|

Report from

Europe

Furniture production growing primarily in Asia

World production of furniture has grown constantly over

the last five years. The CSIL Word Furniture Outlook

currently estimates its worth at about US$480 billion, up

from US$437 billion in 2013. Production in Europe and

North America stagnated between 2009 and 2014.

High-income countries accounted for 39% of production

in 2014 and middle and low-income countries for 61%.

The share of middle and low-income countries in world

production first exceeded 50% in 2010 and has risen

steadily since.

A closer look at the different regions reveals variations

among the low and middle-income countries. CSIL

observed that production in South America, the Middle

East and Africa was static between 2009 and 2014. The

only region to show growth in the reporting period was

Asia and Pacific. Production there almost doubled over the

last five years.

According to CSIL, the world‟s five largest furniture

producing countries in 2014 were China, the USA,

Germany, Italy, and India. Production in China more than

doubled between 2009 and 2014. Over half of world

furniture production was in China last year. Meanwhile,

production in the US and India is increasing slowly while

production is stagnant in Germany and gradually declining

in Italy.

World furniture trade has also grown steadily since the

low of US$94 billion in 2009 during the financial crises.

CSIL estimates that the trade volume reached US$134

billion in 2014, an 8% increase compared to US$124

billion in 2013.

CSIL expects further growth to US$141 billion in 2015.

This estimate is based on assumed world GDP growth of

3.5% in 2015, with forecast growth of 2.4% in advanced

economies and 4.3% in emerging and developing

economies.

Only half of world furniture trade takes place between

countries in geographically distant regions, according to a

study published by the EU Commission at the end of 2014.

The most important of these flows are from the middle and

low-income countries of Asia to the United States and

Europe. In the European Union plus Norway, Switzerland

and Iceland about 75% of foreign furniture trade takes

place among the same countries. In the NAFTA area

(USA, Canada and Mexico), about 28% of foreign

furniture trade is among the three countries. In the Asia

and Pacific region about 38% of total foreign furniture

trade is within the region.

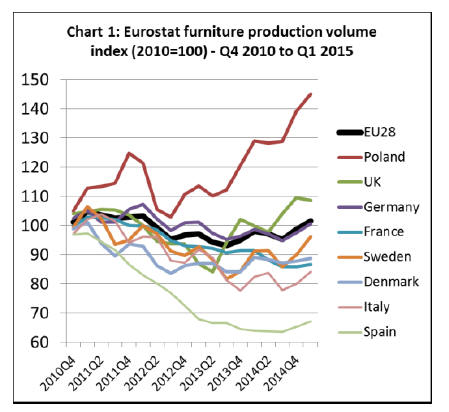

Upward trend in EU furniture production continues

Eurostat data shows that furniture production in the EU is

slowly recovering from the period of weakness in 2012

and 2013. The production volume index was around 1.6%

above the 2010 reference level in the first quarter of 2015,

the first time it has exceeded this level since early 2012

(Chart 1).

Europe‟s three largest furniture producing countries –

Italy, Germany, and Poland - all raised their output in

2014 and early 2015. Furniture production in Poland

increased particularly sharply last year and in the first

quarter of 2015.

In the first quarter of 2015, Polish production was 45%

higher than the 2010 reference level. The furniture edition

of the German trade newsletter EUWID reports that Polish

producers exported 78% of their output in 2014. And

around 80% of the exports went to other EU countries,

with Germany being the most important recipient,

followed by France, the Czech Republic, Belgium and the

UK.

The trend in German furniture production has been very

much in line with the overall EU trend over the last four

years. German production has been rising slowly since the

end of 2013. The German furniture industry remains

under pressure from cheaper products, especially from

Poland and China, both on the domestic market and

abroad.

However, to some extent German furniture producers are

benefiting from robust domestic construction sector and

relatively strong German consumer confidence as well as

recovery in several European export markets.

The kitchen furniture industry, for example, has seen a

positive trend in 2014 and early 2015, both on the

domestic and in various European markets. According to

the German furniture industry federation VDM, there is an

on-going trend towards higher-quality and priced kitchen

furniture in Germany.

Moreover, the export markets in the Benelux region, in

particular, rebounded last year. The positive trend for

German kitchen furniture producers has continued in the

first two months of 2015, according to EUWID, with an

increase in turnover of around 1.3%. Turnover in the

German upholstery furniture sector was stable in the first

two months of this year.

Italian furniture production dipped in mid-2014 but picked

up speed again in the last quarter of 2014 and first quarter

of 2015. EUWID reports that Italian furniture producers

booked good increases in export sales towards the end of

2014, especially in non-European countries such as the

USA, China, Saudi Arabia and the United Arab Emirates.

On the domestic market Italian furniture producers

profited from tax advantages for building renovations,

which include an extra bonus for furniture, according to

FederlegnoArredo.

EU wood furniture trade analysis

The remainder of this report contains a review of the most

recently available EU wood furniture trade data to end

March 2015. Seasonal fluctuations are a major feature of

the EU furniture trade. EU wood furniture exports are

almost exclusively interior products, mainly destined for

other western countries, which tend to rise sharply at the

end of the year in the run-up to the Christmas holiday

season.

In contrast, EU imports of wood furniture tend to be

higher in the opening months of the year. This is partly

because they contain a high proportion of exterior

products mainly imported from Asian countries in the

spring months. In addition, a relatively large proportion of

the Asian furniture imported into the EU is bought during

the January sales season.

Against this background, the following analysis of EU

furniture trade uses “12 month rolling average” data. This

is calculated for every month by averaging the monthly

imports or exports for the previous twelve months.

The data irons out seasonal variations so that potentially

significant long-term changes can be more easily

identified.

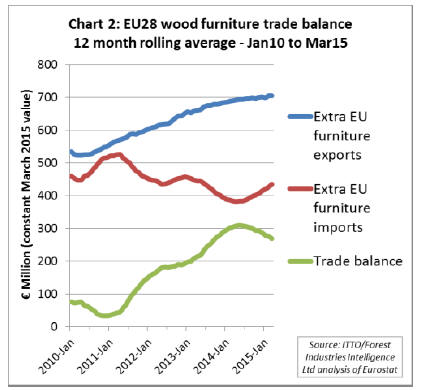

Fall in EU wood furniture trade surplus

Chart 2 illustrates the trend in EU trade balance of wood

furniture using 12 month rolling average data between

January 2010 and March 2015. It shows a steady rise in

EU wood furniture exports over the last four years,

although the rate of growth has flattened somewhat in

recent months.

On the other hand, EU wood furniture imports, which had

declined since 2011 – except for a brief interruption in

2012 – have rebounded in late 2014 and throughout the

first quarter of 2015.

This is partly due to an increase in wood furniture

deliveries from China, which had plummeted in 2013 and

recovered again in recent months. Vietnam has also

delivered more wood furniture to Europe again in the first

months of 2015.

The shift in trade balance is partly due to improved

consumption in individual EU markets, especially in

Germany and the UK, where the construction sector has

been comparatively strong in 2014 and early 2015.

Impact of EUTR

The recent downturn and subsequent recovery in deliveries

from China and Vietnam may be partly attributable to the

EU Timber Regulation (EUTR). The sharp fall occurred at

around the time the EUTR came into force in March 2013

and may have been partly due to concerns about the

reliability of evidence provided by Chinese and

Vietnamese suppliers to demonstrate negligible risk of

illegal timber origin.

Now the EUTR has been in effect for two years, more

buyers may have established reliable supply chains and

documentation and feel more confident about importing

wood furniture from outside the EU.There is some

evidence for the impact of EUTR from interviews with

large European retailers.

A recent trade article based on interviews with

representatives of European furniture manufacturer and

retailer IKEA, flooring manufacturer Kahrs, and DIY

retailer B&Q observes:

“EUTR did not require major revision of their anti-illegal

timber strategies. Illegality risk assessment and due

diligence were already integrated into their operations,

and they are also all working towards 100% certified

sustainable sourcing. What the EUTR did do, however,

was prompt renewed scrutiny and reappraisal of existing

systems and a step up in communication on illegality

risk”.

The interviewees noted that EUTR prompted an extensive

effort to tighten and extend existing procedures, gather

additional data from suppliers and to train staff but did not

generally lead to any significant change in the supply base.

The interviewees said that they had to temporarily stop

sourcing from some companies when documentation was

inadequate. However problems were almost always

resolved so that trading could resume.

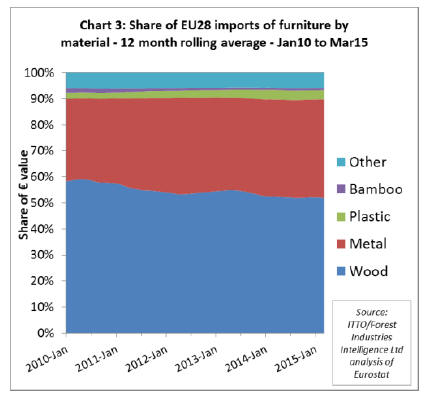

Another line of evidence for the impact of EUTR is

provided by analysis of the share wood in total furniture

imports (Chart 3). Wood‟s share of total furniture import

value fell in the second half of 2013 when EUTR was first

implemented, from around 55% to 53%.

This loss of share was at the expense of metals and, to a

lesser extent, plastic. However, wood‟s share of import

value stabilised in 2014 and 2015. In the 12 months to

March 2015, wood still accounted for 53% of furniture

import value, compared to 38% for metals, 3.5% for

plastic, 1% for bamboo and 5.5% for other materials.

Euro-dollar exchange rate influencing trade balance

An important factor in the recent euro-based increase in

EU wood furniture imports is the dramatic loss in value of

the euro against the US dollar over the last twelve months.

This has led to exchange-rate related price inflation.

The euro lost around 16% of value against the US dollar

between June 2014 and June 2015. Early this year the euro

hit a historic low, triggered by the renewed financial

troubles in Greece and the Swiss government decoupling

the franc from the euro in December 2014.

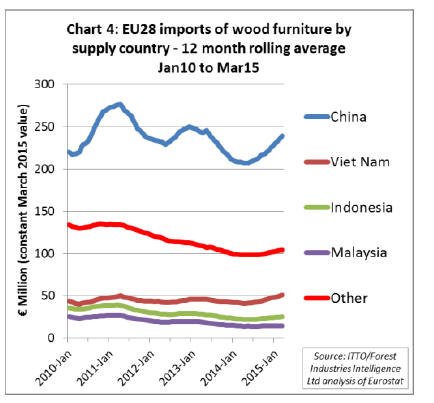

Turnaround in imports from Asia

Chart 4, which shows the trend in EU imports of wood

furniture by supply country using 12 month rolling

average data, reveals that the lasting downhill trend in

imports has turned around at the end of 2014.

This positive trend continued through the first quarter of

2015. In the first quarter of this year, Chinese wood

furniture deliveries to the EU rose by 12.4% and China

alone accounted for 55% of total imports. In the first

quarter of last year, China‟s share stood at 54%.

Vietnam and Indonesia also regained some of the ground

lost between 2011 and 2014, while deliveries from

Malaysia were stagnating. Vietnam‟s share in total imports

rose from 11% to 12 % between the first quarter of 2014

and the first quarter of this year. Indonesia‟s share was

stable at 6% while Malaysia‟s slipped from 4% to 3%.

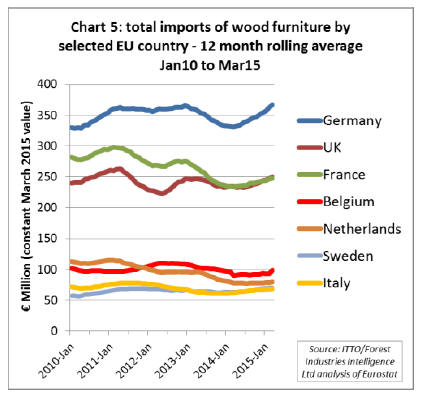

Chart 5 shows the trend in all imports of wood furniture

(from both within and outside the EU) by EU member

state using 12 month rolling average data. It indicates that

the overall downhill trend that persisted during most of the

period from 2011 to 2014 has turned around in various

member states.

The important German market went through a period of

weakness from the end of 2012 to the beginning of 2014.

However, German wood furniture imports have picked up

significantly in recent months and early 2015 volumes

exceed the previous peak in early 2012.

UK furniture imports have been relatively stable overall in

the last four years and were showing signs of

strengthening in the first quarter of 2015. Imports into

France, much affected by the financial crisis in recent

years, are also showing signs of recovery.

Among the smaller importing countries, the slow but

steady stabilisation in Italy has continued through the first

few months of 2015 and Sweden and Belgium are also

recovering slowly. However imports into the Netherlands

remain at a very low level.

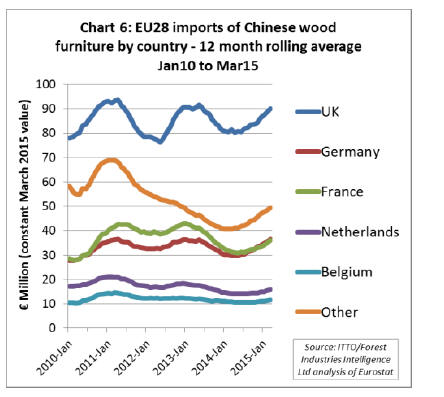

Analysis of EU member states‟ imports of Chinese wood

furniture reveals strong recovery across a wide range of

markets since mid-2014 (Chart 6).

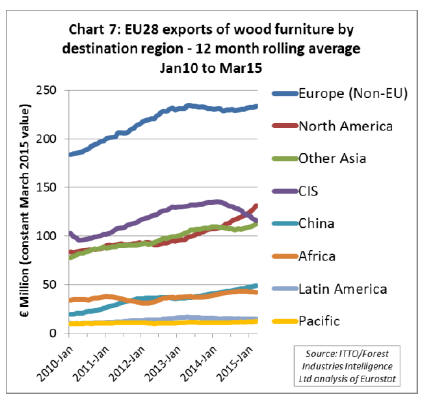

Lower EU furniture exports to CIS region

Chart 7 shows the trend between January 2010 and March

2015 in EU exports of wood furniture to non-EU countries

by destination region using 12 month rolling average data.

This reveals that the slow-down noted in growth of EU

exports to Russia and Eastern Europe from the second half

of 2013 has since turned into decline.

This reflects political tensions between the EU and Russia

in connection with the crisis in the Ukraine as well as

economic difficulties in Russia, which have been

aggravated by the political crisis.

According to an article in the German magazine Spiegel,

the World Bank expects Russian GDP to shrink by 2.7%

this year. This in turn is expected to have a significant

impact on Russian imports of consumer products from the

EU and Switzerland during the rest of 2015.

EU wood furniture exports to European countries outside

the EU were stable over the last twelve months. The same

is true for deliveries to Latin America, the Pacific region

and Africa. On the other hand, exports to North America

continued to rise sharply and deliveries to China and other

Asian countries are also increasing.

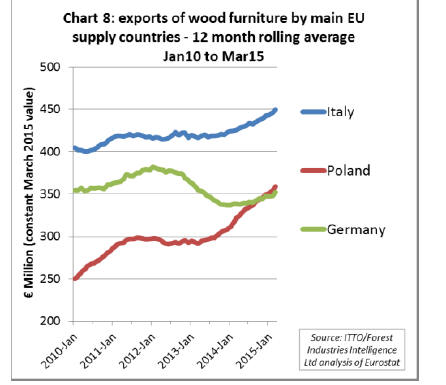

Poland closing gap on Italy the EU’s top wooden

furniture exporter

Chart 8 shows the trend in exports of wood furniture (both

within and outside the EU) by the EU‟s three largest

furniture producing countries in the period to end March

2015. Exports from Poland and Italy have performed more

strongly than those from Germany in recent years.

Italy is still by far the largest European exporter of wood

furniture but Poland has been closing the gap in the last

two years. In late 2014 Poland overtook Germany to

become Europe‟s second largest exporter of wood

furniture. However German exports have been rising since

the start of 2014 after a sharp downturn in 2012 and 2013.

Besides competitive pressure, the comparatively weak

performance of German exporters over the last few years

could also be due to the relatively strong domestic market

in Germany. Against this background, German producers

were under less pressure than Italian furniture

manufacturers, for example, to find new export

opportunities.

Exports by other EU wood furniture exporting countries

showed mixed trends (Chart 9). The sharp downward turn

in French exports registered since 2010 levelled off in

2014 and exports have since stabilised at a relatively low

level. Exports from Denmark show a slow but steady

upturn since 2013 and the country is now the fourth largest

exporter of wood furniture in the EU.

Sweden has fallen back to sixth place following a steep

decline in trade in 2013 and 2014. However Swedish

exports are now showing signs of stabilisation. The

gradual increase in wood furniture exports by Portugal and

Spain since 2012 and 2013, respectively, has continued

through 2014 and into 2015.

Lithuania

Lithuania has overtaken Sweden in the ranking of

Europe‟s largest wood furniture exporters. Lithuanian

exports more than doubled between 2010 and 2015.

According to “enterpriselithuania.com” major furniture

producers invested heavily in production expansion in the

country in the last few years. Lithuania is also a major

supplier of IKEA. Some of the loss in importance of

Sweden and the increase in importance of Lithuania may

be linked to IKEA shifting production capacities.

Romania is also growing in importance as a furniture

exporter, with average monthly exports rising around 35%

between January 2010 and March 2015. Romania benefits

from abundant quality raw material, particularly beech,

and a labour force which is relatively cheap by European

standards with a long-tradition of wood furniture

manufacturing.

Romania‟s exports are mainly destined for the EU, Russia,

and Middle East. There is also rising domestic furniture

demand in Romania, particularly in the hospitality sector.

Romania‟s manufacturers increasingly concentrate on

higher quality hardwood furniture as Chinese

manufacturers are taking a rising share of the Romanian

market for lower end furniture based on wood panels. |