Japan

Wood Products Prices

Dollar Exchange Rates of 25th

April

2018

Japan Yen 109.743

Reports From Japan

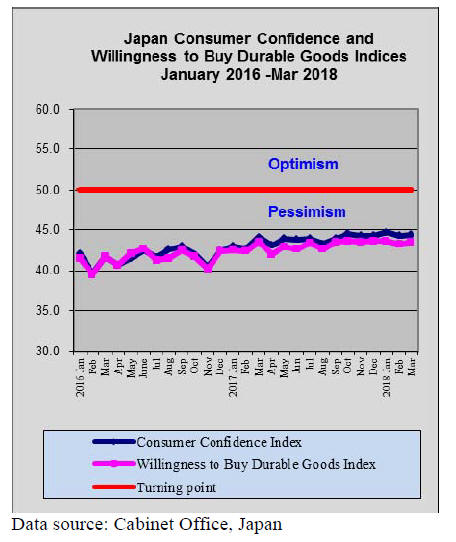

2019 could mark a turning

point on the road to

recovery

The Japanese economy has enjoyed a period of stable

growth buoyed in part by the Bank of Japan¡¯s weak yen

policy and more recently by improvements in global

economic expansion.

But short-term prospects have become precarious. The

government is under attack for a series of scandals

involving officials and public support for the Cabinet has

dipped. This, and the prospect of a hike in the sales tax

next year, is bearing down on both business and consumer

sentiment.

2019 could mark a turning point on the road to recovery

according the International Monetary Fund which is

forecasting slower growth. This, combined with an

anticipated fall in consumer demand because of the sales

tax increase and the suggestion from the BoJ that it could

begin unwinding its easy monetary policy, does not bode

well for the economy.

Angel Gurr¨ªa, OECD Secretary-General, was recently in

Tokyo and during a meeting with the media said Japan

faces important challenges if it is to achieve sustainable

and inclusive growth and labour productivity is one of the

major challenges.

The press release from the OECD says the government

recently launched the New Economic Policy Package,

which aims to double labour productivity growth to 2.0%

per year by 2020. The Package has a number of measures

to boost innovation, including financial support for

investment by SMEs and tax incentives for investment

increases. In addition, Japan is promoting the development

of new industries.

Japan has exceptionally high levels of human capital and a

skilled labour force, which, together with high R&D

intensity, has made it a world leader in technology.

Raising productivity requires better leveraging these

important strengths. Enhancing co-operation between

industry and academia and strengthening Japan¡¯s

integration in international research networks would

increase the return from R&D.

Strengthening Japan¡¯s integration into the global economy

would also boost productivity. Achieving the 2013 goal of

doubling inflows of foreign direct investment by 2020 and

continued measures to enhance openness to trade, building

on the TPP-11, are priorities in this regard.

See: http://www.oecd.org/about/secretary-general/oecd-sg-pressconference-

japan-april-2018.htm

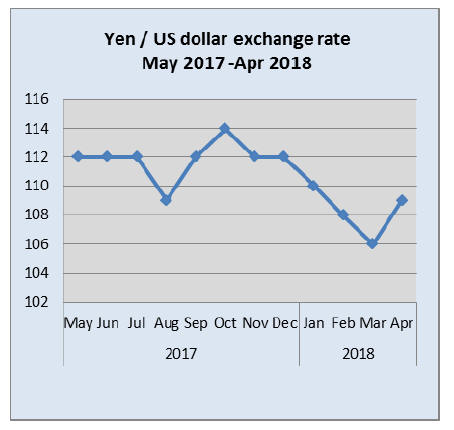

Up-tick in US dollar brings some relief to

Japanese

exporters

The US dollar strengthened for five consecutive days

towards the end of the month driving down the yen

exchange to yen 109 to the dollar.

Japan¡¯s March trade balance continued in surplus but there

was a dip in exports to the US and the EU. The weaker

than forecast growth in exports, despite an improving

global economy, seems to be related to increased

uncertainty driven by fears of a trade war between the US

and China.

The modest weakening of the yen was also attributed in

part to domestic politics. The approval rating of the

Japanese cabinet has slumped as the opposition continues

to attack the ruling party. There have been calls for the

Prime Minister to resign.

Several analysts have commented that it seems odd that

the yen should weaken against the US dollar on rumours

that the Prime Minister may resign since it is he that firmly

supports the weak yen policy of the Bank of Japan (BoJ).

If he resigns there is no certainty that this support for the

BoJ would continue.

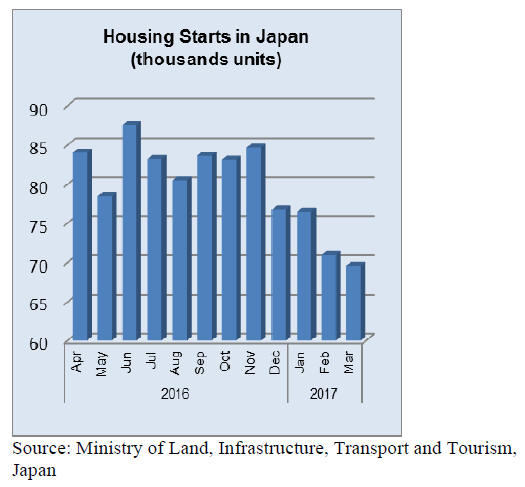

8% drop in March housing starts

Data from Japan's Ministry of Land, Infrastructure,

Transport and Tourism showed housing starts continued to

decline in March. Starts declined over 8% year-on-year in

March, much faster than the 3% year on year decline in

February. At the current pace annualised housing starts

would come in at 895,000 for the year.

Data also showed that construction orders received by big

50 contractors dropped 4% in March after a sharp growth

of 19% in February.

Foreign investment pouring into Japanese real estate

Foreign investors are pouring into Japanese real estate

particularly business premises. Between 2014 and 2017

overseas real estate investment funds have spent around

US$15 billion in Japan and continue to do so believing

that the Bank of Japan will hold down interest rates for the

medium term.

Demand for office accommodation has been boosted by

a

period of economic expansion, the best for more than 15

years which buoyed capital investment especially by the

big corporations.

For as long as the yen is held down against the US dollar

exporters in Japan can expect healthy growth.

For more see: https://www.cbre.com/research-and-reports/apacreal-

estate-market-outlook-2018

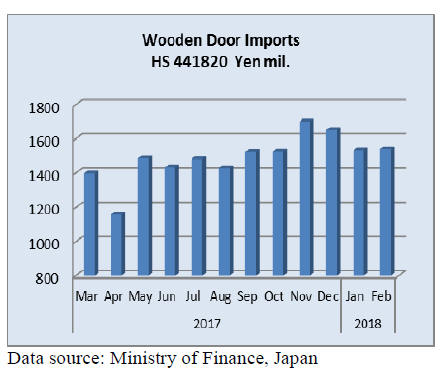

Import round up

Doors

February door imports

February imports of wooden doors (HS441820) continued

to rise compared to a year earlier rocketing up almost 50%

year on year. However, compared to the value of imports

in January there was little change in February.

In February there was a sharp rise in imports from China

which accounted for almost 70% of all wooden door

imports to Japan (58% in January). The combined value of

imports from Philippines and Indonesia plus those from

China amounted to around 90% of all February imports.

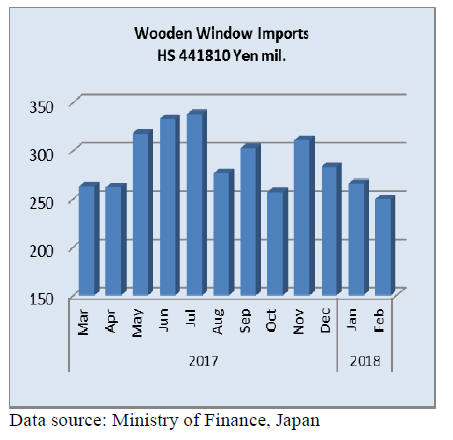

Window imports

February window imports

February marked the third straight decline in the value of

wooden window imports. Year on year February imports

dropped 8% and month on month the value of imports fell

6%.

The top three shippers of wooden windows to Japan

remain China (45%), the Philippines (22%) and the US

(16%) thus accounting for over 80% of all wooden

window imports by Japan.

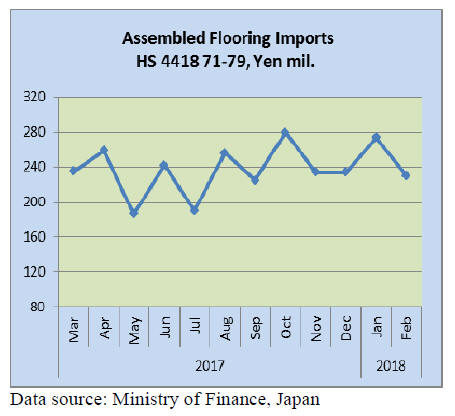

Assembled flooring

January imports

As in previous months wooden flooring imports were

dominated by HS 441875 followed by HS441879.

Together these to categories of assembled flooring account

for almost 90% of all assembled wooden flooring imports.

In order of rank by value, China, Sweden and Thailand

were the main shippers of HS441875 in February while for

HS441879 the main shippers, in order of rank, were

Thailand, China and Indonesia.

Year on year February imports rose over 45% but

compared to the value of imports in January there was a

16% decline in February.

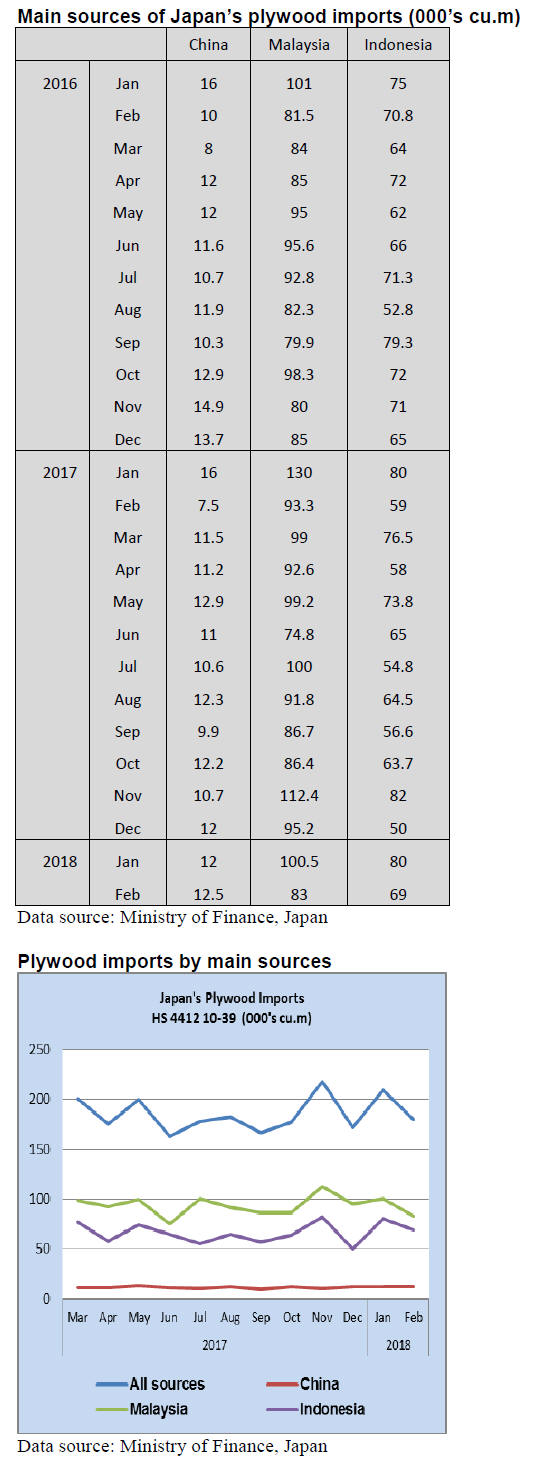

Plywood

February plywood imports

Plywood in HS 441231 accounted for most of Japan¡¯s

imports of plywood and in February accounted for over

85% of all plywood imports. HS441234 accounted for just

8% of February plywood imports and HS441239 less than

1% of imports.

Year on year two of the top three shippers of plywood

(Indonesia and China) increased exports to Japan in

February but shipments from Malaysia were down

compared to a year earlier.

However, month on month, both Malaysia and Indonesia

saw shipments to Japan decline. Shipments from Malaysia

were down 17% while shipments from Indonesia were

down around 14%.

Trade news from the Japan Lumber Reports (JLR)

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

Wood use for public buildings

The Ministry of Agriculture, Forestry and Fisheries and

the Ministry of Land, Infrastructure, Transport and

Tourism announced that percentage of wood used for

public buildings built in 2016 fiscal year. After the 2010¡¯s

law to promote using of wood for lower level public

building, survey is made to see how much wood is used

for lower level public buildings (lower than three stories).

Result of wood use for 97 low level public buildings was

43.3%, 14.4 points lower than 2015. Wooden buildings

were 42, 22 units less than 2015 but by large buildings

with floor space of 1,500 square meters, total floor space

of wooden units doubled compared to 2015. Therefore,

total wood use including interior use increased by 60%.

The Ministries are investigating reasons why buildings are

not wooden.

In 97 public buildings with total floor space of 13,816

square meters, wooden units were 42 with 7,282 square

meters. In remaining 55 units, 35 units are not suitable for

wooden building. Some need to have structure with heavy

load with cranes and some use plenty of water for cleaning

like glass built sun room or storage of precision machines.

Anyway it is necessary to make more campaign to other

government offices to promote of using wood for newly

built buildings. Lack of awareness may be the largest

reason.

South Sea (tropical) logs and lumber imports in 2017

Total import of logs from South Sea countries was

146,806 cbms, 24% less than 2016. During 2017, one of

major South Sea plywood mills quit. Remaining plywood

mills purchase quality logs instead of volume.

By source, 71,202 cbms from Sabah, Malaysia, 29.7%

less. 40,689 cbms from Sarawak, Malaysia, 24.3% less.

6,029 cbms from Solomon Islands, 18.9% less. 28,886

cbms from PNG, 12.6% less.

During 2017, India¡¯s aggressive purchase pushed log

export prices up. In Sarawak, the government raised rate

of timber premium, which also pushed log prices.

In the South Sea countries, harvest restriction of natural

grown timber tightened not only in Malaysia but in other

countries like Myanmar, Laos and Cambodia so hungry

India and Vietnam bought heavily in the Solomon Islands.

In Sarawak, harvest quota is reduced by 20-30% while

quota for local supply expanded from 70% to 80%. With

all these factors, export price of merati regular soared over

US$300 per cbm FOB and even local plywood mills

suffered log shortage.

Log import from Africa in 2017 was 3,787 cbms, 4.1%

more than 2016.

Lumber import was 259,000 cbms, 4% less than 2016.

156,000 cbms from Indonesia and 71,000 cbms from

Malaysia. Both are almost same as 2016. Products are

259,000 cbms of free board, 80,000 ccbms of lumber and

130,000 cbms of processed products.

2017 review of plywood and board

Wooden panel (plywood and board) supply in 2017 was

9,122,748 cbms, 3.7% more than 2016. It is increase of

326,986 cbms. In this, domestic supply was 5,095,378

cbms, 2.8% more and imported panel was 4,027,370 cbms,

4.9% more.

Share of domestic and imports is 55.8:44.2. In volume,

domestic increased 137,320 cbms and the imports

increased 189,666 cbms.

Item of increase is almost all plywood. Domestic increase

of plywood was 146,949 cbms and the imports plywood

was 133,469 cbms.

Domestic softwood plywood production was 3,064,765

cbms, 6.1% more. This is the first time that the production

exceeded three million cbms.

New housing starts in 2017 were 964,641 units, 0.3% less

than 2016. Wood based units were 545,366, almost the

same as 2016. Wood panel supply peaked in 2013 and it

had been declining since then bottomed out in 2015 and

the increase has been for two straight years.

Looking at plywood supply, domestic supply keeps

increasing but the import plywood has been below three

million cbms since 2015.

Domestic plywood manufacturers enjoyed record profit.

Demand for structural panel continues firm then demand

for non-structural panel like floor base and concrete

forming is sharply increasing.

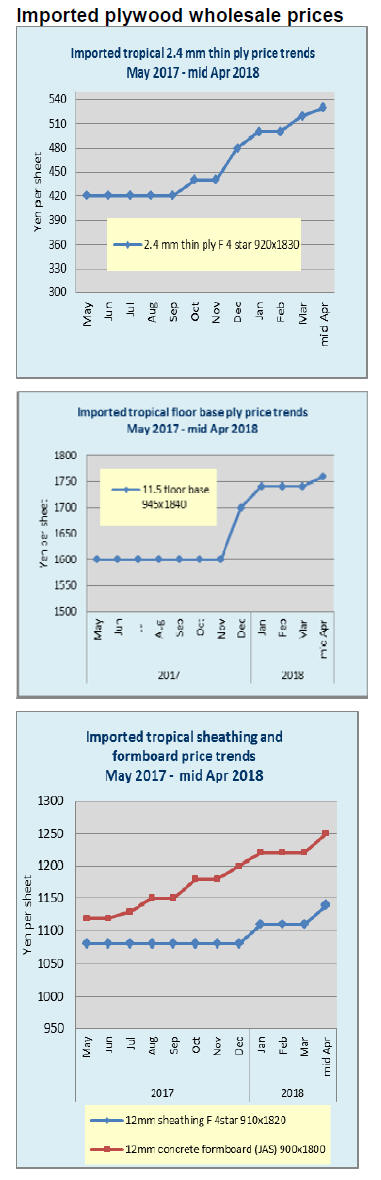

Plywood manufacturers dictate the prices, supported by

brisk demand. Prices of 12 mm 3x6 panel in January 2017

was 980 yen per sheet delivered. 1,000 yen in February.

1,030 yen in September. 1,050 yen in March this year.

Export of domestic plywood in 2017 was 113,846 cbms,

first time to pass 100 M cbms in last five years. The

largest destination is the Philippines.

Supply of South Sea hardwood plywood continues

declining because of log supply shortage in producing

regions by foul weather and various restrictions. Items like

floor base and thin plywood are very tight in supply.

Domestic production of other wooden panels in 2017 was

1,884, 857 cbms, 0.5% less than 2016 while supply of

imported panels was 1,123,251 cbms, 5.3% more.

Major item of the increase is MDF. MDF manufacturers

suffered procurement of material logs and higher prices.

Also high cost of adhesive bond affects manufacturing

cost.

Domestic softwood plywood production has been holding

high level all through 2017.Total production was

3,064,765 cbms, 6.1% more than 2016. This is record high

production and first time to pass three million cbms. Also

the shipment was record high at 3,055,708 cbms, 4.0%

more.

All the plywood plants continued unusually high level

production. With high level consumption, the inventories

have stayed low like only 93 M cbms at the end of

December for monthly shipment of over 250 M cbms so it

was practically hand-to-mouth situation.

The largest change in 2017 was increasing production of

non-structural panels like floor base and concrete forming

panel.

These items relied on South Sea hardwood plywood but

declining supply from Malaysia and Indonesia, domestic

floor manufacturers feel uneasiness for future supply and

have been shifting to domestic softwood plywood.

Production of non-structural plywood in 2017 was

139,172 cbms, 37.2% more than 2016. Plywood plants

have been busy satisfying brisk demand of structural

plywood but considering change of demand structure in

future, they have been producing these items.

Floor manufacturers speeded up shifting to softwood

plywood particularly in the second half of last year after

the prices of South Sea plywood soared. Problem for

softwood plywood plants is procurement of logs and

logistics. Shortage of truck drivers is serious problem so

delivery delays for long distance trucking.

Log procurement is another problem. Mills have made up

log supply network with forest unions and timber owners

but after mills started making non-structural panels, not

only volume but quality becomes important since floor

base needs higher quality logs.

In 2017, sawmills and laminated lumber manufacturers

showed strong demand for logs so competition became

severe for plywood mills.

There will be three more plywood mills starting up this

year so log demand further increases. Also recently started

sawmills have large capacity so log purchase scramble

will get fierce among users.

|