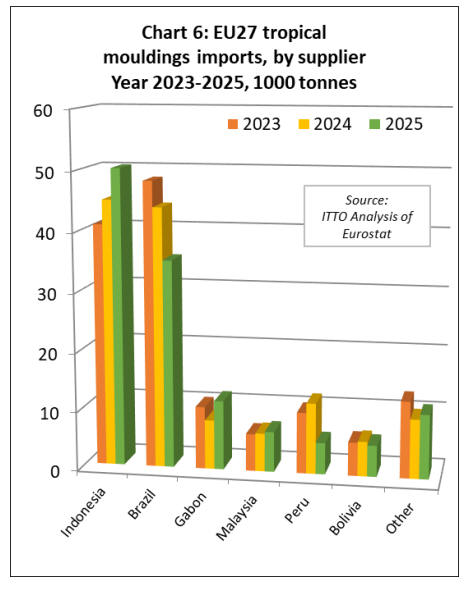

The EU imported 125,200 tonnes of tropical

mouldings/decking with a total value of US$215 million in

2025, respectively 5% and 7% less than in the previous

year. The decrease in imports was mainly due to a steep

decline from Brazil (-20% to 35,100 tonnes), and Peru (-

56% to 5,300 tonnes). Imports were also down 10% from

Bolivia to 5,300 tonnes. However, imports increased from

Indonesia (+12% to 50,200 tonnes), Gabon (+40% to

11,700 tonnes), and Malaysia (+5% to 6,800 tonnes)

during the year (Chart 6).

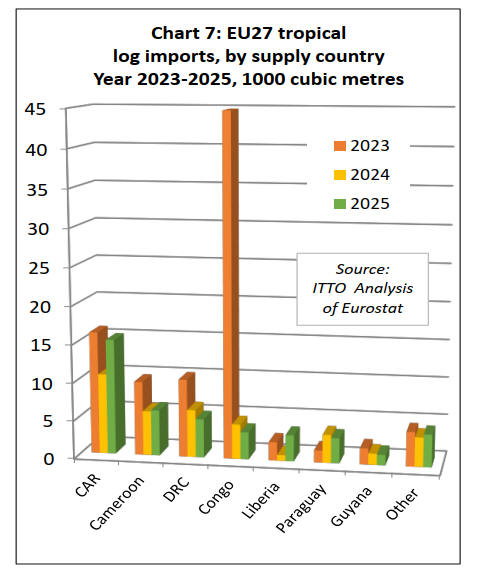

Rising EU imports of tropical logs from CAR and

Liberia in 2025

The EU imported 42,200 cu.m of tropical logs with a total

value of US$24.7 million in 2025, respectively 14% and

12% more in 2024.

The rise in trade quantity was particularly driven by sharp

percentage increases from the Central African Republic

(+44% to 15,200 cu.m) and Liberia (+355% to 3,400

cu.m), concentrated in the second quarter of the year.

Imports from Cameroon were also up 3% to 6,000 cu.m,

gaining pace in the third quarter after a slow start to the

year.

However, log imports declined from both the Democratic

Republic of Congo (-19% to 5,100 cu.m) and the Republic

of Congo (-21% to 3,600 cu.m) in 2025, responding to

tighter controls on log exports. EU log imports also fell

from Paraguay, by 10% to 3,300 cu.m, and from Guyana,

by 8% to 1,400 cu.m during year (Chart 7).

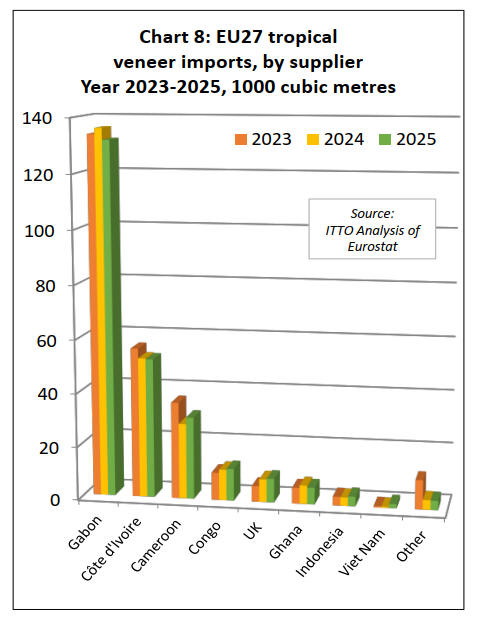

EU tropical veneer imports stable in 2025

The EU imported 250,300 cu.m of tropical veneer with a

total value of US$181 million in 2025. Import quantity

was the same as the previous year but value increased 6%.

EU imports of tropical veneer decreased during the year

from Gabon (-3% to 131,800 cu.m), Côte d'Ivoire (-0.5%

to 52,000 cu.m), and Ghana (-10% to 6,200 cu.m).

However, imports increased from Cameroon (+9% to

21,900 cu.m), the Republic of Congo (+4% to 12,000

cu.m), the UK (+4% to 8,900 cu.m), Indonesia (+15% to

3,600 cu.m), and Vietnam (+276% to 1,600 cu.m) (Chart 8

above).

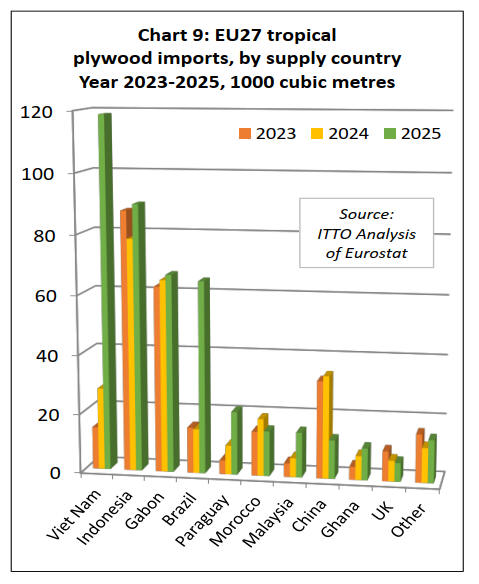

EU plywood imports impacted by anti-dumping duties

on Chinese products

The EU imported 435,900 cu.m of tropical plywood with a

total value of US$272.3 million in 2025, up 54% and 32%

respectively compared to the previous year. The

imposition of EU anti-dumping duties on Chinese

hardwood plywood in 2025, with a provisional rate of

62.4% imposed from 11 June followed by a definitive rate

of 86.8% from 21 November, had a dramatic effect on EU

plywood imports in 2025.

The policy contributed to a very rapid increase in

hardwood plywood imports from several tropical

countries. Imports increased particularly dramatically

from Vietnam last year, by 328% to 118,600 cu.m, thereby

overtaking Indonesia as the largest single supplier of

tropical plywood to the EU.

Hardwood plywood imports also increased sharply last

year from Brazil (+333% to 64,800 cu.m), Paraguay

(+117% to 21,300 cu.m), and Malaysia (+135% to 15,200

cu.m).

Imports increased at a slower rate from Indonesia (+15%

to 89,600 cu.m), Gabon (+3% to 66,700 cu.m), and Ghana

(+33% to 10,700 cu.m). These gains were only partly

offset last year by declining imports of tropical hardwood

plywood from China (-62% to 13,000 cu.m), Morocco (-

21% to 15,200 cu.m), and the UK (-10% to 6,300 cu.m)

(Chart 9).

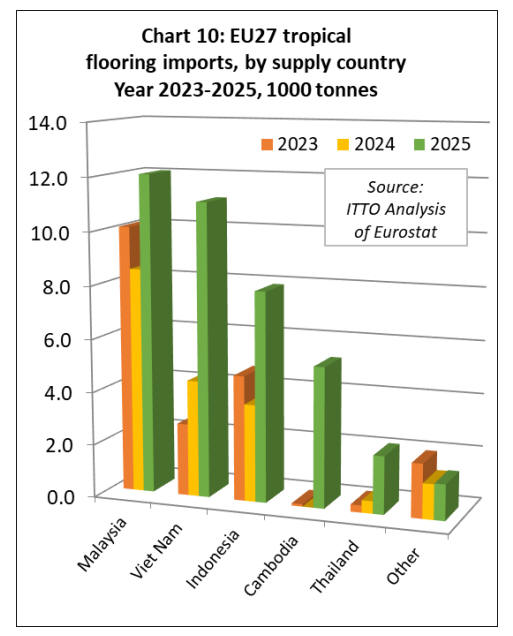

EU imports of tropical flooring up over 100% in 2025

The EU imported 39,900 tonnes of tropical wood flooring

with a total value of US$112.5 million in 2025, up 117%

and 132% respectively compared to the previous year.

Imports increased by 42% from Malaysia to 12,100

tonnes.

Imports of 11,100 tonnes from Vietnam were 152% more

than the previous year. EU imports of this commodity also

increased sharply in percentage terms from Indonesia

(+116% to 7,900 tonnes), and Thailand (+368% to 2,200

tonnes). The EU imported 5,300 tonnes of wood flooring

from Cambodia in 2025, up from near zero in 2024 (Chart

10).

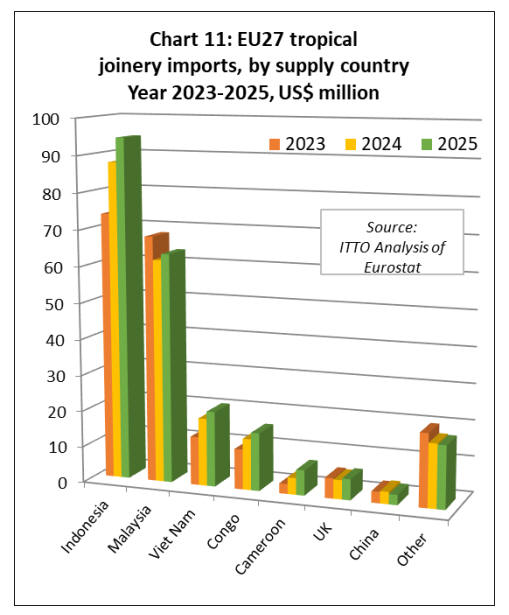

EU import value of other joinery products from tropical

countries - mainly laminated window scantlings, kitchen

tops and wood doors – was US$227.9 million in 2025, 7%

more than in 2024.

Import quantity increased 13% to 103,200 tonnes last year.

Import value increased from Indonesia (+8% to US$94.6

million), Malaysia (+3% to US$63.5 million), Vietnam

(+11% to US$20.8 million), the Republic of Congo (+13%

to US$16.1 million), Cameroon (+51% to US$7.0

million), and the UK (+10% to US$5.8 million).

However, EU import value of joinery products made from

tropical wood was down 17% to US$2.8 million from

! China in 2025 (Chart 11).

|