Japan

Wood Products Prices

Dollar Exchange Rates of 10th

February

2026

Japan Yen 153.27

Reports From Japan

Businesses prioritise stability

The business community in Japan has welcomed the ruling

Liberal Democratic Party's victory in the House of

Representatives election where it regained a majority.

Yoshinobu Tsutsui, chairman of the Japan Business

Federation (Keidanren) said, the organisation hopes that

the administration of Prime Minister Sanae Takaichi, also

LDP Leader, "will steadily implement important policies

under strong leadership backed by the huge public trust.

The Liberal Democratic Party secured a victory in the

recent Lower House election. This will essentially allow

the LDP-led coalition to override challenges that emerge

as a result of its lack of a majority in the Upper House. In

the event key bills and budgets are voted down in the

Upper House, they can be overridden in the Lower House

with a two-thirds majority.

Japanese businesses prioritise stability driven by concerns

over geopolitical tensions, fluctuating costs, a weakening

yen and the need for predictable interest rate policy from

the Bank of Japan (BoJ).

Firms seek to maintain a stable political environment,

specifically, financial market stability rather than drastic,

rapid changes in monetary policy.

In related news, the Japan Federation of Basic Industry

Workers’ Unions decided Wednesday to demand a

monthly pay scale increase of 15,000 yen in this year’s

spring wage negotiations. The unified demand is at the

same level as the previous year which was a record high.

See:

https://www.japantimes.co.jp/news/2026/02/09/japan/politics/jap

an-2026-lower-house-election/

See:

https://www.nippon.com/en/news/yjj2026020400879/?cx_recs_c

lick=true

Slow pace of household spending

A report from the Cabinet Office says Japanese household

spending increased at a slower pace than income over the

past five years indicating that people saved more amid

inflation.

According to the fiscal 2025 report on the country's

economic conditions, disposable income rose across all

age and income groups from 2019 to 2024 but

consumption growth was sluggish, with spending falling

in some groups. The savings rate increased for all groups

except those in their 20s.

Lower-income households were more affected by

inflation, as rising food costs accounted for a larger share

of their spending.

See: https://www.nippon.com/en/news/yjj2026021000904/

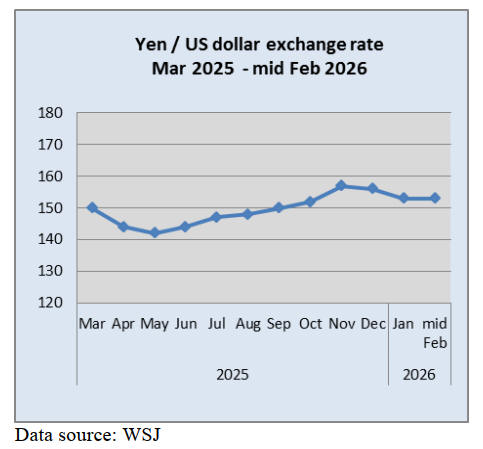

New norm of yen volatility

The volatility and depreciation of the Japanese yen, which

hit multi-decade lows in 2024/5 and remained unstable

into early 2026, has created a difficult environment for

Japanese importers.

The past two years have seen record-breaking swings, with

the yen occasionally falling to 160 per dollar prompting

massive intervention from the Ministry of Finance to

defend the currency. As of early 2026, the yen remained

highly volatile due to uncertainty surrounding Japan's

tentative exit from ultra-easy policy and inflationary

pressures.

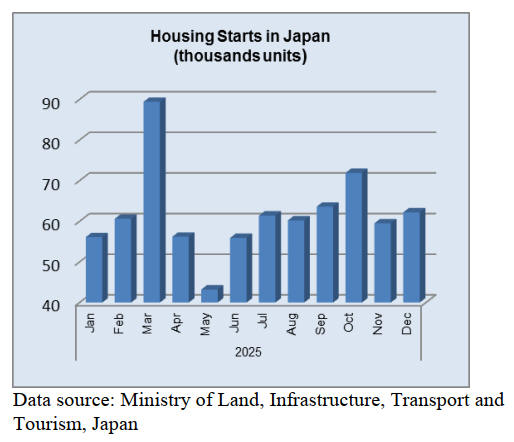

Housing starts at 62-year low

Housing starts in Japan fell 6.5% from the previous year to

740,667 units in 2025, down for the third straight year and

hitting a 62-year low. The drop reflected deterioration in

consumer sentiment amid rising prices as well as falling

demand due to the country's shrinking population.

Of the total, owner-occupied houses dropped 8% to

201,285 units, down for the fourth consecutive year.

Housing for rent fell 5% to 324,991 units, down for the

third year in a row. Condominiums and houses for sale

decreased 8% to 208,169 units, down for the third

consecutive year. Part of the slowdown could be because

of a revision to regulations on homes with energy-saving

features which has increased construction time and pushed

up prices.

See: https://www.nippon.com/en/news/yjj2026013001015/

Contrasting response of home buyers

Inflation is impacting the housing market in contrasting

ways. A Bloomberg Intelligence survey suggests potential

homebuyers are divided on their property purchasing plans

as surging living costs add to affordability concerns.

Some are delaying purchases while others are wary of

missing out on opportunities posed by rising home prices.

People who prefer to wait cited personal circumstances

and the rising cost of living as their main reasons while

those who were bringing forward plans to buy said they

were afraid of prices climbing even more.

See:

https://www.japantimes.co.jp/business/2025/10/17/economy/toky

o-homebuyers-purchase-plans/

Mortgage rates increased

Five major banks have increased base rate for a 10-year

fixed-rate mortgage. This decision is linked to the recent

increase in benchmark interest rates of long-term

government bonds. The rates of MUFG Bank, Sumitomo

Mitsui Banking Corp., Mizuho Bank and Sumitomo

Mitsui Trust Bank are set at the highest since their

establishment.

The new rates are subject to loans filed this month. Loans

that have already been taken out will not be affected. The

five banks did not change variable rate home loans, which

account for about 80% of housing loans that have been

taken out.

See:

https://japannews.yomiuri.co.jp/business/companies/20260201-

308306/

Import update

Wooden furniture imports

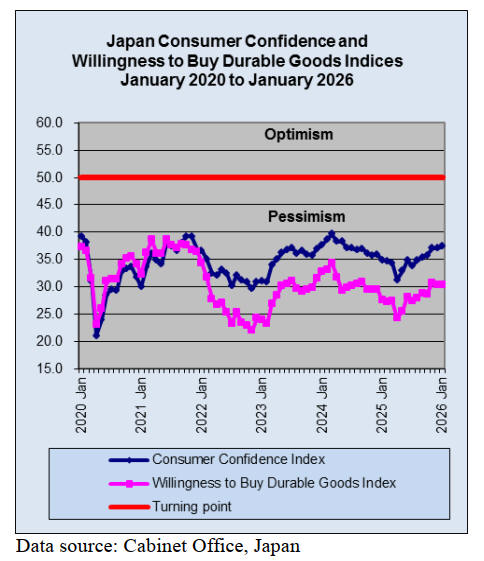

Consumer confidence is a primary driver of furniture

purchases as such items are considered discretionary.

When consumer confidence is high households are more

likely to invest in home improvements and durable goods.

The willingness of Japanese consumers to buy durable

goods has been steadily increasing since early 2025 but is

still below pre-pandemic levels.

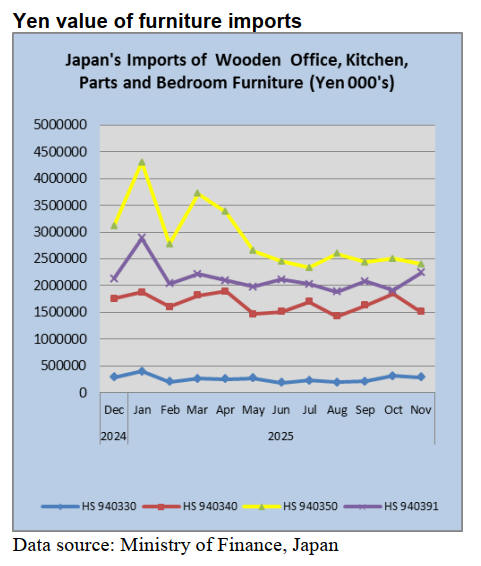

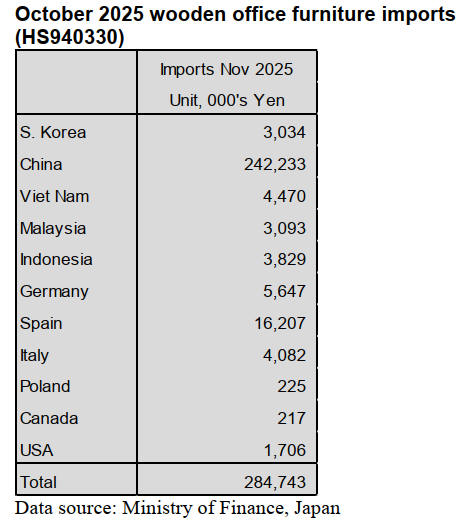

November 2025 wooden office furniture imports

(HS940330)

In November 2025 China accounted for 85% of the value

of wooden office furniture imports followed by Spain (6%

sharply up compared to previous months) and Viet Nam,

Malaysia and Indonesia at around 2.5% each. November

shipments from China were down10% compared to

October and also down by 3% year on year. The other

significant source of wooden office furniture in November

was Germany.

Year on year the value of Japan’s imports of wooden

office furniture (HS940330) in November fell 3%.

Compared to the value of October arrivals there was a

10% decline in the value of imports.

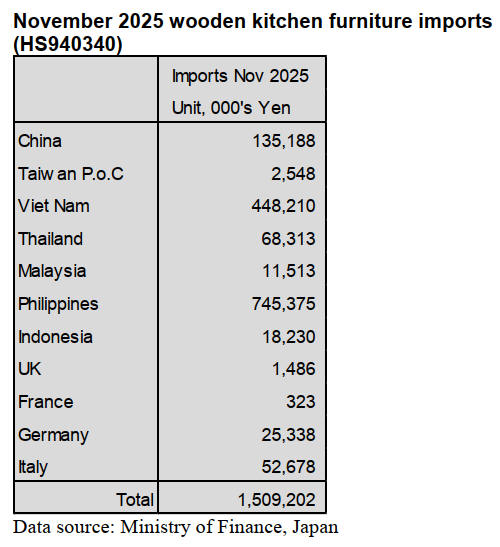

November 2025 wooden kitchen furniture imports

(HS940340)

November imports of wooden kitchen furniture

(HS940340) were dominated by shippers in the

Philippines (49% compared to 55% in October) and Viet

Nam (30% of imports). The value of November imports

from both the Philippines and Viet Nam declined month

on month with shipments from the Philippines dropping

27% and shipments from Viet Nam dropping 16%. The

third ranked shipper in terms of value in November was

China with the value of imports accounting for around 9%

of all HS940340 arrivals.

The top three shippers accounted for nealy 90% of

November arrivals with the other shippers being Thailand

and Italy, where there was a sharp rise in the value of

imports compared to a month earlier. Year on year the

value of November wooden kitchen furniture imports were

down 12%.

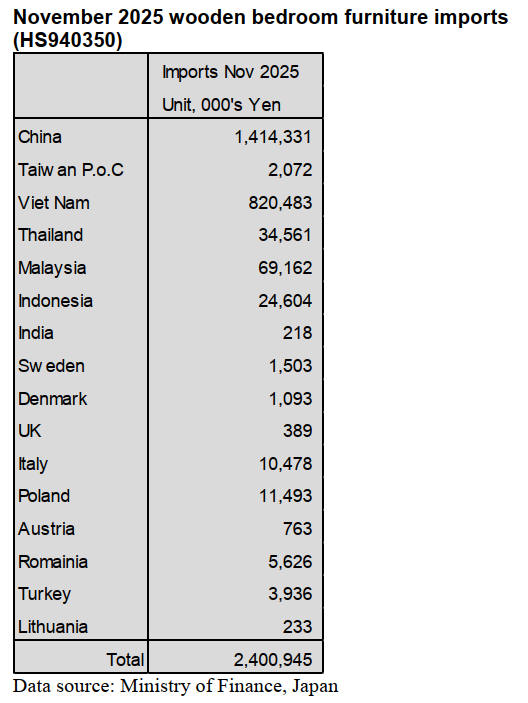

November 2025 wooden bedroom furniture imports

(HS940350)

Since mid-2025 the value of wooden bedroom furniture

imports has been remarkably steady compared to the

volatile trend in the early part of 2025. From June 2025

the value of arrivals has been in a narrow range.

In November over 90% of the value of shipments of

wooden bedroom furniture was shipped from China (59%

of the total) and Viet Nam (34%). Of the other shippers in

November Malaysia was at the top accounting for about

3% of the value of arrivals with November shipments

around three times more than in the previous month..

Year on year there was a 19% decline in the value of

November and a 4% decline in total imports of HS940350

imports.

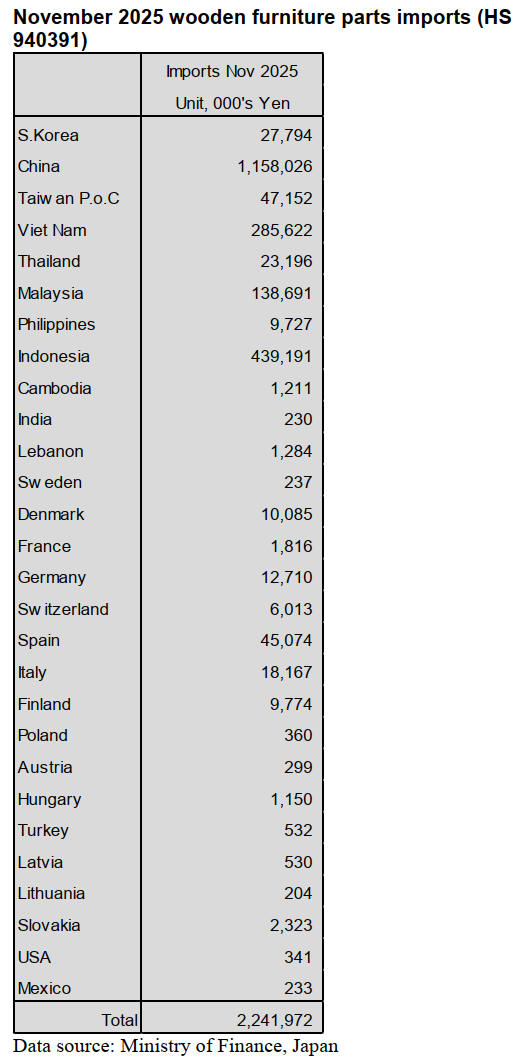

November 2025 wooden furniture parts imports

(HS940391)

Year on year, the value of November imports of

HS940391 was down around 10% but there was a 17%

increase in the value of imports compared to October.

The main shippers of wooden furniture parts to Japan in

November were China at 52% of the total (49% in

October) and Indonesia 20%, around the same level as in

October. November shipments from China were up 24%

month on month and there was a 21% increase in month

on month shipments from Indonesia.

In November the other main shippers of HS940391 were

Viet Nam (13% of imports) and Malaysia, 6% being some

20% higher than in the previous month.

Trade news from the Japan Lumber Reports (JLR)

The Japan Lumber Reports (JLR), a subscription trade

journal published every two weeks in English, is

generously allowing the ITTO Tropical Timber Market

Report to reproduce news on the Japanese market

precisely as it appears in the JLR. For the JLR report

please see: https://jfpj.jp/japan_lumber_reports/

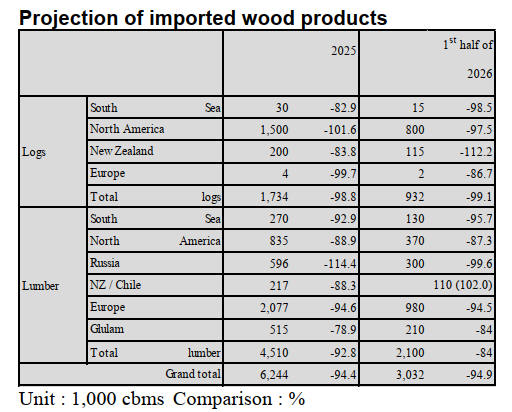

Projection of import wood products

The Japan Lumber Importers Association disclosed

projection of imported wood products for 2025 and the

first half of 2026.

*European logs are softwood logs. South Sea logs

include

African logs. *Glulam is laminated structural softwood lumber

and does not include interior finish materials.

Both logs and lumber/products are expected to decrease

by around 5% compared to the same period last year. It is

considered to be the result of multiple factors, including a

decline in demand for housing-related materials, the

weaker yen and higher interest rates, as well as the

substitution of wood products made from domestic

timber.

In 2025, the supply–demand and price disruptions caused

by the third “wood shock,” which continued through

2024, began to settle down. As a result, issues related to

supply–demand adjustments for imports became less

prominent, while the stronger dollar and weaker yen in

the latter half of the year led to higher import costs.

The supply of U.S. log timber is influenced by the

operating conditions of Chugoku Lumber Co., Ltd., a

company based in Hiroshima. One factor behind this is

the start-up of the Kashima plant in 2025, which added an

additional 150,000 cubic meters of capacity. For New

Zealand timber, higher log prices have pushed up sawn

timber prices, leading to increased use of domestic cedar

for packaging materials. As a result, the decline in import

volumes has become more pronounced.

For South Sea logs, supply has been centered on deliveries

to Sattsuru Plywood Co., Ltd., which has limited demand

in areas such as Nagoya and Hiroshima. The roughly 5%

year-on-year decline in European timber is considered to

be almost within the normal range. If the yen continues to

weaken further, a decline in competitiveness will be

unavoidable going forward.

The decline in U.S. and Canadian timber is substantial,

and the fact that it is expected to fall by more than 10% in

the first half of 2026 is a cause for concern. Russian

timber was the only category to increase, rising by 14%.

The decline in New Zealand and Chilean timber is due to

shipping schedule arrangements.

The nearly 20% year-on-year decline in glulam

clearly

indicates a downturn in domestic demand for housing

construction materials.

North American logs

Harvesting of Douglas-fir logs in Washington and Oregon is

progressing smoothly, and stable output is expected through

February and March. Meanwhile, log inventories within the

United States are declining, keeping export prices on a firm

trend.

In contrast, Canadian supply has not increased due to

rising stumpage fees on public forests and U.S. import

tariffs. However, shipments to Japan remain stable

because they rely mainly on logs from private forests.

January shipments of Douglas-fir sawlogs were unchanged

from December: IS grade at $970 (FAS, 1,000 BM, Scribner

scale), SS grade at $1,000, and SLC grade at $890. Logs for

plywood were also flat at $220–221

Harvesting of Douglas-fir logs in Washington and Oregon is

progressing smoothly, and stable output is expected through

February and March. Meanwhile, log inventories within the

United States are declining, keeping export prices on a firm

trend. In contrast, Canadian supply has not increased due

to rising stumpage fees on public forests and U.S. import

tariffs. However, shipments to Japan remain stable

because they rely mainly on logs from private forests.

Plywood

Domestic softwood structural plywood saw improved

movement toward the end of last year due to pre-holiday

stocking, but activity has slowed somewhat in January.

Precut-plant demand remains relatively steady, while the

building-materials route continues to lack momentum.

Amid these conditions, domestic softwood structural plywood

(12 mm, 3×6) has been weakening, especially in the Tokyo

area since December. January prices in the region are

centered around ¥1,060–1,070 per sheet (wholesaler

delivery), about ¥20– 30 lower than the previous month.

Imported tropical plywood is seeing gradual price increases

for some Indonesian standard panels, while Malaysian 12-mm

products remain mostly flat. In Japan, demand— especially

for coated formwork panels—has been sluggish, domestic

prices have barely risen, and the weak yen has pushed up

forward costs. These factors have kept orders to producing

regions from gaining momentum.

Producing-region prices for Indonesian standard plywood

are around $970 per cbm (C&F) for 2.4-mm 3×6 panels,

$880 for 3.7-mm, and $850 for 5.2-mm. Malaysian

products remain flat from the previous month, with coated

formwork plywood (12 mm, 3×6) at $600–610, formwork

plywood at $500–510, and structural plywood at $510–

520 (all C&F, per cbm).

Coated formwork plywood (12 mm, 3×6) varies by

manufacturer, but prices are around ¥1,840–1,900 per

sheet (wholesaler delivery). Formwork plywood is priced

around ¥1,600 per sheet (wholesaler delivery), and structural

plywood is at a similar level. Indonesian standard plywood is

roughly ¥780 for 2.5-mm panels, ¥930 for 4-mm, and ¥1,100

for 5.5-mm (all per sheet, wholesaler delivery).

South Sea logs and products

Tropical and China-made wood products continue to face

weak sales, but producing regions remain firm due to rising

costs. In Indonesia, reduced log supply is pushing up prices

for keruing, selangan-batu, and Merkus pine products.

Tropical log arrivals from Malaysia and PNG have largely

completed for FY2025 H2, and despite some delays from

Thailand, overall supply–demand conditions are stable.

|