|

Report from

Europe

European wood flooring consumption starting to

recover

After a steep fall of more than 6% in 2014, the European

Federation of the Parquet Industry (FEP) reports that

European wood flooring consumption increased both in

2015 and in the first few months of 2016.

In 2015, FEP observed ˇ°a stabilisation in parquet sales

across Europe, with an upward tendency during the last

monthsˇ±. And in early 2016, FEP report market recovery

across much of Europe.

Preliminary forecasts, which FEP announced during the

Domotex flooring show in Hannover, Germany, suggest

0.5% growth in European wood flooring sales last year.

Final figures will be released at the FEPˇŻs annual General

Assembly in Thun, Switzerland, in June.

Meanwhile a study by Interconnection Consulting is even

more positive about recent trends in the European wood

flooring market. The organisation estimates that wood

flooring sales in the ˇ°top eleven European countriesˇ±

increased 2.2% to 82,7 million m2 in 2015, according to a

press release by Global Flooring Alliance.

The Interconnection Consulting study forecasts continued

growth of 2% per year until 2019. However, prices are not

forecast to rise significantly due to competitive pressure

from Eastern European and Asian manufacturers.

According to FEP, an encouraging sign in EuropeˇŻs wood

flooring market in 2015 was rising momentum in Southern

Europe, notably Spain, for the first time since the

economic crises. There was also good performance in

Sweden, Hungary, the Netherlands, Belgium, Poland and

to a lesser extent, France. The large German, Austrian and

Swiss parquet markets were stable at a high level.

FEP reported further improvements in the first quarter of

2016. Austria, the Baltic States, France, Germany, the

Netherlands and Poland all reported growth rates between

2% and 3% during the period. In Italy and Denmark,

growth ranged between 1% and 2% and the Belgian

market was stable.

However performance in the Nordic countries was

relatively poor. The situation in Finland was described by

FEP as ˇ°the most difficult in Europeˇ±, with an estimated

fall in wood flooring sales of 5-10% in the first quarter.

Sales in Norway were down by around 4%.

A slight improvement in building figures was referenced

as the main reason for the overall improvement in

European wood flooring consumption. The refugee

situation is not believed by FEP to have any impact on

European wood flooring consumption, as less costly

flooring solution would generally be utilised for equipping

emergency housing.

FEP highlighted that the wood flooring sector still faces

stiff competition from other materials. The main source of

competition varies between countries. For example, the

challenge comes particularly from luxury vinyl tiles (LVT)

in Germany and from ceramic tiles in Italy.

According to FEP ˇ°it is becoming increasingly difficult for

consumers to differentiate parquet from competitive

flooring alternatives with a wood look surface.ˇ± Shortage

of raw materials and price increases are mentioned as

additional problems facing the European wood flooring

sector.

Planking and natural look in fashion

With regard to wood flooring types,, FEP note that

wooden planking styles continue to attract customers. A

review of trends at the Domotex show notes that ˇ°floor

boards with grooves, knot holes and irregularities and a

country home look that seems to have just come from the

saw mill are very much the rageˇ°.

The Domotex report identifies oiled instead of sealed

surfaces as another trend.

Interconnection Consulting reports that multilayer parquet

floors now account for 84% of the European wood

flooring market by volume, the majority comprising threelayer

parquet (roughly 70 % of total market volume).

Solid wood flooring accounts for 14% of the market.

Interconnection Consulting also notes ˇ°a trend for real

wooden floors to become customised and exclusive.ˇ±

Declining wood flooring imports from China

While consumption and sales of wood flooring

manufactured in Europe improved in 2015, imports came

under pressure last year. The 5% rise in imports recorded

in 2014, after a lengthy period of weakness, proved to be

short-lived.

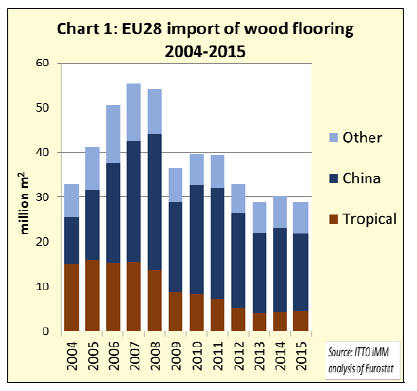

The EU imported 28.82 million m2 of wood flooring last

year, 4.6% less than 2014 and only just exceeding the

recessionary low in 2013. These figures compare to

imports of nearly 40 million m2 in 2010 and a high of

55.40 million m2 in 2007 (Chart 1).

Wood flooring deliveries from China, by far the EUˇŻs

largest single external supplier, fell 7.4% to 17.50 million

m2 in 2015, the lowest level since 2005. While ChinaˇŻs

exports to the UK increased by 2% to 5.19 million m2,

there was a significant decrease in ChinaˇŻs exports to

Belgium (-4% to 2.90 million m2), Netherlands (-8% to

2.07 million m2), Italy (-21% to 1.96 million m2),

Germany (-10% to 1.75 million m2), and France (-47% to

0.44 million m2).

Overall the signs are that Chinese flooring became less

competitive in the EU market in 2015. This is probably

due to a combination of factors notably the weakness of

the euro and concerted efforts by domestic and other

overseas manufacturers in South East Asia and Brazil to

regain share of the European market.

Tightening enforcement of the EU Timber Regulation,

combined with publicity surrounding the Lumber

Liquidators prosecution under the U.S. Lacey Act in

relation to wood flooring from China may also have

discouraged sourcing of Chinese product in 2015.

EU wood flooring imports from tropical countries rise

3%

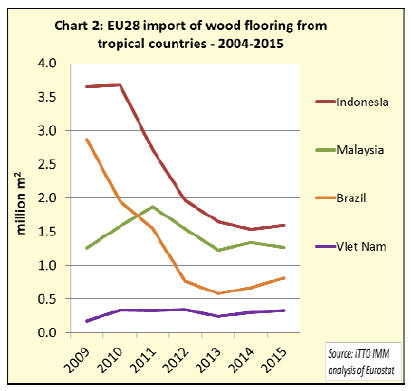

In contrast to EU imports from China, imports from

tropical countries increased 3% to 4.46 million m2 in

2015. Indonesia remains the single largest tropical supplier

of wood flooring to the EU. Although still low by

historical standards, EU imports from Indonesia increased

4% to 1.59 million m2 in 2015.

There was also a partial rebound in imports from Brazil

(+21% to 0.81 million m2) and continued slow growth in

imports from Vietnam (+9% to 0.33 million m2). However

imports from Malaysia declined 5% to 1.27 million m2

(Chart 2).

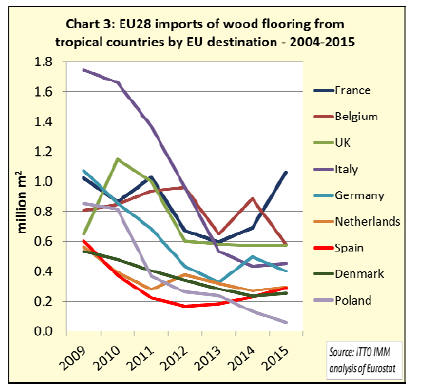

A notable trend in 2015 was a significant switch in

flooring imports by France away from China in favour of

Brazil and Indonesia. However FranceˇŻs increased imports

from tropical countries was mirrored by a decline in

imports into Belgium suggesting it might be partly due to

changing distribution networks in continental Europe

(Chart 3).

UK imports of wood flooring from tropical countries were

flat during 2015, a rise from Indonesia and Malaysia being

offset by a decline from Hong Kong and Vietnam. This

may be explained by the more advanced state of legality

verification systems in the former two countries as EUTR

enforcement has been tightening in the UK.

Imports of wood flooring from tropical countries into

Italy, formerly the largest EU market for this commodity,

remained flat at a low level in 2015. Imports into Germany

declined in 2015 after a brief recovery in 2015. German

imports from Vietnam were particularly weak last year.

However Sweden and Italy imported more from Vietnam

in 2015.

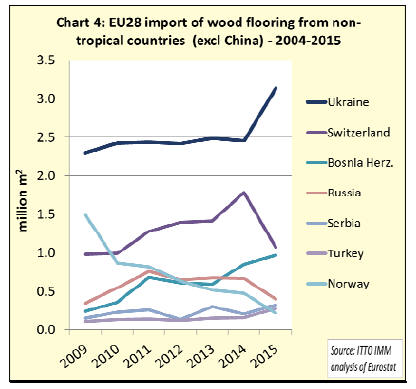

There was strong variation in EU imports from nontropical

countries in 2015 (Chart 4). Imports from

Switzerland plummeted 40% to 1.1 million m2, probably

due to the strong Swiss franc and related price increases

for Swiss flooring in the Eurozone. Imports from Norway

also dropped by 54% and those from Russia fell by 41%.

However EU wood flooring imports from Ukraine

increased 28% to 3.1 million m2 which may be partly due

to a new law that entered into force in Ukraine in

November 2015 which added oak to the list of ˇ°rare and

valuableˇ± timber species for which controls are imposed

on a wider range of secondary and tertiary processed

products.

This may have encouraged importers to purchase

additional supplies of oak flooring before November 2015

to beat the extra controls now in place.

EU wood flooring imports from Bosnia-Herzegovina also

increased sharply in 2015, by 13.5% to 1 million m2.

Bosnia is attracting more investment in wood processing

industries attracted by the countries close proximity to the

EU market, relatively low labour costs for the European

region, and proximity to forest resources which cover 55%

of the countryˇŻs land area.

Laminates dominate European flooring market

While the market for real wood flooring recovered some

lost ground in 2015, data published by the European

Producers of Laminate Flooring (EPLF) association

highlight the scale of the challenge from laminate flooring.

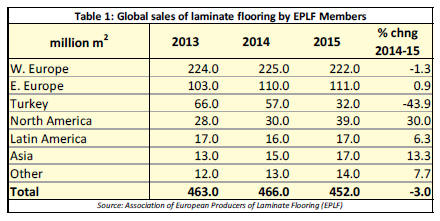

Members of the EPLF association sold 452 million m2 of

laminate flooring last year, around 333 million m2 of

which was in Europe, over four times the volume of real

wood flooring consumption in the region.

Overall world-wide sales of EPLF members declined 3%

in 2015. However the decline was almost all in Turkey due

to one Turkish company leaving EPLF and anti-dumping

proceedings by the Turkish Ministry of Economy against

several German flooring manufacturers which ran until the

summer of 2015 (Table 1).

A slight decline in laminate flooring sales in Western

Europe was offset by a rise in Eastern Europe in 2015.

European flooring manufacturers were also increasing

sales in North and South America and Asia last year. This

is due both to the weak euro and an export market

development strategy centred on higher-end quality

products and adherence to European technical and

environmental standards.

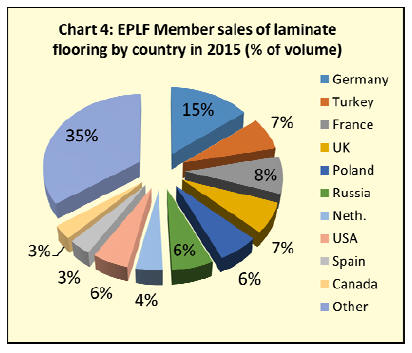

The single biggest market for laminate flooring sold by

EPLF members is Germany, which alone accounted for 66

million m2 in 2015, a fall of 4.3% compared to 2014

(Chart 4). Like solid wood flooring, laminate flooring is

also under pressure in Germany from substitute products,

especially LVL.

Laminate flooring sales in France, the second largest

market, declined 5.1% to 37 million sq.m in 2015.

The positive trend in the UK recorded in 2014 also ended

last year, with sales falling 3.1% to 31 million sq.m

despite continuing growth in the construction market.

In contrast, recovery in the Netherlands and Spain is

reflected in laminate flooring sales figures. Sales in the

Netherlands increased 11.8% to 19 million sq.m and sales

in Spain were up 4.8% at 15.3 million sq.m.

EPLF member sales in Russia, the largest Eastern

European market for laminate flooring, increased 2% to 29

million m2 in 2015, despite economic difficulties. Sales in

Poland increased 7% to 28 million sq.m and Bulgarian

sales jumped 25% to 5 million sq.m during the year.

Romania and Hungary were stable compared to 2014,

accounting for sales of 11 million sq.m and 6 million sq.m

respectively in 2015. However sales to Ukraine fell 38%

to 5 million sq.m last year.

Germany accused of restricting trade in construction

products

According to EPLF, the German Institute for Building

Technology (DIBt) is considering introduction of special

rules for building products that go well beyond the CE

mark requirements for compliance with the European

Construction Products Regulation and which would

effectively ˇ°seal off the German construction products

market from the EU single marketˇ±.

According to the EPLF, the approach now being

considered may be in breach of a decision taken by the

European Court of Justice in October 2014. This

concluded that GermanyˇŻs national requirements for

building products created unnecessary barriers to free

trade in the European free market and must be phased out.

At the time of the CourtˇŻs decision ˇ°the only building

products that could be used in Germany were those

bearing an Ü mark complying with the DIBtˇŻs own

specifications, which were independent from European

harmonisationˇ±, according to EPLF.

Following the decision, DIBt has adopted a new approach

to quality control which would evaluate whole buildings

rather than individual construction products. A draft

document to this effect was circulated among affected

institutions and associations at the end of 2015 and

comments were invited until 25 February 2016.

According to EPLF, which is very critical of this

approach, the draft contains exhaustive requirements

regarding components, emissions, and measurement

procedures. These requirements include a mix of DIBtˇŻs

own stipulations for substances and the EUˇŻs minimum

emission requirements.

The draft has led to protests from industry both in Berlin

and in Brussels. EPLF quotes lawyer Michael

Halstenberg: ˇ°in my view, the draft is once again

incompatible with European law. The DIBt doesnˇŻt

understand that setting building product requirements

through an indirect road (through redefining them as

ˇ°building requirementsˇ±) isnˇŻt permitted eitherˇ±.

EPLF believes that small and medium-sized companies

would particularly struggle to tender for public

construction projects in Germany in the future.

ˇˇ

However, the association concedes that other EU

countries, such as France, Belgium, and Sweden, among

others, have adopted a similar approach.

The draft has also been criticised by the German

Multilayer Modular Flooring Association (MMFA) and

the Association of the German Wood-based Panel Industry

(VHI). The full EPLF press release can be found at:

http://bit.ly/26wnH5k .

German timber companies launch campaign against

FSC

A group of 25 German forestry and timber companies

headed by Eurobinia have published a letter calling for

abolition of FSC certification in public forests and asking

that FSC be dropped as a requirement in German public

procurement policy.

According to a report by the Global Timber Forum (GTF),

the letter was sent through a lawyer and addressed to

ˇ°responsible politiciansˇ±. A press release was also

distributed to timber industry media.

According to the GTF, FSC Germany responded that the

criticism was too far-fetched for the organisation to

comment officially. The website also quotes German

public procurement and certification specialist Ulrich Bick

from Th¨ąnen-Institute as saying that he saw no reason to

change public procurement requirements ¨C which

currently require that timber be either FSC or PEFC

certified.

Ulrich Bick also suggested there is a broad consensus

between German ministries to maintain the current system.

The full article and a related forum discussion can be found at

http://bit.ly/1Uc5mFM and http://bit.ly/21ccmDC.

|