|

Report from

the UK

Largest increase in share of EU27 tropical wood

market for at least 15 years

In 2021, logistical problems on the supply side in tropical

countries during the COVID pandemic seemed to

accelerate the long term trend away from tropical timber

products in the EU27 market.

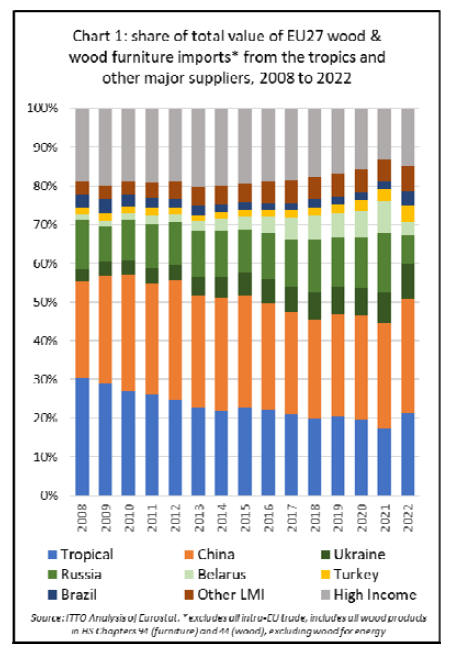

The share of tropical products in the total value of EU27

imports of wood and wood furniture fell from 20% in

2020 to just 17% in 2021.

However, last year the situation was transformed as

tropical products recorded the largest increase in share for

at least the last 15 years, rebounding to 21% of the total

value of EU27 imports of wood products and wooden

furniture (Chart 1).

The recovery in the value and share of tropical wood

products trade with the EU in 2022 was driven both by

normalisation of supply chains and falling freight rates

after the severe disruption of pandemic, together with a

sharp fall in available supply of wood products from

Russia and Belarus during the year.

In 2021, the EU27 imported wood and wooden furniture

with a total value of US$4.95 billion from Russia and

Belarus, nearly one quarter of total import value of these

products. However, this fell to just US$2.24 billion in

2022.

The EU first imposed trade sanctions on Belarus timber

products on 2 March 2022. These were extended to

Russian timber products on 8 April 2022.

On 10 March 2022, Russia’s Industry and Trade Ministry

announced a ban on all wood and timber-related exports to

"unfriendly countries", including the EU, UK and US.

Both leading certification organisations, the PEFC and

FSC, announced in March 2022 that all timber originating

from Russia and Belarus would be categorised as ‘conflict

timber’ (i.e. from a controversial source) and not eligible

to be sold and promoted as PEFC- or FSC-certified. This

had a significant impact on many European companies

which had become heavily dependent on Russia and

Belarus for their supplies of certified wood.

Of total FSC global forest area of 237 million hectares at

the start of last year, 63 million hectares (27%) was in

Russia and 15 million hectares (6%) in Belarus.

Of PEFC certified area worldwide of 328 million hectares

at the start of last year, 32 million hectares (10%) was in

Russia and 9 million hectares (3%) in Belarus.

At the start of 2023, PEFC reported no certified forest in

either Russia or Belarus.

FSC is currently reporting zero certified forest area in

Belarus but 39.5 million hectares in Russia despite the

‘conflict timber’ categorisation.

EU27 trade data indicates that these measures took time to

take effect, with timber products continuing to be imported

in significant volumes from both Russia and Belarus until

July 2022. However EU27 imports from both countries

fell to close to zero in the last five months of the year.

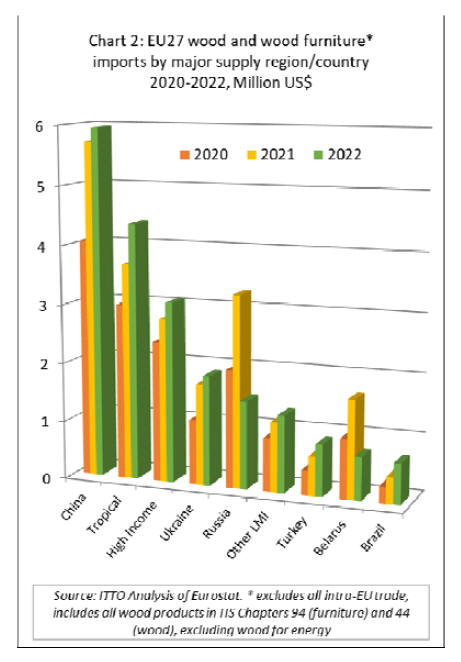

In value terms, tropical products were significant

beneficiaries of the sharp fall in EU27 imports of wood

products from Russia and Belarus during 2022.

Whereas total EU27 imports of wood and wood furniture

fell 4% from US$21.2 billion in 2021 to US$20.4 billion

in 2022, imports of tropical products increased 18% from

US$3.7 billion to US$4.4 billion during the same period.

EU27 import value of wood and wood furniture from

China increased only 4% to US$6.0 billion in 2022,

although this did build on a massive 42% gain the

previous year. Import value from Ukraine also increased

by 9% to US$1.9 billion in 2022, despite the serious

disruption due to the war, following a 55% gain the

previous year.

Other significant beneficiaries were Turkey, for which

EU27 import value increased 32% to US$890 million last

year, and non-tropical products from Brazil which

recorded a 54% increase to US$ 690 million in 2022

(Chart 2).

EU27 import value from the tropics increased across all

wood product groups last year including furniture (+10%

to US$1.73 billion), sawnwood (+22% to US$904

million), mouldings/decking (+21% to US$396 million),

joinery (+27% to US$286 million), plywood (+52% to

US$254 million), veneer (+13% to US$234 million),

marquetry/ornaments (+55% to US$127 million), flooring

(+45% to US$89 million), and logs (+10% to US$65

million) (Chart 3).

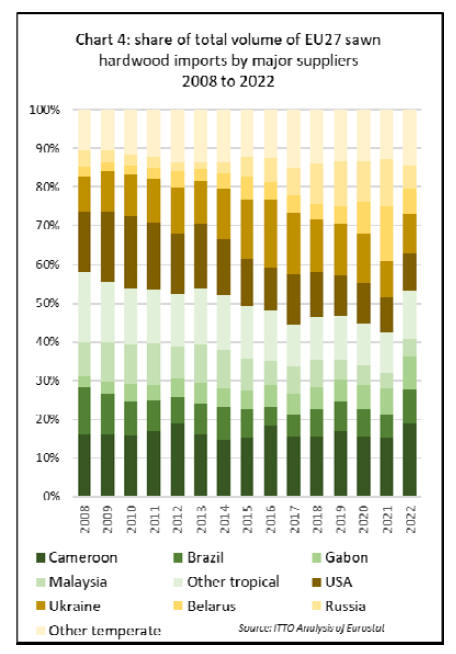

EU imports of tropical sawnwood exceed 1 million

cu.m for first time since 2016

In volume terms, tropical sawn hardwood recorded a

particularly large increase in share of total EU27 imports

of sawn hardwood in 2022 (Chart 4).

EU27 imports of tropical sawnwood increased 18% to

1.01 million cubic metres during the year, exceeding one

million cubic metres for the first time since 2016.

In contrast, EU27 imports of temperate hardwoods fell

23% to 890,000 cubic metres in 2022. The share of

tropical in total EU27 sawn hardwood imports jumped

from 43% in 2021 to 53% in 2022, the highest share since

2013.

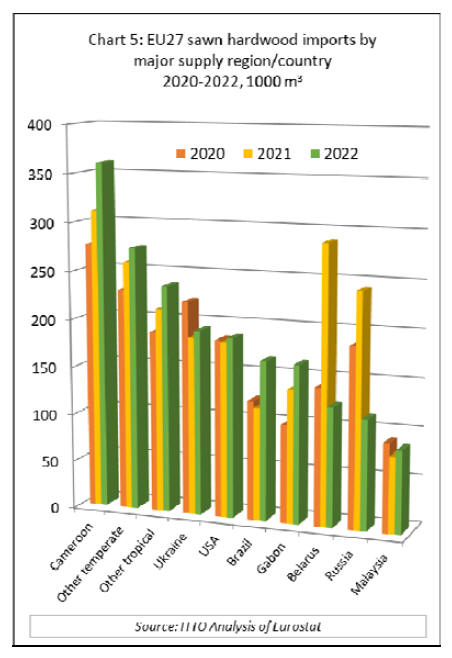

Tropical sawnwood was by far the largest beneficiary of

the decline in share of Russian and Belarus sawn

hardwood in 2022 as other suppliers of temperate

hardwood made only minor gains.

Imports from Ukraine increased just 4% to 192,000 cubic

metres, while imports from the U.S. were up only 2% to

187,000 cubic metres.

This compares to gains of 16% to 360,000 cubic metres

from Cameroon, 42% to 166,000 cubic metres from

Brazil, and 19% to 164,000 cubic metres from Gabon

(Chart 5 above).

War in Ukraine has massive impact on EU27 plywood

market

Russia's invasion of Ukraine had a massive impact on the

EU market for plywood in 2022. ITTO interviews with EU

plywood importers during the year indicated a huge rush

for products from the tropics where mills were encouraged

to ramp up production as much as possible for the EU

market. Tropical manufacturers were particularly

encouraged to launch (or relaunch) production of thicker

film-faced boards, mostly supplied to the EU by Russia in

recent years.

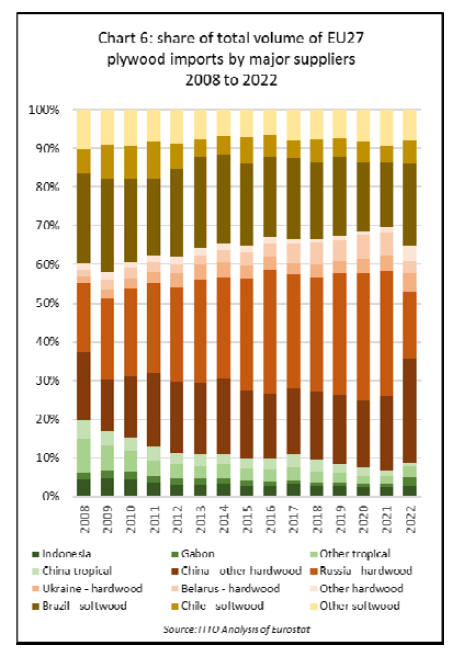

The share of tropical products in total EU27 plywood

imports, which fell to an all-time low of just 7% in 2021,

rebounded to 9% in 2022, close to the level prevailing in

the decade before the pandemic (Chart 6).

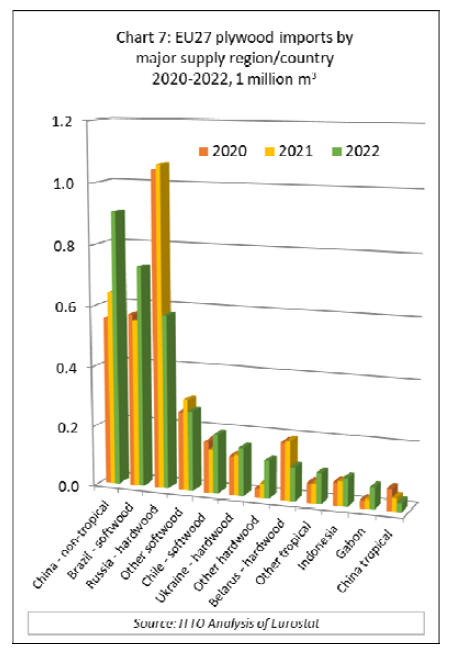

Total direct imports of plywood from the tropics increased

48% to 266,000 cubic metres in 2022, with imports from

Indonesia up 13% to 92,000 cubic metres and from Gabon

up 124% to 72,000 cubic metres.

Imports of tropical hardwood plywood from China

decreased 32% to 31,000 cubic metres. In contrast to the

decline in EU27 imports of tropical hardwood plywood

from China, imports of non-tropical hardwood plywood

from the country surged 41% to 906,000 cubic metres.

Other plywood products making significant gains in the

EU27 market in 2022 were softwood plywood from Brazil

(+32% to 730,000 cubic metres) and Chile (+35% to

196,000 cubic metres), and hardwood plywood from

Ukraine (+18% to 160,000 cubic metres) (Chart 7 left).

|