|

Report from

Europe

ˇ°Greta effectˇ± evident at European trade shows in

opening weeks of 2020

As usual in January, the IMM furniture fair in Cologne

and the Domotex flooring show in Hamburg were key

events for the European wood trade, providing a signal of

market sentiment and an insight into emerging trends.

Official reports from both shows were typically bullish,

implying a high level of underlying confidence in

sophisticated and innovative European manufacturing

sectors.

IMM Cologne reported 1,233 exhibitors from 53 countries

and over 128,000 visitors, up from 125,000 the year

before, with over 50% of the 82,000 trade visitors from

overseas. Domotex reported 35,000 attendees, 70% of

them from abroad, and over 1,400 exhibitors from more

than 60 different nations.

An emphasis on ˇ°sustainabilityˇ± has, of course, been a

common theme running through these and similar shows

in Europe now for several years. However, this year there

was a sense that the environmental issue has become more

urgent, that industry needs to move decisively beyond the

greenwash and that failure to do so voluntarily will almost

certainly lead to imposition of new taxes and regulations.

The intense focus on sustainability at the shows is not so

surprising given the ˇ°Greta effectˇ±, which is galvanising

EU efforts to meet the goals of the Paris climate

agreement, and the timing of the shows so soon after the

launch of the new ˇ°Green Dealˇ± by the European

Commission which aims to make the EU climate neutral

by 2050.

This policy initiative and associated design trends towards

more authentic, natural and carbon neutral products,

higher quality items that are more durable and less often

replaced, and increasing interest in furniture that can be

used interchangeably either inside or out of doors, all have

clear and generally positive implications for wood product

suppliers.

To some extent though, the sunny outlook portrayed in the

publicity for these trade shows, flies in the face of

economic and trade data which suggests that the European

trade in both wood furniture and flooring products, which

has never really recovered the dynamism of the years prior

to the financial crises, was cooling again in 2019.

There is intense competition, which is certainly acting to

spur innovation in some sectors, but the concern is always

that wood manufacturers, particularly those dealing with

solid hardwood, are falling behind in the R&D stakes.

There remains an almost overwhelming focus on the oaklook,

a trend which extends even into artificial surfaces,

which is damaging prospects for wider hardwood market

development.

Slowdown in European wooden furniture consumption

in 2019

In the wooden furniture sector, recent trade trends suggest

a slowdown in overall European consumption, although

there is some positive news for external suppliers who

benefited from increased EU market penetration during

2019.

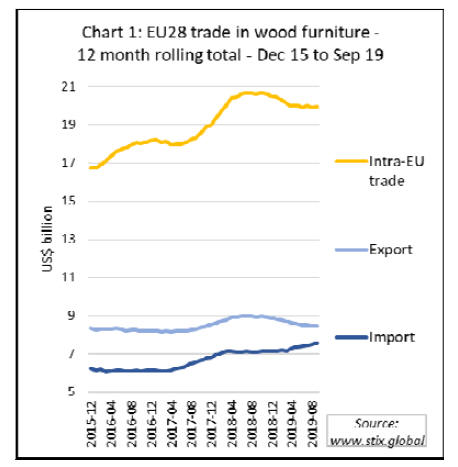

Chart 1, which shows the 12-month rolling total US dollar

value of EU trade in wooden furniture, highlights that

internal EU trade which had been rising strongly in 2018,

fell back sharply in the first quarter of 2019 before

levelling in the in the second half of the year.

Meanwhile EU wooden furniture exports were sliding

consistently throughout 2019 while imports were

beginning to rise. Taken together these trends imply a

slowdown in sales for the EU wooden furniture

manufacturing sector in 2019.

Note: STIX is a joint initiative of The International Tropical Timber

Organisation (ITTO) through the FLEGT Independent Market

Monitoring (IMM) mechanism funded by the EU, and the Global Timber

Forum (GTF).

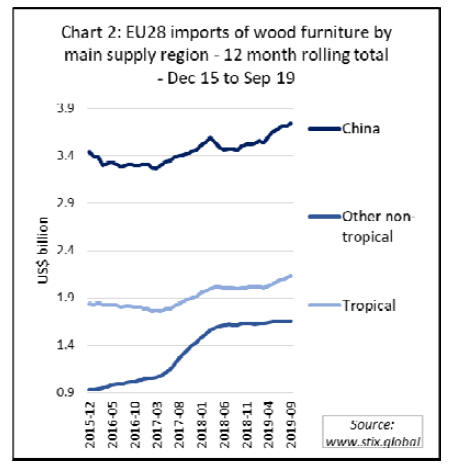

Chart 2 indicates that the main beneficiaries of growth in

EU wooden furniture imports during 2019 were China and

tropical countries. This is in stark contrast to the 2017-

2018 period when EU wooden furniture import growth

was driven by non-tropical countries other than China,

particularly Turkey, Bosnia, US, Serbia, Ukraine and

Belarus.

One reason for this shift in trade is likely to be the USChina

trade dispute which has encouraged Chinese

manufacturers to redirect export sales from the huge US

market into Europe.

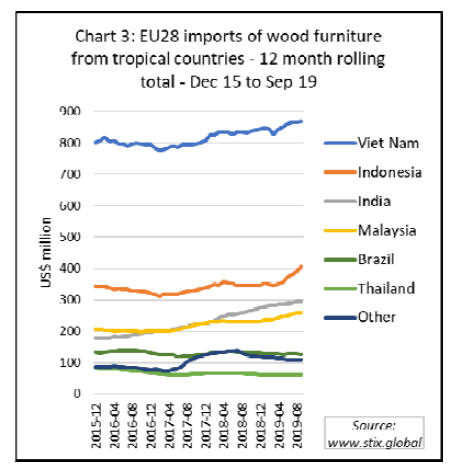

The upturn in EU imports of tropical wooden furniture

products is being driven by a gradual long-term increase in

market penetration by Vietnam and India, combined with a

surge in imports from Indonesia in the second and third

quarters of 2019 (Chart 3).

This last trend may be partly linked to the competitive

advantage for Indonesian furniture in the EU market due

to the FLEGT license which is becoming more of an issue

now that more concerted efforts are being made to enforce

EUTR in the wooden furniture sector.

One indication of this was news in January that a UK

importer, Heartlands Furniture (Wholesale) Ltd, was fined

a total of £13,300 for two EUTR offences dating back to

2017 for failure to undertake adequate due diligence with

respect to a Brazilian pine Corona bed frame from Brazil

and an American oak glass-fronted cabinet from Vietnam.

The recent surge in EU wooden furniture imports from

Indonesia was destined mainly for the Netherlands,

although the UK remains by far the largest destination for

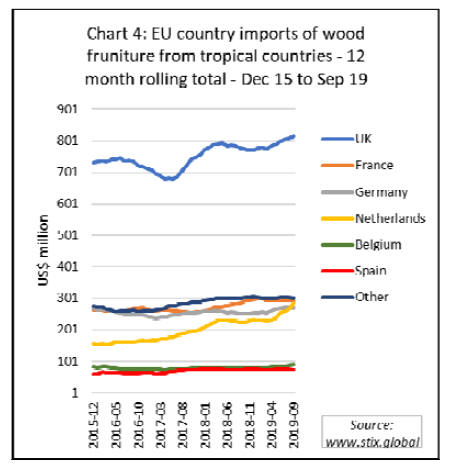

tropical wooden furniture in the EU (Chart 4).

With the UK due to depart from the EU on 31st January,

there are of course profound implications for the overall

EU trade balance in tropical wooden furniture. In the

twelve months to 2019, the UK imported just over

US$800 million of wooden furniture from tropical

countries, nearly 40% of all EU imports from these

countries.

European wood flooring consumption recovers a little

ground in 2019

At the Domotex show, the European parquet floor

association FEP provided a preliminary assessment of the

European wood flooring market in 2019. Drawing on

information from FEP member companies and national

associations, it was estimated that European consumption

was flat overall during the year.

FEP emphasised that this was a first assessment subject to

change in anticipation of the complete data to be

communicated at FEPˇŻs Annual General Assembly due to

be held on 11th and 12th June in Hamburg, Germany.

After a year in 2018 when parquet flooring consumption in

FEP countries fell by 2.3% to 79.9 million m2,

consumption is estimated to have recovered slightly in

2019.

This is mainly due to a moderate upturn in Germany, the

largest European parquet market. Consumption also

improved in Austria, France, Poland and Spain.

However, these positive developments in 2019 were offset

by declining consumption in Italy, Sweden, Switzerland,

and the Nordic Cluster (Denmark, Finland and Norway).

Regarding competition, FEP members emphasised both

the continued rise in market share of products with a

wood-look, especially Luxury Vinyl Tiles (LVT).

They also stressed the uncertainties created by the trade

war between the US and China on global and European

markets.

In contrast, FEP sees the European Green Deal as an

opportunity for the wood flooring industry, particularly

welcoming the strong focus on construction and

renovation.

According to FEP, ˇ°the European Parquet Industry is

offering a circular sustainable product which saves carbon

and substitutes energy-intensive and/or fossil-intensive

alternativesˇ±.

Further information on FEPˇŻs 64th General Assembly and

45th Parquet Congress to be held in Hamburg in June can

be obtained from Isabelle Brose, FEP Managing Director

(isabelle.brose@parquet.net).

Increased import penetration in EU wood flooring

market

When speaking of competition, it is perhaps surprising that

the FEP report on the Domotex meeting made no mention

of imports. Analysis of EU wood flooring trade trends

shows that imports from outside the EU have been rising

strongly since 2017, a trend only moderating in the third

quarter of last year.

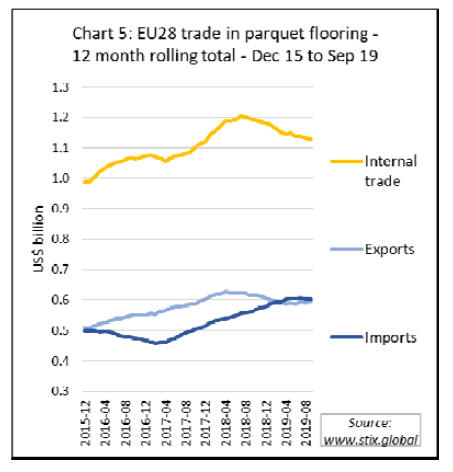

The rise in wood flooring imports from outside the EU

contrasts with the slowing pace of internal EU trade and

EU exports (Chart 5).

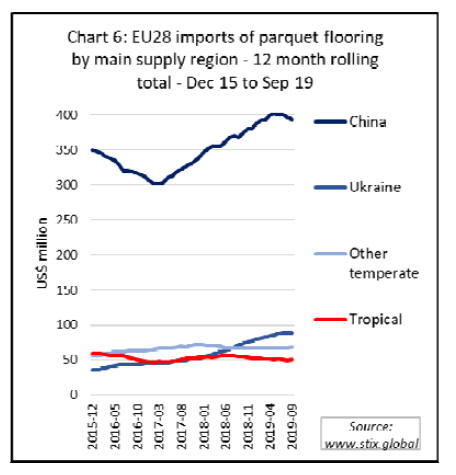

Chart 6 shows that the rise in EU wood flooring imports is

almost all due to China and Ukraine. Imports from China

in the 12 months to September were US$400 million, up

from only US$300 million two years before. During the

same period, imports from Ukraine have nearly doubled

from US$50 million to close to US$100 million.

European laminate flooring sales stabilised in 2019

EuropeˇŻs globally dominant laminate flooring sector is

another key competitor for parquet flooring in Europe. Of

estimated global laminated flooring production of nearly 1

billion m2, the 18 manufacturers in nine European

countries (including in Russia and Turkey) that are

members of the European laminate flooring association

EPLF accounted for around 50% last year. This compares

to global share of around 25% for Chinese manufacturers

and 8% share for US manufacturers.

According to data presented by EPLF at Domotex,

worldwide laminate flooring sales by EPLF members were

446 million sq.m in 2019, a decline of 2% from 454

million sq.m in 2018.

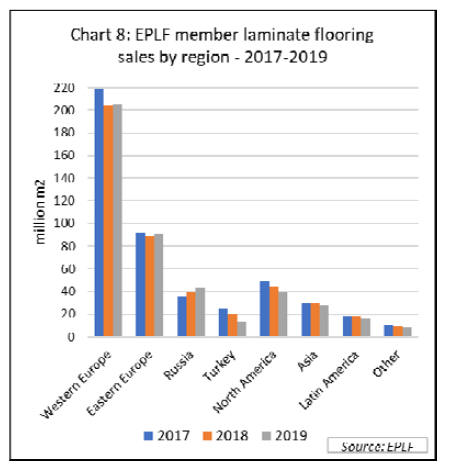

However, after a significant fall in 2018, laminate flooring

sales in Europe stabilised last year. The decline in sales in

2019 was due to a decline outside Europe, notably in

Turkey, North America, and Asia (Chart 8).

Laminate flooring sales continued to fall in Germany in

2019, by far the largest single market in Europe,

accounting for around 50 million sq.m last year, but the

pace of decline has been slowing. Sales in Germany were

down 4% in 2019 compared to a 9% fall the previous year.

The decline in Germany in 2019 was offset by an 8% rise

in sales in the UK, to 33 million sq.m, a 1% rise in France

to 36.5 million sq.m, and a 3% rise in the Netherlands to

18.6 million sq.m.

A clear upward trend is also evident in Eastern Europe

where 2019 sales of 91.2 million sq.m were 3% more than

the previous year, and Russia, where sales increased 11%

to 44 million sq.m.

Laminate flooring is distributed via two major channels

which have been growing at around the same pace in

recent years; specialist wholesalers which supply most

professional floor installers, and DIY retailers that target

the general public.

Key trends in the flooring sector identified by EPLF at

their press conference at Domotex include:

Natural: flooring aims to look and feel ever more

like real wood;

Oak is still the dominant material in real-wood

floors and look in artificial finishes;

Concrete, granite and raw steel are increasingly

used as contrasting elements to wood;

There is a strong focus on improving the water

resistance of floors; and

The use of renewable wood and low-emission

production supports the sustainability of laminate

flooring.

EU ˇ°Green Dealˇ± creates new opportunities for timber

The Green Deal, published on 11 December 2019 by the

new European Commission and adopted by the European

Parliament on 15 January 2020, sets out a three-decade

effort to upend just about every policy area in the EU to

make the bloc climate neutral by 2050. In doing so, it has

real potential to create a policy environment very

favourable for the wood industry.

The strategy includes 50 specific policy measures of

which the flagship is a climate law, to be presented by the

Commission before the end of March, which will commit

the bloc to slash emissions to net zero by 2050, and a plan

to increase the 2030 emissions reduction target to at least

50 percent and "towards" 55 percent from the current 40

percent goal.

The Annex to the Green Deal indicates the Commission

will put forward an EU Industrial Strategy in March, as

well as a new Circular Economy Action Plan. The latter

will include a sustainable product policy with

ˇ°prescriptions on how we make thingsˇ± in order to use less

materials and ensure products can be reused and recycled.

On trade, the Green Deal pledges to make respect of the

Paris Agreement "an essential element for all future

comprehensive trade agreements." Another measure likely

to attract attention ¨C and controversy ¨C is a proposal for a

carbon border tax.

There is also a commitment to building renovation to

improve insulation and reduce energy efficiency. The key

objective there is to ˇ°at least double or even tripleˇ± the

renovation rate of buildings, which currently stands at

around 1%.

On forests, there is a specific objective to promote

products that do not involve deforestation and forest

degradation, to be encouraged through new labelling rules.

There is also recognition that the ˇ°EUˇŻs forested area

needs to improve, both in quality and quantity, for the EU

to reach climate neutrality and a healthy environmentˇ±.

The potential for the strategy to help drive demand for

responsibly sourced wood products is well recognised in

the European wood sector and initiatives are being put in

place to better exploit the opportunities, although there is a

lot of work still to do.

This was highlighted in a recent article for the Timber

Trades Journal by Patrizio Antonicoli, secretary-general of

the European Woodworking Industries Confederation ¨C

CEI Bois. Mr Antonicoli said CEI-Bois has developed

three key assets to underpin the industryˇŻs transition to the

era of the Green Deal.

The CEI-Bois Manifesto for the EU term 2019-2024

illustrates how the European woodworking industry can

help the EU reach key goals, such as reduction of GHG

emissions in line with the Paris Agreement and the

deployment of a circular bio-economy, while ensuring

jobs creation and employment stability.

The Manifesto focuses on six priorities; Wood Availability

and Sustainability, Circular Bioeconomy, Competitiveness

of Wood in Construction, Free but Fair Trade, Research

and Innovation and Industrial Relations & Social Affairs.

The second asset is the wood itself. CEI-BoisˇŻ ˇ°Building

the Bioeconomyˇ± booklet shows how Europe can reduce

emissions by using low carbon, renewable alternatives,

such as timber, over high carbon materials, such as

concrete, steel and plastic.

With this publication, the European wood-working sector

is calling on policy makers to put wood at the centre of

emission reduction and zero carbon strategies and to

recognise it as a model product for transition towards a

circular economy.

Finally, the Forest-Based Industries vision 2050 focuses

on how forest-based solutions can help achieve five

ambitious targets:

To decarbonise Europe by 2050 by substituting

CO2-intensive raw materials and fossil energy

with forest-based alternatives

Eradicate waste in the circular economy, with a

sector target of 90% material collection and 70%

recycling

Drive resource-efficiency in the forest-based

industries value chain by enhancing productivity

Meet demand for raw materials by maximising

new secondary streams and ensuring primary raw

material supply from sustainably managed forests

Satisfy growing demand for climate-friendly

products by increasing use of wood.

Mr Antonicoli concludes, ˇ°we see our sector becoming the

most competitive, sustainable provider of net-zero carbon

solutions through research, break-through technologies,

increased recycling and reuse. Together the European

woodworking industries can ride the Green Deal waveˇ±.

Clarification.

In the 1-15 January 2020 report the term litre was coined by our

correspondent to indicate a small unit of per capita timber

consumtion. This was not an error just an attempt to make for

easy reading. 1 ˇ®litreˇŻ is equivalent to 0.001 cubic metres.

|