Japan Wood Products

Prices

Dollar Exchange Rates of

25th September 2014

Japan Yen 109.29

Reports From Japan

ˇˇ

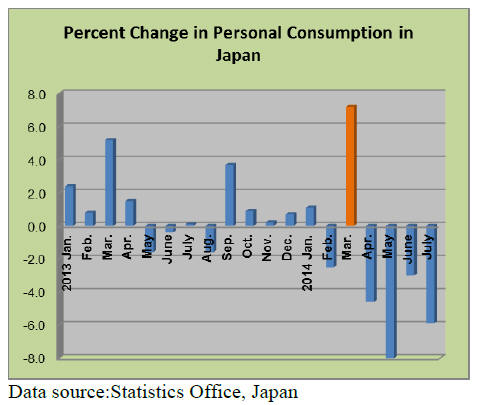

Personal consumption key to growth

Japan's annualised growth in the first quarter of this year

was almost 6% as companies and consumers brought

forward spending to beat the 60% rise in the consumption

tax (from 5% to 8%) 1 April 2014.

As expected, personal spending fell back sharply in the

second quarter and the Bank of Japan has warned that it is

taking longer than forecast for spending to recover.

Personal spending accounts for over 60% of GDP growth

in Japan and the rapid fall in household spending, coupled

with the yen's depreciation, has slowed recovery from the

„tax shock‟.

The average monthly household expenditure for July was

yen 280,293 down 5.9% in real terms from the previous

year.

Will 2015 consumption tax increase to 10% derail

growth?

The Japan Center for Economic Research (JCER) in its

short-term forecast for the Japanese economy forecasts

that economic expansion would resume in the July¨C

September quarter as the effects of the consumption tax

increase subside and they forecast an upswing in capital

investment at the beginning of next year.

See:

http://www.jcer.or.jp/eng/pdf/sa158-eng2.pdf

JCER notes that the last-minute consumer spending,

especially on durable goods, in the first quarter increased

more than recorded in the same period prior to the

previous consumption tax increase in 1997.

In 2015 the consumption tax is due to be raised to 10%

from the current 8% and while there will be once again a

degree of last-minute spending by consumers, this is not

expected to greatly affect overall growth for 2015 such

that the Japanese economy is expected to expand in real

terms by 1.1% in fiscal 2015.

There are risks however and JCER point to a possible drag

on growth brought on by a 2015 consumption tax hike; a

downswing in net exports as the electronics and other

industries continue to hollow out; effects on markets in

emerging economies from tapering of QE3 measures in

the United States; fragility of the Chinese financial

market; geopolitical instability, such as the situation in

Ukraine and foreign exchange market fluctuations.

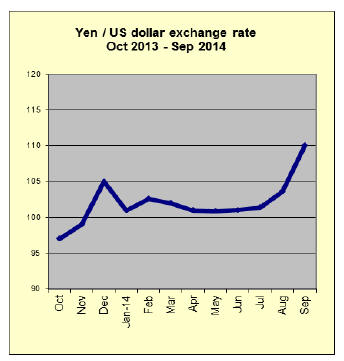

Yen at six year low

The yen fell to a six-year low against the US dollar during

the second half of September. Behind the yen weakness

was the improving US economy and signals from the US

Federal Reserve that it could raise borrowing costs faster

than expected.

While the Federal Reserve has said it would keep interest

rates near zero for a "considerable time" investors are

moving money out of yen into dollars in anticipation of an

interest rate hike. Such a move makes dollar-denominated

assets more attractive since both Japan and the EU rates

are likely to remain low for some time.

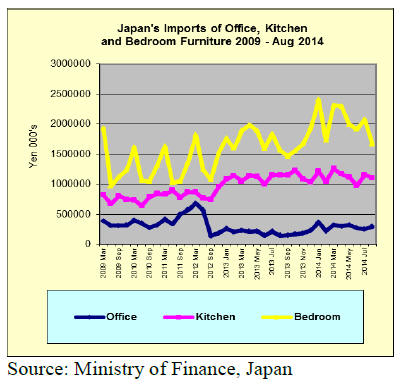

Trends in office, kitchen and bedroom furniture

imports

Japan‟s office, kitchen and bedroom furniture imports

from 2009 to the end of August 2014 are shown below.

Japan‟s imports of bedroom furniture fell sharply in

August. If it were not for the modest increase in July then

the trend would have been down for four consecutive

months. Demand for imported kitchen furniture remains

flat largely a reflection of the slow housing market.

Imports of office furniture have settled back into the

steady levels seen before the minor peak just before the

consumption tax increase in April this year.

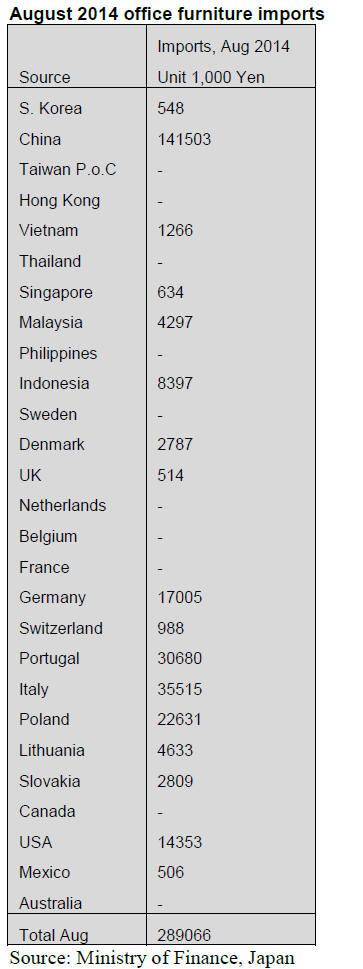

Office furniture imports (HS 9403.30)

Japan‟s August 2014 imports of office furniture were up

15% compared to levels in August. China remains the

major supplier (49%) but its market share fell slightly in

August. Exports of office furniture by both Italy and

Portugal increased and there was a big jump in imports

from the US in August.

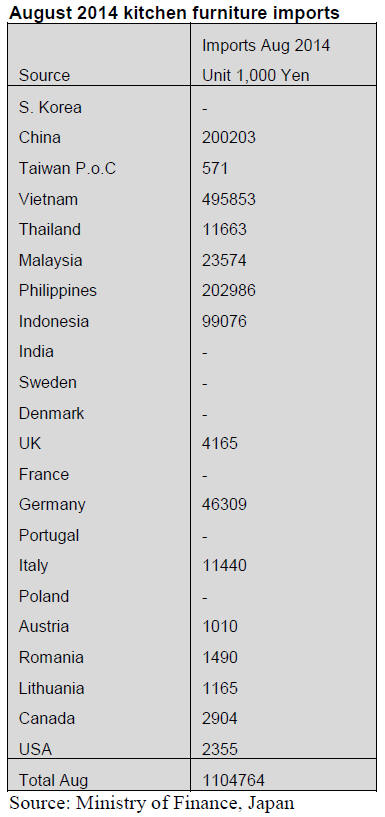

Kitchen furniture imports (HS 9403.40)

The top suppliers of kitchen furniture to Japan in August

continued to be Vietnam (45%, an increase over July

levels), China and the Philippines, each of which

accounted for between 17-18% of all August imports of

kitchen furniture.

Year on year, August 2014 imports of kitchen furniture

were barely changed from levels in August 2013.

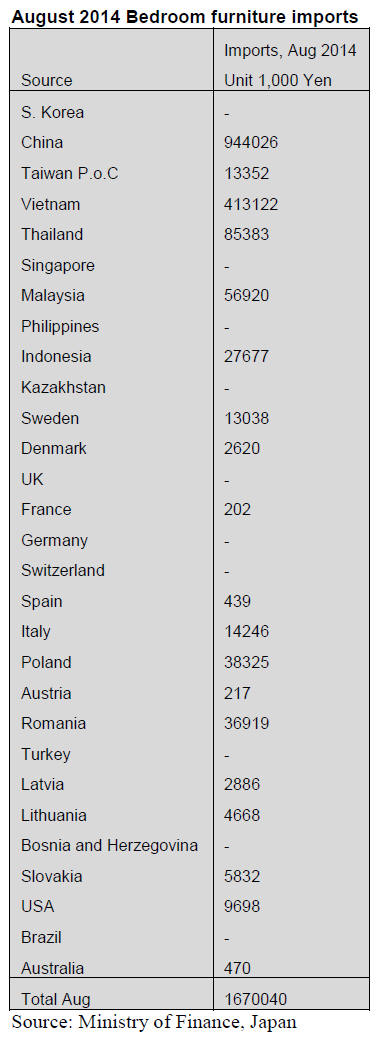

Bedroom furniture imports (HS 9403.50)

China, Vietnam and Thailand dominated bedroom

furniture imports in August as they have since early in the

year but each suffered a decline as Japan‟s overall imports

of bedroom furniture fell by 9% in August.

Other major suppliers include Malaysia, Poland and

Romania but all saw a correction in levels of demand in

August. As the holiday season in Japan is over house

builders are back at work so hopefully completions will

increase which should lift demand for furniture.

Trade news from the Japan Lumber Reports (JLR)

For the JLR report please see:

http://www.nmokuzai.

com/modules/general/index.php?id=7

South Sea (tropical) logs

Log market in supplying regions continues firm. In

Sarawak and Sabah, Malaysia, heavy rain started in

middle of August, which could be a start of rainy season.

In Sarawak, where log supply relies on rivers, barges are

not able to navigate rivers so that logs stay upstream.

Log supply has been tight even before the rain started so

Sarawak log prices are unchanged at US$280-295 per cbm

C&F on meranti regular for Japan. Low grade meranti for

India is US$260-270.

Since Sarawak log supply has been tight, more buyers are

active in Sabah to supplement Sarawak supply. Sabah is

also suffering foul weather and log supply is down. Log

buyers try to procure enough logs before rainy season

starts in September but rain started much sooner so many

ships are waiting for logs at loading ports.

Sabah‟s yellow serayah regular prices are slightly up at

US$260-265 per cbm FOB. After Myanmar stopped log

export, India has been everywhere to look for

substitutions.

India‟s main use is keruing for plywood. There is not

enough keruing in Sarawak so India has been buying

meranti and melapi. India is also buying in PNG and

okoume in Africa.

Log production has been dropping in PNG and Solomon

Islands after rain started since July. Log market in Japan

is holding weakly. Sarawak meranti regular log prices are

yen 10,700 per koku CIF, unchanged from August.

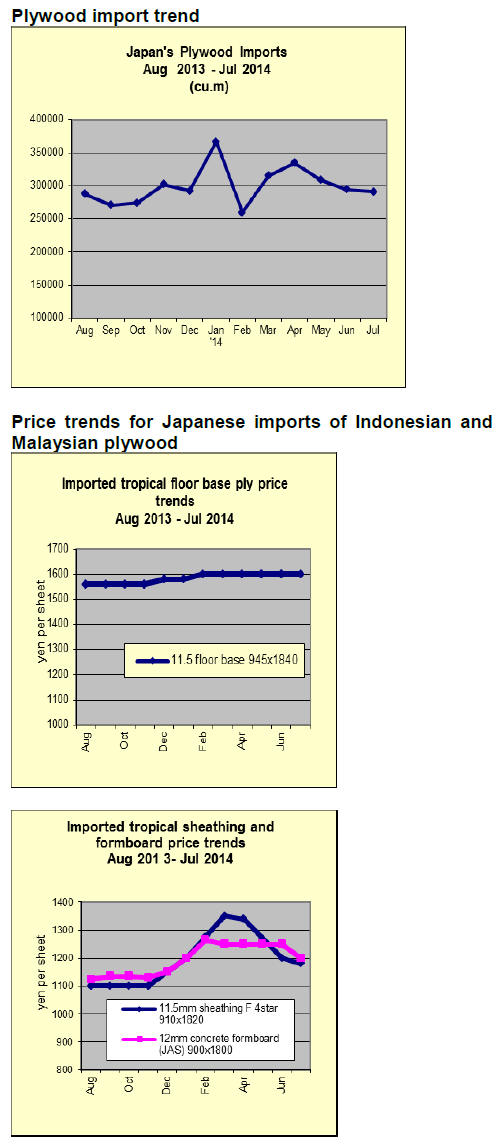

Production curtailment of plywood

The market of softwood plywood has been weakly holding

after the demand bottomed in May and June then

recovered some in July and August. The shipment in July

increased to about 200,000 cbms.

The domestic manufacturers reduced the production by

about 15% in July and August to hold the market and

expressed the plan to continue 15% production curtailment

in September.

However, actual July production was 213,300 cbms, only

7.9% less than June production but the production in

August is estimated down to 190,000 cbms because of

summer vacation with the shipment of about 190-200 M

cbms so that the inventories should be staying unchanged

at about 220-230,000 cbms.

Abnormal heavy rain in the Western Japan in August

slowed down construction activities. After things get back

to normal, deliveries of plywood are affected by shortage

of trucks.

Import of European lumber for the first half of 2014

Import of European lumber for the first half of this year

was 1,416,000 cbms, 11.0% less than the same period of

last year but it is the second highest in last five years.

Because of this high level import, the market started

slowing down and future purchases of lamina and stud are

largely reduced. In the first half of last year, demand was

expected to increase before the consumption tax increase

in April so that monthly import has continued about

250,000cbms.

Also high Euro based export prices encouraged the

European suppliers then the demand of European lumber

and laminated lumber started lagging in Japan since spring

with housing starts dropping. The arrivals finally dropped

down to about 200,000 cbms in June and further import

curtailment seems to continue through the year.

Export of domestic wood products

Export of wood products from Japan has been increasing

consistently and the amount of the export for the first half

of this year was yen 8.164 billion, 51.1% more than the

same period of last year. This is much faster pace

compared to the increase by 30% of last year.

By item, log export was yen 3.165 billion, 173.8% more

than the same period of last year, exceeded total amount of

last year in six months. Weaker yen made the Japanese

logs much competitive so the log export to China, Korea

and Taiwan has been climbing rapidly. Meantime, export

of other products like lumber and plywood has also been

increasing by 13.9% and 23.4% respectively.

The government plans to increase the export of forest

products from yen 12.3 billion in 2012 to yen 25 billion in

2020 and the Forestry Agency allocated sixty million yen

budget for performance experiments in China by Chinese

standard, promotion to use the Japanese products in China,

holding seminars and exhibition and making guidance

manuals.

Logs for China are mainly C grade logs for crating lumber

and engineering works. In Japan, thinning used to be

abandoned in the woods but now they are encouraged to

haul out so that the supply of C grade logs has been

increasing.

Domestic logs and lumber

In Western Japan, heavy rain and typhoons hampered log

production and the log market is in confusion.

Sawmills in the area reduced log purchase in rainy season

of June and July in fear of beetle damage so their log

inventories are not enough. Consequently, in Kyushu,

cedar log prices are soaring and in Shikoku and Kansai

region, log production has been disrupted rather

extensively.

In Northern Japan and Hokkaido, unstable weather

reduced log supply. This is time for sawmills to buy and

build up log inventory so the log prices are firming

generally. However, lumber movement is not so active and

stagnating so sawmills are not able to go after high priced

logs.

Nationwide average log prices are 12,300 yen on 3 meter

post cutting cedar, 400 yen up from August, 10,300 yen on

4 meter purlin cutting cedar, 400 yen up, 16,800 yen on 3

meter post cutting cypress, 400 yen up, 27,400 yen on 6

meter post cutting cypress, 300 yen down.

Lumber market is one step weaker after the summer

vacation season. Orders from precutting plants are not as

much as expected. Despite climbing log prices in Western

Japan, buyers are in no hurry to buy lumber. Present

market is soft and further deterioration is possible if the

demand continues sluggish. Meantime, some marketers

see that considering tight log supply and possible rise of

fall demand, the market prices should hold up.

|