|

Report from

the UK

UK 2022 tropical imports flat as weak second half

offsets strong start to the year

The latest data from the UK Office for National Statistics

shows that UK GDP increased 4.0% in 2022 after 7.6%

growth in 2021, as it recovered from the historic blow

from the COVID-19 pandemic. However this "rise" over

the last two years must be considered in the light of the

UK being amongst countries worst affected by the

COVID-19 pandemic which led to a 9.4% fall in GDP in

2020 at a time when there was already uncertainty due to

the country’s departure from the EU. The UK economy in

December 2022 was still smaller than it was in December

2019.

The relatively sluggish recovery of the UK economy last

year is reflected in UK imports of tropical wood and wood

furniture products which were flat overall in 2022, valued

at US$1.4 billion, the same as the previous year and just

equalling the pre-COVID level in 2019. UK import value

of tropical wood and wood furniture products last year was

only marginally above the long term average for the

previous ten years and well below levels prevailing in the

years prior to 2010 (Chart 1a).

Strong UK imports of tropical products in the first half of

last year were offset by a sharp downturn in the last six

months of the year. In 2022 there was an increase in UK

import value of tropical joinery (+9% to US$271 million),

sawnwood (+32% to US$124 million), and

mouldings/decking (+18% to US$35 million). However

UK import value of tropical wood furniture fell 8% to

US$731 million, while import value of tropical hardwood

plywood was down 12% to US$168 million.

Vietnam was the leading supplier of tropical wood and

wood furniture to the UK last year, with import value of

US$382 million, 3% down on the previous year. The value

of direct imports also declined last year from all three of

the other leading tropical suppliers including Indonesia (-

8% to US$309 million), Malaysia (-4% to US$238

million), and India (-3% to US$102 million).

However, these figures may overestimate the decline as

problems of shipping cargo directly from Asia into the UK

last year contributed to an 63% increase in the value of

tropical wood and wood furniture imports into the UK

from EU27 countries, to US$107 million.

After losing share in the UK market between 2019 and

2021 during the COVID-19 pandemic, tropical wood and

wood furniture products regained some share last year,

mainly at the expense of other lower and middle income

(LMI) countries, particularly China, Russia, and Belarus.

The total value of UK imports of wood and wood furniture

products from all countries was US$13.62 billion in 2022,

9% less than the previous year. This followed a gain of

42% in 2021.

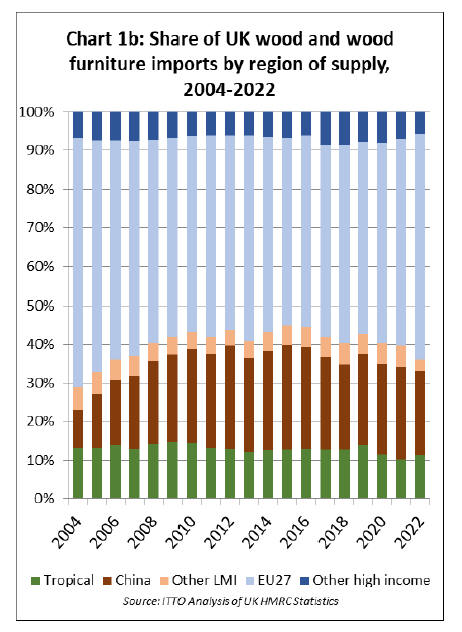

The share of tropical products in total UK wood and wood

furniture import value increased from 10.4% in 2021 to

11.4% last year, although this is still well below the long

term average of between 13% and 14% share (Chart 1b) .

UK import value of non-tropical wood and wood furniture

products from China fell 17% to US$2.67 billion last year.

The share of China in total UK wood and wood furniture

imports fell from 24% in 2021 to 22% last year. This

represents a return to more normal levels in UK imports

from China after a 43% surge in US$ value the previous

year in response to booming demand in the immediate

aftermath of the COVID lockdowns.

Other factors contributing to slower UK imports from

China last year included supply problems during China’s

strict COVID-19 lockdowns, serious congestion at UK

ports in the first half of last year, and concerns that

Chinese products may contain Russian wood which has

been subject to trade sanctions in the UK since Russia’s

invasion of Ukraine in February last year.

UK sanctions imposed on Russian products led to an 89%

decline in the value of UK imports of Russian wood and

wood furniture last year, from US$329 million to just $36

million. Although the UK has not officially sanctioned

imports of wood from Belarus, these also fell sharply, by

90% from US$59 million to US$6 million.

Imports of non-tropical products from several other LMI

countries also fell sharply last year including Brazil (-19%

to US$151 million), South Africa (-37% to US$29

million), Ukraine (-14% to US$26 million), UAE (-56% to

US$17 million), and Uruguay (-29% to US$16 million).

Overall the share of UK imports of non-tropical products

from LMI countries other than China decreased from 6%

to 3% last year.

UK imports of non-tropical wood and wood furniture

products from the EU27 fell 1% to US$7.17 billion in

2022. This followed on from a huge 46% increase in 2021.

And because the decline from the EU27 last year was

much less than from other regions, the EU27 total share of

UK import value of wood and furniture from the EU27

increased from 53% in 2021 to 58% in 2022.

Expectations that the UK's departure from the EU might

lead to a decrease in the share of imports of wood and

wood furniture from the EU and a switch to other regions

have yet to be realised. On the contrary, in the five years

following the UK's decision to trigger Article 50 of the EU

Treaty on 29 March 2017 which began the formal process

for withdrawal from the EU, a process eventually

completed in January 2020, the share of UK wood and

wood furniture imports from the EU27 has risen by nearly

10%.

Of course recent trends in UK wood and wood furniture

imports have probably been influenced much more by the

effects of the COVID-19 pandemic than by Brexit. And

since the start of last year, trading patterns in all parts of

Europe have also been impacted by the war in Ukraine.

Therefore these short-term changes in market share may

not be a good guide to the long term effects of Brexit.

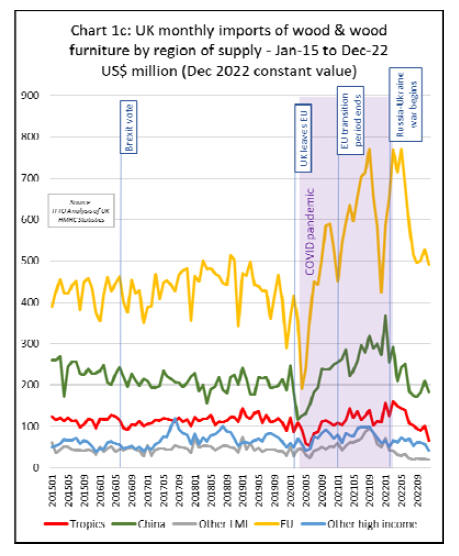

Probably the most notable feature of UK imports in recent

years has been the extraordinary level of volatility. This is

highlighted in Chart 1c which tracks UK import value of

all wood and wood furniture by major region of supply on

a monthly basis since January 2015.

The level of UK trade volatility began to increase soon

after the Brexit vote in June 2015, an event which created

considerable economic uncertainty, compounded by

regular and often confusing alterations to the timetable for

the UK’s departure from the EU, and the lack of clarity on

the trade deal with the EU that would eventually result.

And then just a few weeks after the UK officially left the

EU on 31 January 2020 - with a “harder” Brexit deal than

many expected - the COVID pandemic struck leading to a

very sharp dip in trade during the first lockdown. But this

was followed by a massive and unexpected rebound in

trade, initially as money was poured into home renovation

projects, and then as government stimulus measures, much

focused on the construction sector, began to kick in. These

measures helped maintain a buoyant level of trade until the

middle of last year.

The combination of COVID and Brexit meant that

problems of shipping and transport logistics were

particularly severe in the UK between 2020 and 2022. The

problems of shipping into the UK led to more calls for

distributors and manufacturers to shift away from their

existing "just-in-time" business model to a "just-in-case"

model of bringing more manufacturing closer to home and

increasing inventories once again.

In practice, this implied a continuing high level of

dependence on the large suppliers in continental Europe

for which turnaround times, while much longer than

before the UK left the EU single market, still compared

favourably to imports from other parts of the world.

Demand and trade will be subdued during 2023

What happens next is uncertain. However, the current

economic situation in the UK implies that overall demand,

and the level of trade, will be subdued during 2023. In

early February, the Bank of England forecast that the UK

would enter a shallow but lengthy recession, starting in the

first quarter of this year and lasting five quarters.

UK business groups have said that future investment will

be deterred by a steep increase in taxation on profits that

takes effect in April. Retailers are reported to be cutting

inventory levels due to reduced consumer demand.

Inflation remains high and interest rates are being raised,

increasing the costs of borrowing.

Despite Brexit, EU-based wood suppliers seem certain to

maintain their dominance in the UK market for many

years to come, not least due to their proximity and that

they are particularly well placed to supply the commodity

softwoods and mass-produced furniture on which the UK

relies.

But, equally, opportunities for non-EU wood product

suppliers, including in the tropics, should improve around

the margins of the UK market with the recent dramatic fall

in global freight rates and as the logistical problems that

built up during the pandemic have now eased

considerably.

One indicator is the Drewry global freight rate index

which at US$1,997 per 40-foot container in January was

81% below the peak of US$10,377 reached in September

2021 and was 26% lower than the 10-year average of

US$2,693, indicating a return to more normal prices.

|