|

Report from

Europe

Climate change debate threatens to tip European

hardwood market over the edge

Headline figures for sawn hardwood consumption in

Europe show that demand has been flat for the last decade.

However, these figures obscure major underlying changes

in the European market.

This was clear from presentations and discussion during

the International Hardwood Conference (IHC) in Berlin

during November, an event co-organised by the European

Organisation of Sawmill Industries (EOS), the European

Timber Trade Federation (ETTF) and German Sawmill

and Wood Industries Association (DeSH).

There was a widespread view that new opportunities are

emerging, particularly driven by strong political and

emerging consumer interest in carbon mitigation and other

environmental concerns. However, it also became

apparent that other factors are undermining the ability of

the hardwood sector to respond to these opportunities.

The European hardwood market has become too narrowly

focused on a single species, oak, and there has been

insufficient focus on driving demand for and adding value

to other species.

Lack of investment in hardwood market development in

Europe has contributed to a large proportion of logs being

exported, particularly to China, a market which has lately

become very volatile.

Supply side problems are also arising as drought and pest

infestations in Europe have led to large volumes of lowquality

hardwood being placed on the market contributing

to falling prices for low grade lumber and by-products

such as chips, sawdust and bark.

There is also uncertainty over long term supply security.

Lack of consistent and harmonised inventory data across

Europe, combined with resource changes due to climate

change, have made projections of future supplies less

reliable.

In retrospect too, the almost exclusive focus on

certification in environmental communication may have

been a distraction from pressing environmental

imperatives in the hardwood sector that are not addressed

in existing certification frameworks.

These imperatives include the need to:

ensure that consumers buy the full range of

hardwood species and grades that the forest can

produce sustainably;

promote efficient processing and use to minimise

waste and maximise yield and value;

provide transparent data on the likely long-term

availability of different hardwood species;

respond effectively to changes in the resource due

to climate and other environmental impacts and

past management decisions (and failures);

remove illegal wood from hardwood supply

chains while promoting market access for legal

operators (both large and small); and

better demonstrate and exploit the carbon

mitigation potential of hardwood products.

Eastward shift in European hardwood consumption

According to data presented to IHC by Rupert Oliver,

Trade Analyst to the FLEGT IMM, the ITTO project

supported by the EU, EU-wide sawn hardwood

consumption was around 9.98 million m3 in 2018, 3%

more than in 2017. EU sawn hardwood consumption was

projected to have fallen back again to around the 2017

level in 2019.

Despite these minor ups and downs, overall sawn

hardwood consumption in the EU in the 2017-2019 period

remained firmly within the narrow band of 9.5 to 10.5

million m3 per year prevailing since 2009 and well down

on figures closer to 15.0 million m3 typical before the

financial crises.

Underlying these recent trends, said Mr Oliver, was

reasonably robust, if unexciting, growth in EU GDP and

construction in 2017-2018 and the first half of 2019.

However, economic uncertainty contributed to slowing

sawn hardwood trade in the second half of 2019.

Mr Oliver noted that the latest data from the joinery sector

shows that wood generally was holding its own against

other materials in doors and window manufacturing,

although much of this benefit may have accrued to

softwoods rather than hardwoods.

Mr Oliver said that EU wood furniture manufacturers are

continuing to maintain their dominance of domestic

markets and holding their own against imports. While

there is some weakness in EU wood furniture production

in western Europe, this is offset by a rise in Eastern

Europe.

Mr OliverˇŻs data showed that per capita sawn hardwood

consumption in western European countries remains low,

typically less than 20 litres per year, and the trend is either

flat or sliding downwards.

In contrast, per capita sawn hardwood consumption is

generally rising in eastern Europe and already exceeds 100

litres per year in the Baltic States and is approaching 60

litres per year in Romania.

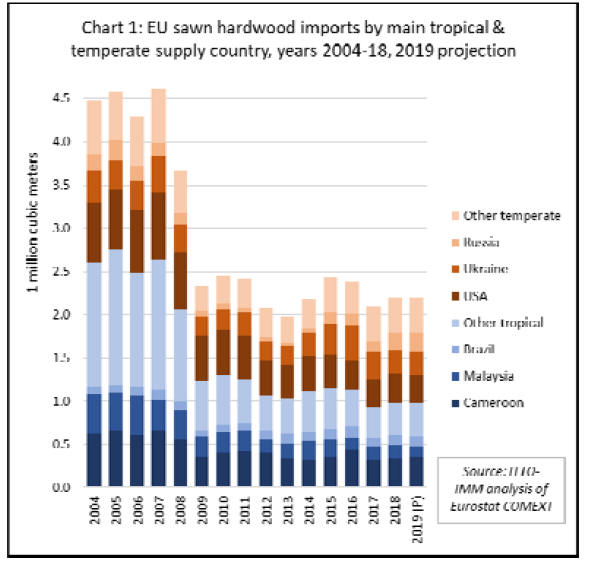

Mr. Oliver estimated that EU imports of sawn hardwood

from outside the region were around 2.2 million cubic

meters in 2019, very similar to the level in 2018,

maintaining the gains made compared to 2017, but still

down on imports of 2.4 million m3 in 2015 and 2016, and

only half of the level of before the financial crises (Chart

1).

Mr Oliver noted that eastward shift in manufacturing in

Europe has been linked to a partial shift towards East

European and CIS hardwood suppliers in recent years,

with most growth in EU sawn hardwood imports coming

from Ukraine and Bosnia in 2016 and 2017, and Russia

and Serbia in 2018 and 2019.

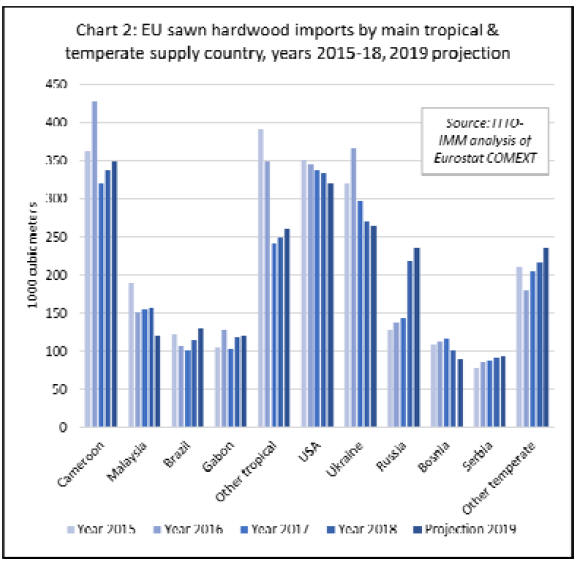

According to Mr Oliver, total imports of tropical

sawnwood are projected to be 980,000 m3 in 2019,

marginally down from 993,000 m3 in 2018. Imports from

Cameroon and Brazil recovered some ground in 2019,

helping to offset a significant fall in imports from

Malaysia (Chart 2).

Expanding scope of TLAS and due diligence

regulations in tropical trade

Mr Oliver also commented on the evolving situation in

relation to legality verification, due diligence regulations

and certification in the international tropical hardwood

trade.

He highlighted the considerable scope of efforts to

develop Timber Legality Assurance Systems (TLAS) in

tropical countries, a process encouraged by the EUˇŻs

FLEGT Action Plan.

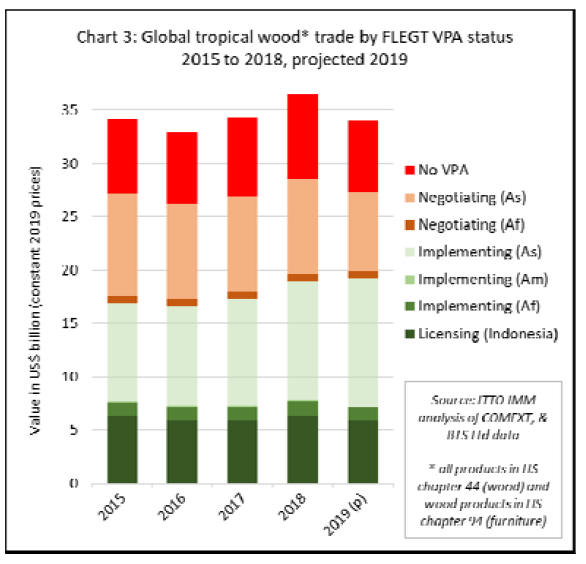

According to Mr Oliver, tropical countries that are either

already issuing FLEGT licences or in the process of

implementing a FLEGT licensing system accounted for

57% of global the value of trade in tropical wood and

wood furniture products in 2019, up from 52% in 2018

(Chart 3).

The rising share of FLEGT partner countries in tropical

trade last year was driven mainly by a sharp rise in exports

by Vietnam, a country which has set an initial objective of

establishing a FLEGT licensing system by the end of 2020

(although this plan is acknowledged to be ambitious and

time scales and activities are likely to be adjusted with

experience).

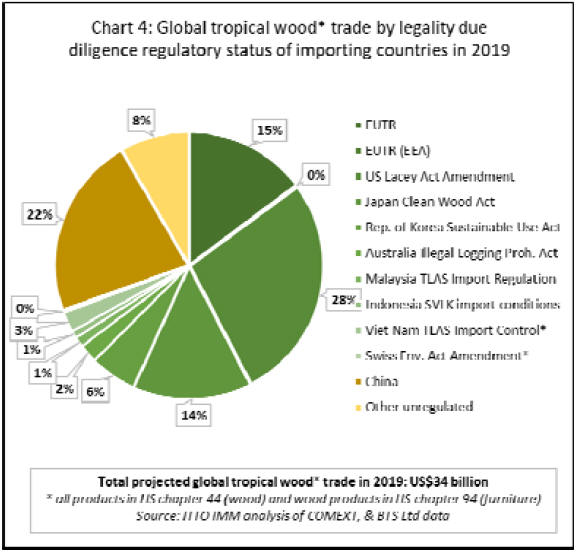

The work by tropical countries to implement TLAS is

mirrored by the wide range of countries that have

introduced regulatory measures requiring legality due

diligence for timber products in trade. According to Mr

Oliver, in 2019 around 70% of the total global value of

tropical wood and wood furniture trade is imported by

countries implementing such legislation, including the US

(28%), EU (15%), Japan (14%), South Korea (6%), and

Vietnam (3%) (Chart 4).

Mr Oliver said the widespread evolution of TLAS in

tropical timber supplying countries contrasts with the

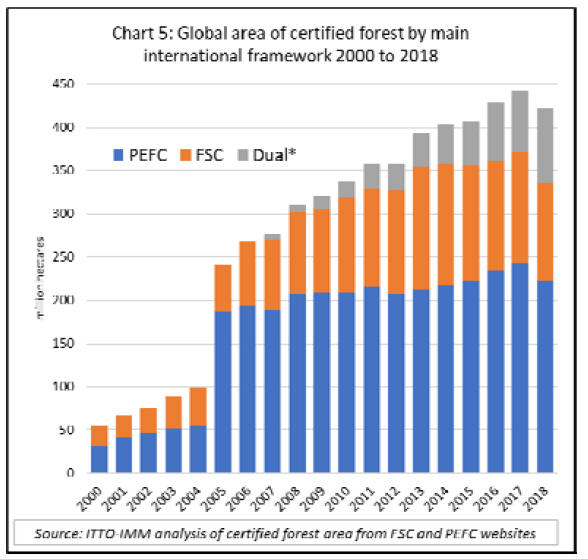

implementation of forest certification. Analysis of data

from FSC and PEFC suggests that the total area of forest

certified by these schemes worldwide actually declined for

the first time in 2018.

Although FSC and PEFC both reported either stable, or a

slight increase in their own certified forest area during the

year, this was only because of a rise in the area dual

certified to both schemes (Chart 5).

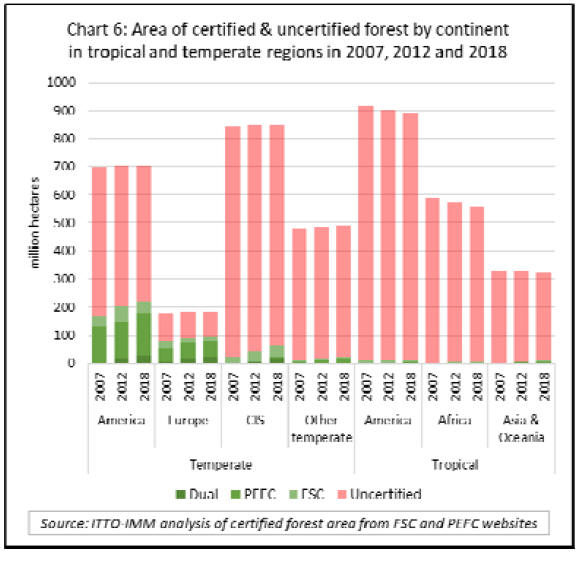

According to Mr Oliver, closer analysis of the data reveals

that most new certificates issued in recent years have been

for large state-owned and industry managed lands in

temperate and boreal regions, particularly in Russia.

Tropical countries and small non-industrial operators

remain seriously under-represented amongst certified

forest areas (Chart 6).

Certification necessary to overcome market

prejudices: a widespread view

While tropical countries are making headway to

implement TLAS systems, tropical wood promotion

activities in the EU is remains heavily oriented towards

certified products.

There is a strong view in parts of the EU timber trade and

industry that the market is so prejudiced against tropical

timber that nothing short of assurance of full conformance

to FSC and/or PEFC certification will overcome this bias

(and even this may not be enough for some influential

European specifiers and buyers).

Although not said explicitly, this was an underlying

narrative behind the presentation to IHC by Mr. Benoît

Jobb¨¦-Duval, Managing Director of the International

Tropical Timber Technical Association (ATIBT).

Mr. Jobb¨¦-Duval provided an update on two years of

progress to implement the Fair & Precious (F&P) ˇ°verified

sustainableˇ± tropical timber branding campaign in Europe.

This campaign, which ATIBT is implementing in

cooperation with various agencies including STTC, FAO,

European timber associations (including the European

TTF and national associations in Belgium, France,

Germany, UK, Fedustria), promotes FSC and PEFC

certified tropical timber.

The key message of the campaign, and the 10

commitments made by organisations adopting the brand, is

that FSC and PEFC certified forest operations directly

contribute to the delivery of the UN Sustainable

Development Goals in tropical countries.

M.r Jobb¨¦-Duval noted that three separate F&P

communication campaigns have been launched targeting

15,000 architects, specifiers, and potential buyers of

tropical timber, covering France, UK, Germany, Italy,

Spain and the Netherlands. Seventy-seven press articles

have been published so far reaching a total audience of 1.2

million.

A new F&P website (https://www.fair-and-precious.org)

was launched in October 2019, and a series of press trips

are planned in certified forest concessions. Social media

campaigns are underway through Instagram and Linked

In. Seventeen organisations are now F&P partners and the

number is gradually rising.

In France, said Mr. Jobb¨¦-Duval, a successful partnership

has been formed between F&P and the national railway

operator SNCF that now acknowledges the environmental

benefits of certified tropical timber and actively promotes

its wider use in the French rail sector.

ATIBT has also contributed to efforts, alongside STTC,

and the Danish offices of various organisations including

WWF and FSC, to rectify an effective ban on all tropical

timber in products certified by Nordic Swan, the official

ecolabel of the Nordic countries.

The label can be voluntarily applied to products in 60

categories groups, the most relevant for tropical timber

being furniture, outdoor furniture and playground fittings,

construction and façade panels, and windows and exterior

doors.

Mr. Jobb¨¦-Duval said that besides insisting that all timber

products bearing the Ecolabel were 70% FSC or PEFC

certified, with the remainder FSC controlled wood or from

PEFC controlled sources, Nordic Swan has drawn up an

82-strong list of species, dominated by tropical wood, that

it would not cover irrespective of whether or not certified.

As well as many lesser-known species, these included

many commercial species widely available and sold in

Scandinavia and the rest of Europe. Among them are ip¨¦,

doussie, jatoba, movingui and okoum¨¦.

Qualifications for being put on the prohibited list were

CITES listing, and inclusion on the IUCN red list

(categorized as critically endangered (CR)), endangered

(EN), vulnerable (VU) and relevant species as Near

Threatened (NT).

The decision to ban all these species from use in labelled

products takes no account of the fact that species listed in

CITES Appendices are not prohibited from exploitation

and sustainable use is often the best form of protection.

Mr. Benoît Jobb¨¦-Duval reported that a decision on this

policy is still pending by Nordic Swan (the ˇ°Forestry

Requirementsˇ± for the label reported on the Nordic Swan

website in mid-January 2020 continue to include over 80

species of mainly tropical timber prohibited from use in

labelled products).

Deteriorating market and supply challenges for

European hardwood

The market situation for German hardwoods was

described at IHC by Steffen Rathke, Vice President of

DeSH who said that both domestic and export market

demand deteriorated in the second half of 2019, partly a

response to responding to mounting economic uncertainty

in Europe and China, the main export market.

Mr. Rathke also highlighted that raw material availability

is becoming more challenging in the hardwood sector with

pests and drought having an increasing impact. Mills are

having to cut back on production of beech because of

severe damage to logs during lengthy periods of drought in

recent years. Although the freshly harvested beech logs

often appear unblemished on the outside, the timber

contains a lot of defect and the yield of higher-grade

lumber is negligible.

Referring to a previous period when the export market for

European beech logs was severely undermined by

shipment of a lot of low quality (in this instance stormthrown)

beech, Mr. Rathke said that ˇ°it is has taken 15

years to get the beech market back in China, but now

again we are seeing more of these lower quality being sent

to China and we could lose this market againˇ±.

Mr. Rathke also expressed concern about the possibility of

a similar fate for oak with a rising incidence of worm

holes, which cannot be detected when logs are inspected in

the forest, also caused by drier conditions.

ˇ°Our trees are under stressˇ±, concluded Mr Rathke, ˇ°the

industry needs to do more to help forest owners, to bring

out the dead wood out, to replant and re-establish the

forest resourceˇ±.

A similar narrative emerged from a review of the wider

market for European hardwoods delivered to IHC by

Maria Kiefer-Polz, EOS Vice President for Hardwood.

She emphasised the rising impact of drought, pest and

disease increasing hardwood forest mortality and leading

to rising proportion of logs of lower grade being placed on

market and contributing in turn to a significant fall in

prices for chips, sawdust and bark, undermining the

profitability of hardwood sawmills.

There has also been a decrease in demand and prices for

packaging wood in parts of Europe due to a large increase

in low grade softwood on the market following a major

bark beetle infestation.

Ms. Kiefer-Polz said that the pressure on supply of

European oak eased during 2019 in response to cooling

demand both in Asia and Europe. Although prices for

higher grades of European oak logs had remained

reasonably stable, prices for lower quality oak logs were

down around 15% during the year. Longer term supply

problems are expected with rising oak mortality in the face

of drought.

European beech prices were also easing in 2019, with log

prices down around 15% due to lower log exports,

particularly to China. Demand for beech sawnwood is also

slowing in China. French beech sawmills are suffering

from falling prices in the context of rising raw material

availability and declining export demand.

Drought has meant there are now 700,000 m3 of dead

beech trees in Eastern France.

European ash log prices have remained high, benefitting

for some extent from this species popularity as a cheaper

alternative to oak. There has been particularly strong

demand for French ash logs in Viet Nam.

However, ash dieback is now hitting the European ash

resource hard and led to a rise in production which is

expected to be short-lived.

In Romania, according to Ms. Kiefer-Polz, there has been

falling export demand in China, North Africa and the

Middle East, traditionally the major markets for Romanian

sawn hardwood. RomaniaˇŻs domestic furniture industry is

also declining and consuming less hardwood, while

RomaniaˇŻs imports of furniture are rising.

Prices for Romanian sawn hardwood are falling and

warehouse stocks were rising in the second half of 2019.

Romanian sawn hardwood production is being curtailed

and is expected to be down up to 15% overall in 2019.

The whole wood sector in Romania is suffering from lack

of access to finance and low levels of investment.

The market situation of European hardwoods is made

more challenging by lack of reliable data on the resource

and understanding of the changing resource dynamics as

the climate changes. This issue was highlighted at IHC in

a presentation by Gert-Jan Nabuurs, Professor at the

Wageningen University and lead scientist for European

forests.

Surprisingly, given the long tradition of systematic forest

management in Europe and widespread perception of a

stable well-managed resource, Professor Nabuurs

commented that ˇ°We know very little about hardwood

stocks, increment, and diameters [in Europe]. Data

gathering needs to improve. EU member states are not

sufficiently open with national forest inventory data and

inventory methodologies are inconsistent between

countriesˇ±.

This in turn had contributed to a situation where ˇ°the

hardwood processing sector is not ready for the challenges

coming at us; climate change, matching regional demandsupply,

and fragmented ownership. The hardwood sector

needs much stronger collaboration between forest owners

and industry and much greater investment in forest

resourcesˇ±.

On the changing composition of the European hardwood

forest, Professor Nabuurs suggested that ˇ°there will be

more beech, but even this species is suffering. We hardly

know how fast the ash decline is taking place. Overall

there are some indications that we are eating up quality

[hardwood] stocksˇ±.

US hardwood struggles in face of China trade dispute

The US hardwood industry is also facing challenges,

though for different reasons, according to American

Hardwood Export Council (AHEC) Executive Director

Mike Snow. From 2009 to 2017, US hardwood exports to

China had ˇ®explodedˇŻ. By 2018, one out of every four

boards of graded hardwood lumber produced in the United

States was destined for China.

However, this left the sector especially vulnerable to the

on-going US-China trade dispute. In fact, since the dispute

started, American hardwood sales lost in China have

exceeded total US hardwood exports to Europe and the

rest of Asia put together.

In the first eleven months of 2019, US sawn hardwood

exports to China were down 40%, with red oak and ash

each falling 38%, and white oak down 45%. China is not a

market that can be easily replaced. The loss of export sales

has been ˇ°absolutely devastating for the industryˇ± said Mr

Snow.

Mr Snow noted that US hardwood exports were hit

particularly hard by ChinaˇŻs immediate reaction to the

trade dispute.

ˇ°At the same time as imposing a 10% tariff on US

imports, China allowed the RMB to devalue, effectively

increasing their cost still further,ˇ± said Mr. Snow.

While the only real solution, said Mr. Snow, was

resolution of the trade dispute, he added that the US

hardwood industry needs also to invest more in domestic

market promotion. US domestic consumption of hardwood

is driven by industrial applications, such as packaging and

pallets, rig mats used in the oil and gas industry, and

railroad ties, which collectively account for almost 60% of

volume. Although volumes are large in these sectors,

profitability is low.

Despite the current challenges for US hardwood in China,

caused by the trade dispute, and signs that the wider

Chinese economy is slowing, Mr. Snow suggested that this

country still offered significant opportunities for the

hardwood sector.

ˇ°China still has major hardwood growth potential, with

development of its western provinces and huge investment

in its belt and road programme, in particular, set to

increase its consumption still further,ˇ± he said. ˇ°But at the

same time, thereˇŻs realisation in the US hardwood sector

that it must diversify exports ¨C and grow its domestic

market. It canˇŻt afford to put all its eggs in the China

basket.ˇ±

Major focus on American red oak promotion in Europe

David Venables, AHEC Europe Director, highlighted that

the sharp downturn in US exports of hardwoods to China

has important implications for the market development of

American hardwoods in Europe. Specifically, it has

greatly increased availability of red oak, a species which is

largest single component of the US hardwood forest and

which previously dominated exports to China.

American exporters now need a new outlet for red oak

which traditionally has not been favoured in Europe.

Europeans have always tended to favour white oak which

closely matches the European oak familiar to European

manufacturers.

Mr. Venables observed that in recent years there has been

strong demand for European and American white oak

while supplies have come under pressure, pushing prices

higher. The market has been looking for more options,

initially turning to ash as the grain and colour is similar

and availability has been high in the short term, due to

dieback in Europe and the Emerald Ash Borer outbreak in

America.

Red oak provides another option, particularly as prices are

currently much lower than for white oak. However, Mr.

Venables noted that amongst European importers and

manufacturers there has been a negative attitude to red oak

with questions raised over its colour, performance and

durability.

Mr. Venables said that this view stems largely from lack

of knowledge, experience and familiarity with red oak in

Europe. However, AHEC has found, through regular

contacts with the European design community, that they

are often very responsive to red oakˇŻs appearance. Those

manufacturers that can be persuaded to use red oak have

come quickly to appreciate its strong technical

characteristics.

AHECˇŻs strategy for red oak aims to supplement, but not

replace, the existing demand for white oak in Europe. The

main target group is designers, building on their evident

interest in the wood, but also involves efforts to educate

and inform European manufacturers and importers of the

opportunity offered from increased sales and use of red

oak.

Testing has also been undertaken to better assess and

document the technical performance of red oak, to

demonstrate that it is at least as good as other oaks, and to

highlight its versatility, especially on finishes. There is

also a major focus on red oakˇŻs vast resource base,

consistent supply, and sustainability.

M.r Venables said that throughout 1919 and 2020 AHEC

is engaged in multiple red oak design and building projects

across Europe to generate a constant flow of publicity.

These are being linked with targeted online and social

media campaigns.

Meanwhile, AHEC continues to development work on

new hardwood applications in Europe. AHEC has worked

with specifiers and designers on hardwood projects,

including the worldˇŻs first cross laminated hardwood

building, a cancer care centre near Manchester in the UK

built with a core structure of American tulipwood CLT

and clad with thermo-treated tulipwood.

Mr. Venables also described the range of tools AHEC has

developed to demonstrate and promote US hardwoodsˇŻ

environmental credentials. These include an interactive

map showing forest growth and timber harvest, a life cycle

analysis (LCA) tool for US hardwood species and the

American Hardwood Environmental Profile (AHEP),

which details the carbon and wider environmental impacts

of hardwood consignments shipped anywhere in the

world.

In all these tools, emphasis is placed on providing easy

access to data individually tailored for all commercially

available American hardwood species. According to Mr.

Venables, this helps ˇ°avoid too much focus on just a

narrow range of hardwood types. Our resource cannot be

sustainably managed unless we encourage use of the

whole portfolio of speciesˇ±.

Mr. Venables emphasised that ˇ°in the hardwood sector, we

have one of the worldˇŻs the most sustainable materials, a

fact not yet widely recognised. We need to broaden the

discussion away from just certification and to innovate in

our communication.

For technical reasons, we canˇŻt offer certified volume, so

instead we have developed an interactive map, making US

forest inventory data accessible to end users and

specifiersˇ±.

He went on, ˇ°we have also reviewed and updated the

Seneca Creek study, first commissioned by AHEC in

2008, which demonstrates that American hardwood forests

are sustainably managed and that there is a negligible risk,

certainly much less than 1%, of any illegal wood entering

the US hardwood supply chain. Through our LCA work,

we prove to specifiers and our customers that we are

supplying not only a technically superior material, but also

a carbon storeˇ±.

North

|