|

Report from

Europe

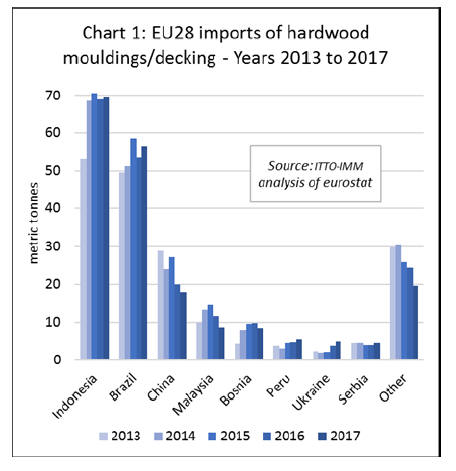

EU imports of hardwood mouldings led by Indonesia

and Brazil

EU imports of ˇ°continuously shapedˇ± wood (HS code

4409) includes both decking products and interior

decorative products like moulded skirting and beading.

Total EU imports of hardwood products under this

heading declined by just over 3% in 2017, to 122,800

metric tonnes (MT). However, imports from Indonesia and

Brazil, the two largest suppliers, increased last year.

IndonesiaˇŻs leading role as a supplier of this commodity

group to the EU is due both to the popularity of bangkirai

for decking applications in Europe, and to IndonesiaˇŻs ban

on rough sawn exports encouraging greater focus on

profiled products. After a steep rise in 2014, imports from

Indonesia remained broadly flat in the next three years and

were 69,600 MT in 2017, 1% more than the previous year

(Chart 1).

Brazil has access to several Amazonian species like ipe,

garapa and massaranduba that perform well as decking

timbers. Following a 9% decline in 2016, EU imports from

Brazil rebounded 6% to 56,600 MT in 2017.

ChinaˇŻs trade in this commodity with the EU has been

declining in recent years owing both to rising costs of

production in China and declining availability of raw

material. Imports from China fell a further 10% to 18,000

MT in 2017. China depends on imported tropical timber

with a strong preference for teak in the decking sector.

China also supplies small quantities of interior hardwood

mouldings to the EU market.

While total EU trade in decking and similar garden

products has been gradually increasing in recent years due

to a slow improvement in EU construction activity,

tropical timber faces intense competition from substitute

materials in this sector, notably Wood Plastic Composites

(WPC), thermally and chemically modified European

hardwoods and softwoods, and preservative-treated

softwoods.

Tropical hardwood decorative mouldings for interior use

are also being replaced by European timbers and MDF.

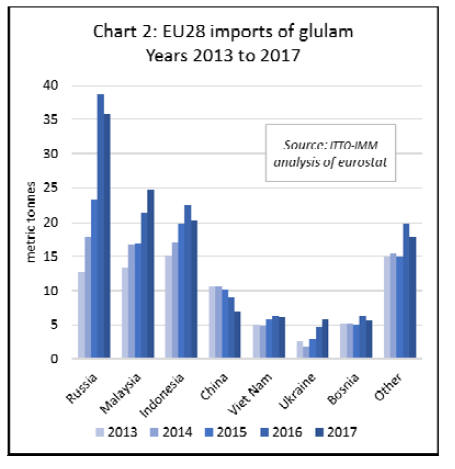

EU market for glulam challenging for external

suppliers

Anecdotal reports indicate that the glulam sector in Europe

struggled with over-supply and low margins in the 2013 to

2016 period. Taken together these trends suggest relatively

poor prospects for external suppliers to expand glulam

sales in the EU market.

Nevertheless, EU imports of glulam were increasing

between 2013 and 2016 when they reached a peak of

128,700 MT. Last year total imports fell back 4% to

123,300 MT, but Malaysia, the leading tropical supplier,

continued to make gains. Imports from Malaysia increased

16% to 24,800 MT in 2017 (Chart 2).

In contrast to Malaysia, in 2017 imports from Indonesia

declined by nearly 10% to 20,300 MT and imports from

Viet Nam fell nearly 4% 6,100 MT. Imports also fell 8%

from Russia to 35,800 MT and 24% from China to 6,900

MT.

The relative strength of tropical glulam imports at a time

of intense competition in the wider EU glulam market is

partly due to the specific mix of products involved.

Whereas much of the EU internal market comprises large

beams and other structural elements, a large proportion of

imports are more specialised small dimension products for

non-structural applications.

Imports of tropical glulam have remained reasonably

buoyant in response to improved demand in specific niche

sectors, notably for durable laminated window scantlings

in the Netherlands and Belgium.

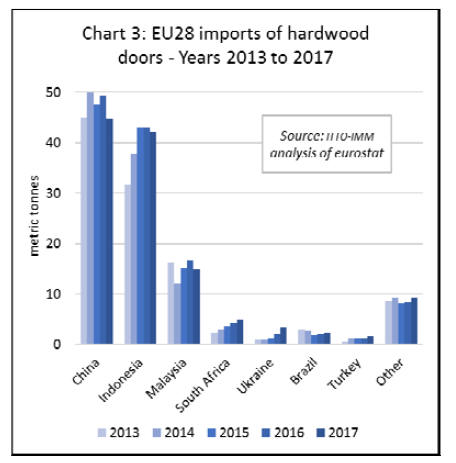

EU imports of wooden doors lose ground in 2017

Most new wood door installations in the EU comprise

domestically manufactured products. Imports from outside

the bloc account for less than 5% of total consumption

value in the EU. Imports from the three largest non-EU

countries ¨C China, Indonesia and Malaysia ¨C all lost

ground in 2017. However, imports increased from several

smaller external suppliers last year, including South

Africa, Ukraine, Brazil and Turkey (Chart 3).

In 2017, EU imports of wood doors fell 9% to 44,700 MT

from China, 2% to 42,100 MT from Indonesia, and 11% to

14,900 MT from Malaysia. In contrast, imports increased

11% to 4,800 MT from South Africa, 69% to 3,300 MT

from Ukraine, 14% to 2,300 MT from Brazil, and 14% to

1,500 MT from Turkey.

The European wood door sector is increasingly dominated

by products manufactured using veneered panels and

finger-jointed timbers rather than from solid timber.

Requirements to comply with higher energy efficiency

standards and efforts to provide customers with long-life

time guarantees are driving this concerted shift to

engineered wood products.

Doors with a real wood veneer have also been losing share

to doors manufactured using High Pressure Laminate

(HPL) foils and white lacquered products. This is partly

due to a shift in overall door production from Southern

European countries such as Spain and Italy, which

strongly favoured real wood veneer, to Germany where

there is a very sophisticated foil and laminates industry.

German slowdown dampens European wood flooring

demand

An insight into the current status of the EU wood flooring

market and the wider economic situation in individual EU

countries is provided by the report of the meeting on 4

April 2018 of the Board of Directors of the European

Federation of the Parquet Industry (FEP).

According to the report, compared to the same period last

year, provisional results for the first quarter of 2018 point

to a continuation of the moderately positive European

parquet consumption trends observed in 2017 with the

exception of Germany which is reporting a significant

decrease.

The report notes that new build projects are the main

driver of the market for wood flooring in Europe, although

renovation is creates significant additional activity.

It also notes that despite the long and wet winter in

Europe, the availability of raw material is not a critical

issue for the time being. This implies some easing of the

supply problems that have emerged in recent years owing

to the sectors very heavy reliance on oak which now

accounts for around 80% of production.

The report includes a rapid-fire appraisal of the market

situation in each of the countries represented by the FEP

membership:

Austria: parquet sales continued to increase by 2% in the

first quarter 2018 compared to the same period last year.

Belgium: parquet sales are estimated to have 3% during

the first three months of 2018.

Baltic States: Baltic countriesˇŻ markets showed a slightly

positive trend in the first quarter 2018.

Denmark: The Danish parquet market remains flat overall,

a decrease in the retail market is compensated by rising

demand from building contracts and projects.

Finland: parquet sales increased by 1% in the first quarter,

mainly driven by moderate growth in large projects while

the residential market is stable.

France: parquet sales are gradually recovering, rising an

estimated 2% in the first quarter of 2018.

Germany: parquet sales are estimated to have fallen 5% in

the first quarter of 2018 compared to the same period in

2017.

This decrease reflects the subdued residential market, a

lack of installation professionals, intense competition from

ˇ°wood lookˇ± floor coverings, and diminishing store space

allocated for hardwood flooring by DIY retailers.

Italy: parquet sales increased 2% in the first quarter of

2018 and continue to benefit from more positive economic

developments in the country.

Netherlands: parquet sales increased by an estimated 3%

during the first quarter 2018 in line with improving

economic conditions in the country.

Norway: the market was flat with some signs of slight

improvement (less than 1% growth) during the first

months of 2018.

Spain: despite the turbulent political situation, the Spanish

market expanded slowly by between 1% and 2% in the

first quarter of 2018.

Sweden: parquet consumption increased 2% in the first

quarter. Declining retail sales were offset by increased

demand from building projects. Sweden is currently the

most dynamic market in Scandinavia.

Switzerland: parquet consumption remains flat but at a

high level with numerous large on-going renovation

projects.

Weak start to the year in UK construction sector

As a country without a significant domestic flooring

manufacturing sector, the UK is the only large EU

consuming country not covered in the FEPˇŻs rapid

appraisal of market conditions. However, information

from the UK Construction Products Association (CPA)

indicates market conditions for flooring and other joinery

products in the UK deteriorated in the opening months of

2018.

According to the CPAˇŻs market statement for the first

quarter of 2018, the start of the year was a bad one for UK

construction. Carillion, the UKˇŻs second biggest

contractor, went into liquidation in January and this led to

an hiatus on infrastructure and commercial projects. Poor

weather also badly affected work on site in February and

March and, as a result, 2018 Q1 construction was around

£1.5 billion lower than in 2017 Q4.

The CTA statement goes on to note that construction

activity in the UK is forecast to be flat this year and rise by

2.7% next year, primarily driven by infrastructure and

private house building.

Infrastructure output is forecast to grow 6.4% this year and

13.1% in 2019 as main civil engineering work commences

on several large projects. In private housing, output is

forecast to rise 5.0%, with demand for new build

underpinned by government support for first home buyers.

This performance contrasts with other sectors of the

construction industry, however. The sharpest decline is

forecast in the commercial sector, where a post-EU

Referendum fall in contract awards for new offices space

since the second half of 2016 is expected to translate into a

fall in activity this year. Office construction is expected to

decline 20.0% in 2018 and 10.0% in 2019.

|