|

Report from

Europe

Sharp fall in tropical share of European

wood products

market

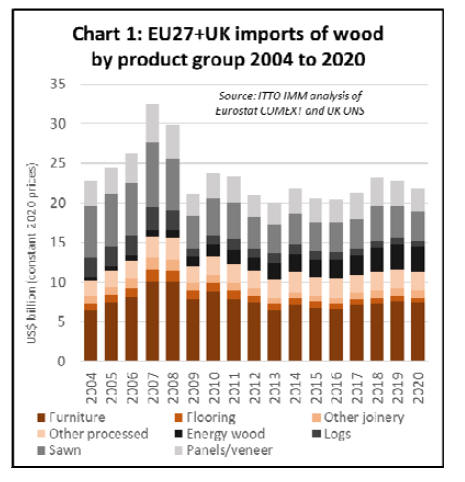

Despite upheaval in the EU27+UK wood market and

wider economy in 2020 due to the COVID-19 pandemic,

the total dollar value of EU27+UK imports of wood

(HS44) and wood furniture (HS94) products fell only 4%

to US$21.86 billion euro in 2020.

In dollar terms, EU27+UK imports in 2020 were higher

than during the 2015-2017 period and not significantly out

of alignment with the trend of the previous 10 years (Chart

1).

While the overall level of EU27+UK imports of wood and

wood furniture products remained surprisingly resilient

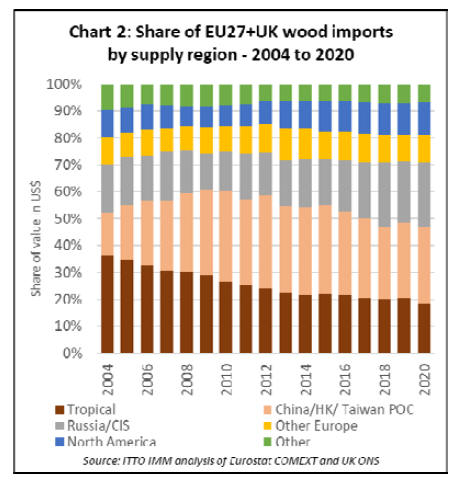

during 2020, there were winners and losers. Unfortunately

for tropical suppliers, their share of the European trade fell

sharply in 2020 after making some tentative gains the

previous year. In total, wood and wood furniture imports

into the EU27+UK from the tropics were US$4.08 billion

in 2020, 13% less than the previous year. The share of

tropical suppliers in the total value of EU27+UK wood

product imports decreased from 20.5% in 2019 to 18.5%

in 2020, the lowest level ever recorded which compares to

a figure of over 35% only 15 years before (Chart 2).

The latest downturn in tropical woodˇŻs share of the

EU27+UK market is partly due to supply side problems in

tropical countries during the pandemic, compounded by

severe lack of container space, particularly in shipments

from South East Asia to Europe.

Another key factor was that in 2020 the pandemic

impacted most heavily on a few western European

countries ¨C notably the UK, Spain, Italy, Belgium and

France ¨C which are the largest markets for tropical wood

and wood furniture products in the region.

At the same time, the largest single market for tropical

wood and wood furniture products in the region ¨C the UK

¨C went through the painful process of removing itself from

the EU, officially leaving the bloc on 31st January 2020

and the single market on 31st December after a brief

transition period last year.

In contrast to tropical countries, the total value of

EU27+UK imports of wood and wood furniture products

from China declined just 3% to US$6.18 billion in 2020,

mainly driven by a slight decline in wood furniture. This

follows marginal 1% gains in EU27+UK import value

from China in 2018 and 2019 after a period of decline

between 2014 and 2017.

EU27+UK imports of wood and wood furniture products

from CIS countries actually increased in 2020, rising 1%

to US$5.27 billion. The share of CIS countries in total

EU27+UK imports increased from 22.9% in 2019 to

24.1% in 2020. EU27+UK imports of softwood

sawnwood, birch plywood and wood furniture from the

CIS region all made gains in 2020 while imports of wood

pellets were stable. EU27+UK imports of wood and wood

furniture products from other non-EU European countries

declined 2% to US$2.17 billion in 2020 and share of

imports from these countries increased slightly, from 9.7%

in 2019 to 9.9% in 2020.

After dipping sharply early in the year, imports from

Norway (mainly softwood logs and sawnwood) and

Bosnia and Herzegovina (mainly wood furniture and some

sawn hardwood) rebounded strongly in the second half of

2020.

However, imports from Switzerland (mainly furniture and

panels), Serbia (mainly furniture), and North Macedonia

(all furniture) were recovering only slowly.

EU27+UK imports of wood and wood furniture products

from North America (excluding Mexico) decreased by just

1% in 2020 to US$2.68 billion. The regionˇŻs share of total

EU27+UK imports increased from 11.8% in 2019 to

12.3% in 2020. Rising imports of pellets offset declining

imports of sawnwood, furniture, and veneers from North

America.

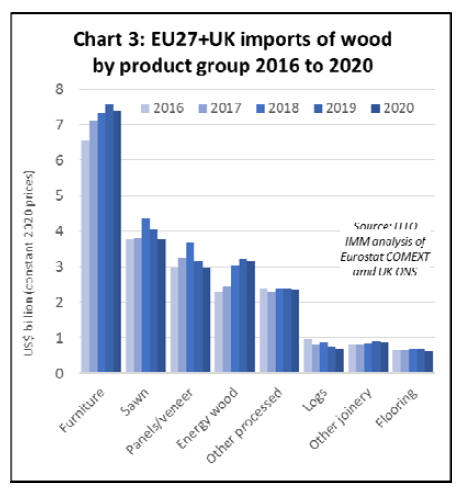

EU wood furniture imports down 3% in 2020

Considering individual products (Chart 3), the dollar value

of EU27+UK imports of wood furniture decreased by 3%

to US$7.4 billion in 2020 after a 4% increase in 2019.

Wood furniture imports from temperate countries fared

much better than imports from tropical countries during

the year.

Imports of wood furniture from China, which alone

accounts for around 50% of the EU27+UK external trade,

declined only 3% to US$3.7 billion. Imports of wood

furniture from all the other leading supply countries in

temperate regions increased during the year including

Turkey (+19% to US$335 billion), Bosnia (+6% to

US$233 billion), Ukraine (+17% to US$215 billion),

Belarus (+28% to US$183 billion) and Serbia (+3% to

US$153 billion).

In contrast, there was a universal fall in imports of wood

furniture from tropical countries in 2020, including

Vietnam (-14% to US$751 billion), Indonesia (-12% to

US$367 billion), India (-6% to US$280 billion), and

Malaysia (-16% to US$222 billion).

Such consistency across the board - with rises in imports

from temperate countries matched by declines from

tropical countries - is unusual.

It may be a short-term adjustment as European importers

switched to more regional suppliers with the sharp drop in

availability of container space and rising freight rates and

other problems in sourcing products from South East Asia

during the pandemic.

On the other hand, it may have long term consequences if

it reinforces the trend towards ˇ®reshoringˇŻ and a preference

for sourcing furniture from neighboring countries in

Eastern Europe on-going now for some time in the region.

A similar trend is apparent for sawnwood. EU27+UK

imports of sawnwood (inclusive of both softwood and

hardwood, and decking) declined 6% to US$3.79 billion in

2020 following a 7% fall the previous year.

The biggest falls in sawnwood imports during 2020 were

all reserved for tropical suppliers. Imports fell 15% from

Cameroon to US$223 million, 12% from Brazil to US$237

million, 17% from Malaysia to US$117 million and 15%

from Indonesia to 114 million.

In contrast to tropical wood, imports of sawnwood from

Russia, by far the largest external supplier, recovered 9%

to US$889 million after falling 11% the previous year.

Imports from Belarus also remained quite stable in 2020,

declining only 2% to US$462 million after a 4% fall the

previous year.

Most sawnwood imports from Russia and Belarus

comprise softwood and lower value hardwood species

such as birch and aspen. EU27+UK imports of sawn wood

from both countries have been high in recent years

following imposition of log export bans.

Imports of sawnwood from Ukraine, comprising a mix of

softwood and hardwood, fell 12% in 2020 to US$310

million following a 13% fall the previous year. Imports

from the United States, almost exclusively hardwood, are

also declining, down 14% to US$291 million in 2020

following a 13% decline the previous year.

EU27+UK imports of plywood and other wood panels

decreased 7% to US$2.95 billion in 2020 after a 14%

decline the previous year.

This European market for plywood and panels weakened

sharply in the second half of 2019 with widespread reports

of overstocking and falling prices as the economy began to

cool at that time. The onset of the pandemic last year

deepened the prevailing downward trend.

With few exceptions, the downturn impacted on all the

leading suppliers of plywood and panels, both in temperate

regions and the tropics. Imports from Russia fell 5% to

US$694 million following a 14% decline the previous

year, similarly China fell 5% to US$510 million in 2020

following a 14% decline in 2019, Ukraine was down 7%

in 2019 and 1% in 2020 to US$304 million, and Brazil fell

16% in 2019 and 26% in 2020 to only US$225 million.

Of temperate suppliers, only Belarus made gains in 2020,

rising 6% to US$249 million but this followed a 19% fall

the previous year.

Amongst tropical suppliers of plywood and panels,

EU27+UK imports declined 30% to US$86 million from

Indonesia in 2020 after a 13% fall the previous year.

However, in 2020 gains were made by Gabon, with

imports rising 13% to US$110 million after a 5% fall the

previous year, and Malaysia, from where imports

increased 5%, to US$37 million, after falling 33% the

previous year.

Following nearly 20 years of almost uninterrupted growth,

the dollar value of EU27+UK imports of energy wood fell

1% to US$3.18 billion in 2020. Imports of energy wood

are now dominated by pellets from North America, Russia

and the CIS countries. Imports from the United States

continued to rise in 2020, by 3% to US$ 1.4 billion, and

also increased 25% from Canada to US$374 billion.

Imports from Russia were US$501 million in 2020, no

change compared to 2019. However, imports from Belarus

fell 3% to US$190 million in 2020. Imports from Ukraine,

which includes much charcoal as well as pellets and other

fuelwood, declined 7% to US$185 million in 2020.

EU27+UK imports of logs declined 8% to US$680 million

in 2020 after a 15% fall the previous year. In 2020,

imports fell from nearly all the countries that continue to

allow log exports, including Russia (-5% to US$290

million), Norway (-15% to US$223 million), Switzerland

(-19% to US$43 million), and USA (-15% to US$35

million).

However, after falling to negligible levels in 2018 and

2019 following imposition of tight export controls, log

imports from Belarus increased sharply last year to US$21

million.

After years of decline, EU27+UK log imports from

tropical countries are now very low and fell from all main

supply countries in 2020, down 15% from Republic of

Congo to US$18.1 million, 31% from Central African

Republic to US$6.2 million, and 44% from DRC to

US$3.7 million.

The value of EU27+UK imports of wood flooring fell 6%

to US$640 million in 2020 after a 3% fall the previous

year.

Flooring imports from China, by far the largest external

supplier accounting for around two thirds of the total,

declined 9% to US$385 million in 2020, while imports

from Ukraine were down 4% to US$97 million. However

flooring imports from Malaysia increased last year, by

25% to US$29 million. Imports from Indonesia were down

4%, to US$21 million, continuing a long-term downward

trend.

EU27+UK imports of ˇ®otherˇŻ joinery products (i.e.

excluding flooring and mainly comprising doors and

laminated wood for window frames and kitchen tops) fell

3% to US$880 million in 2020 after a gain of 5% the

previous year. Imports from China were stable at US$206

million in 2020 after rising 4% in 2019.

However, imports from Indonesia were down 16%, to

US$174 million, reversing the 9% gains made the previous

year. Imports from Malaysia also declined in 2020, by 6%

to US$95 million after rising 10% in 2019. Imports from

Vietnam increased by 1% to US$26.7 million in 2020,

building on a 14% gain in 2019.

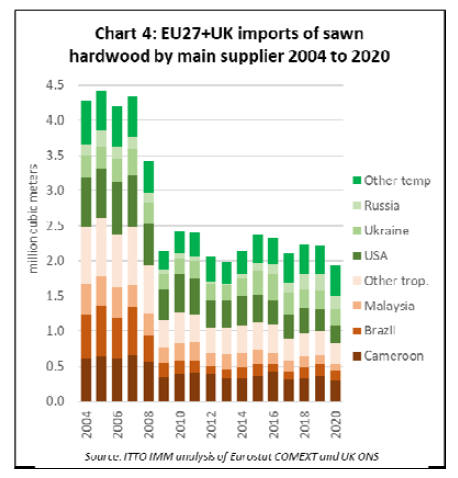

Record low EU27+UK imports of sawn hardwood in

2020

In quantity terms, EU27+UK imports of sawn hardwood

fell 13% to 1.93 million cu.m last year, the lowest level for

at least thirty years and only the second year ever

(alongside 2013 during the euro currency crises) that

imports have fallen below 2 million cu.m. EU27+UK

import quantity of tropical sawn hardwood declined 18%

last year to only 828,000 cu.m, the lowest level ever

recorded. Import quantity of temperate sawn hardwood

fell 8% to 1.11 million cu.m.

Despite the sharp decline in trade, the level of EU27+UK

sawn hardwood imports last year was not significantly out

of alignment with imports in any year since 2009. The

reality is that European sawn hardwood imports have been

stuck at historically low levels ever since the financial

crises. The decline last year is a relatively minor blip

compared to the huge 50% fall between 2007 and 2009

(Chart 4).

In quantity terms, in 2020 EU27+UK imports of tropical

sawnwood declined 17% from Cameroon to 303,000 cu.m,

25% from Brazil to 129,000 cu.m, and 13% from Malaysia

to 105,000 cu.m. Imports of temperate sawn hardwood

also declined from all leading supply countries including

the US (-13% to 261,000 cu.m), Ukraine (-17% to 224,000

cu.m) and Russia (-15% to 197,000 cu.m).

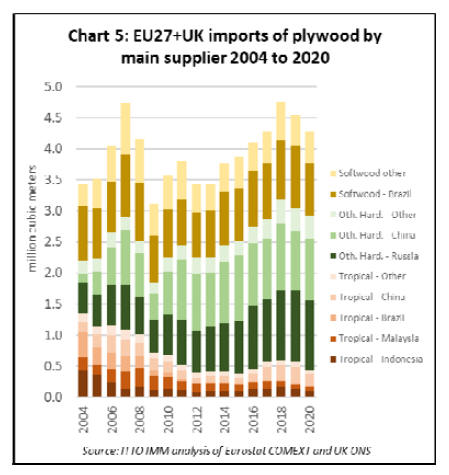

EU27+UK imports of tropical plywood down 22% in

2020

In quantity terms, in 2020 EU27+UK imports of plywood

fell 6% to 4.28 million cu.m following a 5% decline the

previous year. While EU27+UK imports of plywood

declined in both 2019 and 2020, they were still at

historically high levels, last year being the fourth strongest

year for plywood imports in the last 20 years (Chart ).

While overall EU27+UK plywood imports were strong in

2020, there was a significant loss of market share for

tropical products. Imports of tropical hardwood plywood

fell 22% to 441,000 cu.m last year and share of all

plywood import quantity declined from 12% in 2019 to

10% in 2020.

Although imports of tropical hardwood plywood increased

24% from Malaysia to 72,000 cu.m, they declined from

other leading supply countries including Indonesia (-27%

to 104,000 cu.m) and China (-31% to 187,000 cu.m).

In 2020, tropical hardwood plywood lost share mainly to

non-tropical hardwood plywood from China, including

both mixed light hardwood (comprising mainly eucalyptus

and poplar) and birch products. Total EU27+UK imports

of non-tropical hardwood plywood increased 1% to 2.49

million cu.m in 2020.

A 6% increase in imports from China to 998,000 cu.m

offset a 5% decline in imports from Russia to 1.12 million

cu.m. EU27+UK imports of softwood plywood fell 10% to

1.35 million cu.m in 2020, mainly due to a 17% decline in

imports from Brazil to 842,000 cu.m.

|