By Madison's Lumber Reporter

An unfortunate truth of life, economics, and physics is that not all things can go up at the same time. Once up, they don’t always stay there. This is a week of mixed news: U.S. home building activity continues to improve, but in Canada forest operators are facing work-stoppage with one of the two railways.

In regards to this CN Rail strike: usually these last just a few days. However, at this time the House of Commons does not sit again until Dec. 2 so there is no possibility of back-to-work legislation until then. In any case, it is a fact that forest products are among the last to resume service once the railway starts operating again.

As for the good news, U.S. home building for October jumped +3.8% the Commerce Department said Tuesday, reaching a seasonally adjusted annual rate of 1.31 million units. Starts for single-family houses were up +2%, largely due to construction in the West and South. Construction of apartment buildings rose +6.8% in October from the prior month.

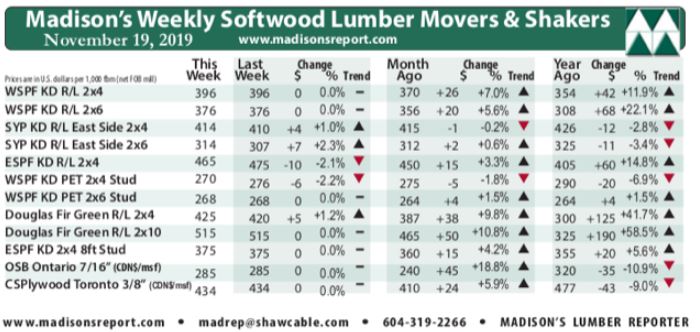

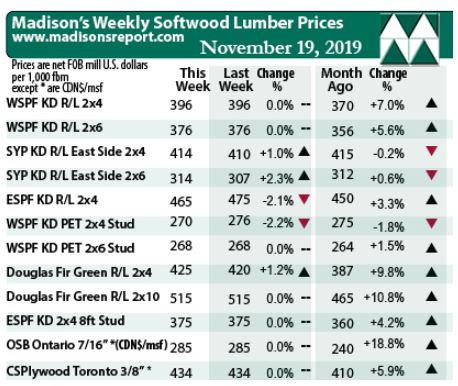

Once again flat over the previous week, the price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr remained last week at US$396 mfbm (net FOB sawmill; cash price, or “print”). Last week’s price is +$26, or +7%, more than it was one month ago. Compared to one year ago, when prices were sliding down terribly, this price is up +$42 or +12%.

An unfortunate truth of life, economics, and physics is that not all things can go up at the same time. Once up, they don’t always stay there. This is a week of mixed news: U.S. home building activity continues to improve, but in Canada forest operators are facing work-stoppage with one of the two railways.

In regards to this CN Rail strike: usually these last just a few days. However, at this time the House of Commons does not sit again until Dec. 2 so there is no possibility of back-to-work legislation until then. In any case, it is a fact that forest products are among the last to resume service once the railway starts operating again.

As for the good news, U.S. home building for October jumped +3.8% the Commerce Department said Tuesday, reaching a seasonally adjusted annual rate of 1.31 million units. Starts for single-family houses were up +2%, largely due to construction in the West and South. Construction of apartment buildings rose +6.8% in October from the prior month.

Once again flat over the previous week, the price of benchmark lumber commodity Western Spruce-Pine-Fir KD 2×4 #2&Btr remained last week at US$396 mfbm (net FOB sawmill; cash price, or “print”). Last week’s price is +$26, or +7%, more than it was one month ago. Compared to one year ago, when prices were sliding down terribly, this price is up +$42 or +12%.