|

Report from

Europe

Slowing pace of EU tropical timber imports

Latest trade data shows that the rising trend in the value of

EU imports of tropical wood products that began in the

second half of 2014 levelled off in 2016.

The stability in the euro value of tropical wood imports in

the second half of 2016 may hide a slight fall in the

volume of imports as European currencies weakened on

foreign exchange markets during that period (which

implies a rise in import prices).

The euro, trading at around US$1.15 in June 2016, had

fallen to only US$1.05 by the end of the year. Even more

pronounced is the fall in the British pound, which was

trading at US$1.50 in June just before the country’s vote

to leave the EU before declining to a 30-year low of

US$1.29 in early July after the result and which now

stands at just US$1.23.

Nevertheless, the dramatic slowdown in European tropical

wood imports forecast for the second half of 2016 in

response to currency movements and economic

uncertainty in the UK following the Brexit vote failed to

materialise. Prospects for the market in 2017 also look

reasonably positive.

While the political situation in Europe is still uncertain,

the economic recovery is gathering pace, helped by an

improving global outlook, low interest rates, a significant

fall in the level of unemployment, a weak euro and the end

of austerity.

Charts 1 to 3 below show the monthly trend in imports of

tropical wood products into the EU up to the end of

October 2016 using 12 month rolling totals.

This is calculated for each month as the total import of the

previous 12 months. The data removes short-term

fluctuations due to seasonal changes in supply and

shipping schedules and provides a clear indication of the

underlying trade trend.

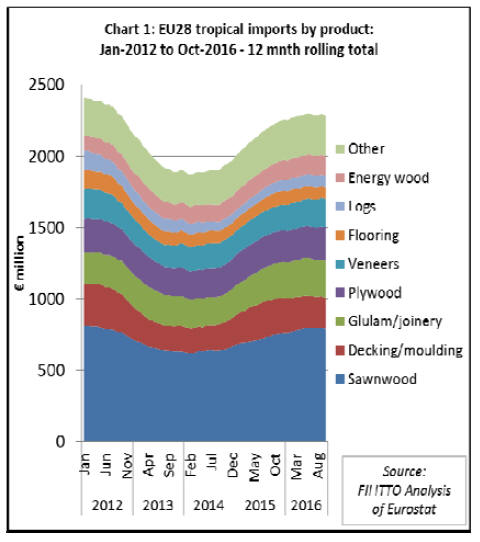

Chart 1 shows total EU euro import value of all wood

products listed in Chapter 44 of the HS codes sourced

from tropical countries. Total imports in the 12 months to

October 2016 were euro 2.29 billion, slightly above euro

2.26 billion recorded for the 12 months of 2015.

European imports of tropical veneer, plywood, and energy

wood continued to rise slowly between January and

October 2016. European imports of tropical sawnwood,

LVL and logs, which were rising in the first half of 2016,

stabilised at the higher level in the second half of the year.

However, imports of tropical decking and mouldings,

which increased sharply in 2015, were sliding throughout

2016.

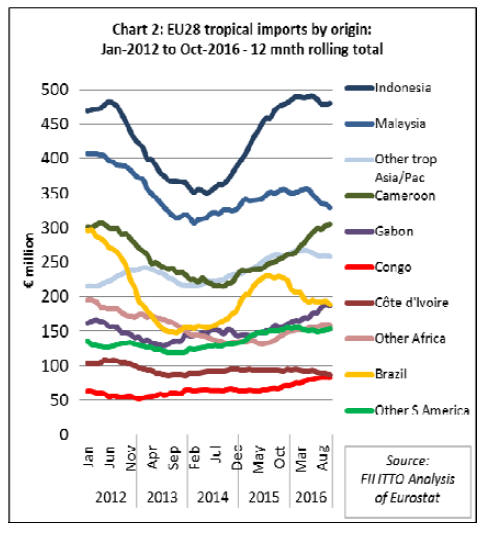

Chart 2 shows how European imports from the major

tropical supply countries developed between 2012 and

October 2016.

After rapid growth in 2015 and the first quarter of 2016,

European imports from Indonesia (dominated by decking,

doors, plywood and LVL) stabilised at the higher level

between April and October 2016.

Imports from Malaysia (mainly sawnwood, plywood,

doors, and LVL) peaked in May 2016 and fell in the

months to October. Imports from Brazil (mainly

sawnwood and decking) were also sliding in 2017.

However, imports from Cameroon (almost all sawnwood)

and Gabon (a mix of sawnwood, veneer and plywood)

continued to rise in the year to October.

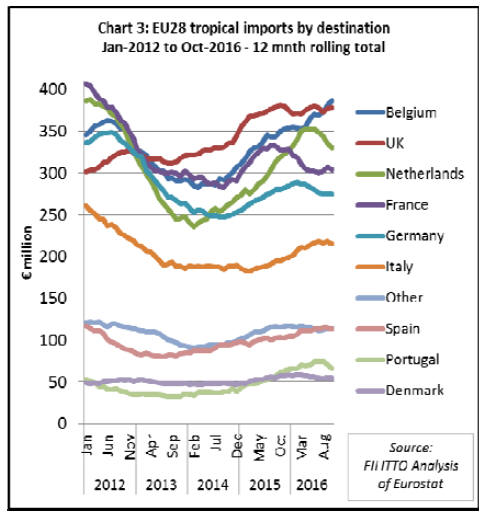

Chart 3 shows the recent trend in tropical wood imports

into the main EU consuming countries. The pace of

growth in imports into the UK (which takes mainly doors,

plywood and sawnwood) was slowing in the early months

of 2016.

Contrary to expectations of a sharp downturn, the euro

value of UK imports stabilised at the higher level in the

months following the Brexit vote in June.

The value of tropical wood imports into Belgium (mainly

sawnwood and decking) increased so rapidly in the year to

October that the country was on course to overtake the UK

as the largest European destination for tropical wood in

2016.

This suggests that the trend towards concentration of

Europe’s tropical imports in the hands of a few large

traders close to main ports continues to intensify - a trend

driven partly by logistics and partly by the risk

management demands of the EU Timber Regulation.

However, the rise in import value into Belgium between

April and October 2016 was mirrored by a sharp decline in

imports into Netherlands during the same period, so these

trends may simply reflect temporary shifts in internal EU

distribution channels between the ports of Rotterdam and

Antwerp.

Meanwhile, direct imports of tropical wood into France

(mainly sawnwood, decking and veneer) and Germany

(mainly decking and sawnwood) were sliding in the

opening months of 2016 but stabilised between July and

October.

The recovery in tropical wood imports by Italy (mainly

sawnwood and veneer), Spain (mainly sawnwood and

veneer) and Portugal (mainly sawnwood, logs and chips)

in the first half of 2016 lost some momentum in the second

half of the year.

Improving economic prospects in Europe

While there are significant downside risks in 2017,

particularly with key national elections due to be held in

Germany, France and the Netherlands, prospects for the

European market seem promising.

Economic surveys show that manufacturing activity and

economic sentiment in the EU increased to their highest

levels since 2011 in the closing months of last year.

By the end of 2016, unemployment in the 19-nation euro

zone had fallen to its lowest point in more than seven

years: 9.8% according to Eurostat compared to over 20% a

year earlier.

The big question in Europe this year is whether fragile

economic growth and unprecedented central-bank stimulus

will be overtaken by populist politics which could threaten

the future of both the euro and the European single market.

But while Europe’s political calendar in 2017 certainly

creates uncertainty, it might also offer opportunities.

In a recent interview for CNBC, Francesco Garzarelli, cohead

of global macro and markets research at Goldman

Sachs noted that a potential right-wing president in France

could lead to a stronger reform agenda in Europe. "If

France were to change gear and become more inclined to

move forward into reforming its economy I think that will

force the likes of Italy, Portugal, Greece to do the same,"

Garzarelli said.

In fact, more economic analysts now seem inclined to give

Europe the benefit of the doubt and are suggesting that

growth will exceed expectations. According to a research

team led by Anais Boussie, writing in the Credit Suisse

European Economics note on 9 January, "The euro area is

set to deliver an upside growth surprise this year. Market

expectations for growth are too low, in our view. Growth

should strengthen on the back of stronger global trade and

a pick-up in construction activity. It should remain

supported by consumer spending, for which the

fundamentals are improving,"

The Credit Suisse team forecast that GDP in the euro-zone

will rise by a sturdy 2.0% in 2017, growth that will be

underpinned by consumer spending. Instead of being

fuelled by things like low oil prices, Credit Suisse reckon

consumer spending will grow thanks to improving

fundamentals like labour demand.

They also note that "construction investment has

contributed positively to growth for the past six quarters,

and appears to be accelerating”.

Credit Suisse are confident that "the risk of deflation in the

euro area has largely disappeared and headline inflation is

set to rise sharply in the first half of 2017 as the strong

dampening effect from past oil price declines fades away."

They also expect that the European Central Bank will be

“dull” (a positive trait after a few too many “interesting”

years) – quantitative easing will continue to provide

greater liquidity at least until the end of the year while the

base interest rate is likely to remain unchanged.

UK economy defies expectations in 2016 but likely to

slow in 2017

Outside the euro-zone (but still a member of the EU for at

least another 2 years), the UK economy defied

expectations in 2016 as Britons decided to keep calm and

carry on spending following the Brexit vote. Growth

showed surprising resilience in the face of fears of

recession with warnings from the Bank of England ahead

of the EU referendum proving unfounded.

Indeed, the UK Office for National Statistics said the

economy grew by 0.5 per cent between July and

September 2016, the three month period after the

referendum.

The UK economy remained buoyant in the last quarter of

the year. The Markit/CIPS UK Manufacturers Purchasing

Managers Index for December rose to 56.1, the strongest

reading since June 2014, and up from 53.6 in November.

A reading above 50 indicates expansion in the sector, with

the month's figure driven up by orders from home and

abroad. The figures put the UK on course to be the fastest

growing economy in the G7 group of leading nations in

2016.

However, this resilience is not expected to last. The British

pound’s plunge in value last year may see growth falter in

2017. Surging prices due to the weaker currency are

widely forecast to bring an end to the consumer spending

spree that has helped prop-up growth since the EU

referendum.

The UK’s Office for Budget Responsibility (OBR)

estimates the economy will take a hit of almost �60 billion

over the coming five years as a result of the Brexit vote.

The OBR has slashed UK growth forecasts and is

predicting higher borrowing than previously expected.

To boost short term growth, the UK government is pinning

its hopes on a big increase in public spending on

infrastructure in a package of measures unveiled in August

last year worth more than �170 billion and on historically

low interest base rate of only 0.25%.

|