|

Report

from

Europe

Signs of recovery in EU plywood market

After a period of turbulence during the years of the EU

recession, the EU plywood market has stabilised and

shown signs of recovery in the last 18 months. Supply and

prices have also become more consistent and the industry

appears to have adjusted well to the new demands of the

EUTR.

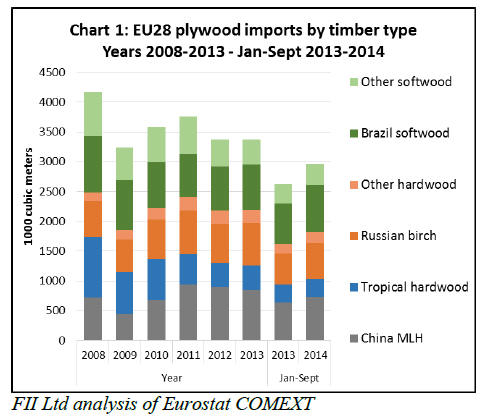

The annual trend in EU plywood imports over the last 6

years is shown in Chart 1. After a dip between 2011 and

2012, imports remained stable at 3.38 million m3 in 2013.

EU imports in the first nine months of 2014 were 2.96

million m3, 12% more than the same the previous year

(Chart 1).

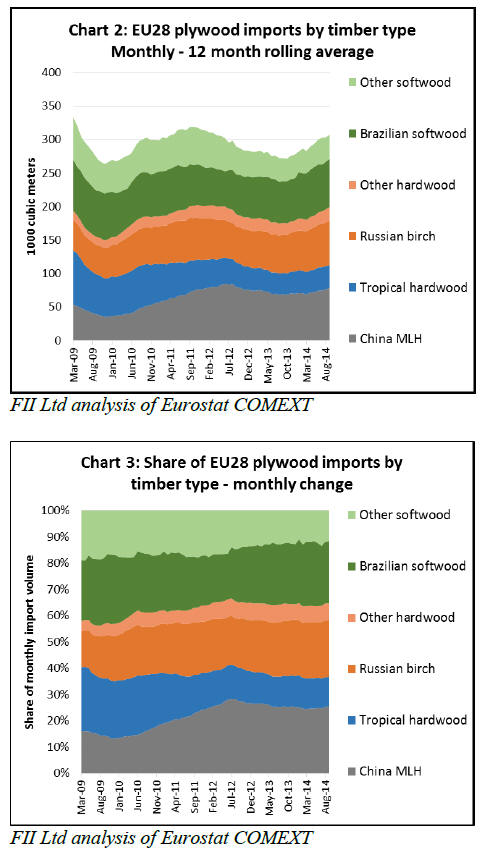

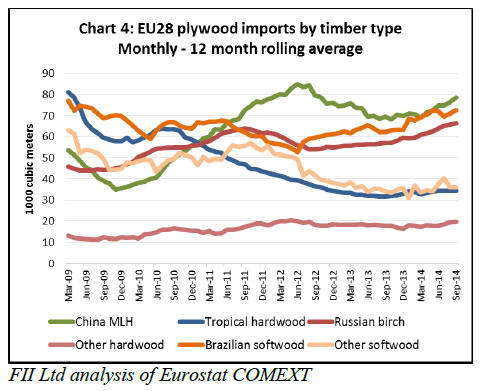

Charts 2 to 4 show the monthly trend in plywood import

volume into the EU to September 2014 using 12 month

rolling averages. This is calculated for each month as the

average monthly import of the previous 12 months. The

data removes short-term fluctuations due to seasonal

changes in supply and shipping schedules and provides a

clear indication of real changes in consumption.

Chart 2 shows that EU plywood imports declined between

September 2011 and October 2013 but recovered

continuously in the 12 months between September 2013

and September 2014. Chart 3 highlights that the share of

different types of plywood in the EU market was quite

stable in the period between July 2012 and September

2014.

This contrasts with the period of import growth between

January 2010 and June 2012 when Chinese Mixed Light

Hardwood (MLH) plywood and Russian birch plywood

rapidly gained share, primarily at the expense of tropical

hardwood plywood and softwood plywood.

Impact of EUTR

The relative stability in share between different plywood

types over the last two years coincides with the timing for

introduction of the EU Timber Regulation (EUTR) in

March 2013. There was much speculation in advance of

this measure that it might impact particularly heavily on

the plywood sector.

It was assumed that difficulties in obtaining reliable

assurances of legality in the complex supply chains that

prevail in China‟s plywood sector might lead to a loss of

share. Beneficiaries were expected to be domestic

suppliers and tropical countries with simpler supply chains

and where far-reaching steps were being taken to

implement third party certification or legality verification

systems.

The fact that EU plywood imports from tropical countries

has at least stabilised over the last 2 years may be partly

attributable to these efforts in combination with the EUTR.

Plywood exported into the EU from Malaysia is mostly

certified to the MTCS, imports from Indonesia are

certified to the SVLK, while those from Gabon are

primarily FSC certified.

At the same time, the EU import data indicates that a

significant number of Chinese suppliers have been able to

adapt to the new demands of the EUTR – either by

switching to locally produced face veneers – such as

poplar – or by sourcing tropical veneers from certified or

otherwise known legal sources.

This assumes that measures by EU countries to implement

the regulation have been sufficiently rigorous to change

behaviour. Regular contacts with EUTR Competent

Authorities and EU trade associations suggest that there

have been far-reaching EUTR implementation measures in

most of the largest plywood importing countries –

particularly in the UK and Germany.

Anecdotal reports in the European timber trade press also

highlight the growing emphasis on legality verification in

the EU plywood sector and the effect this is having on

supply chains.

Changing plywood market share

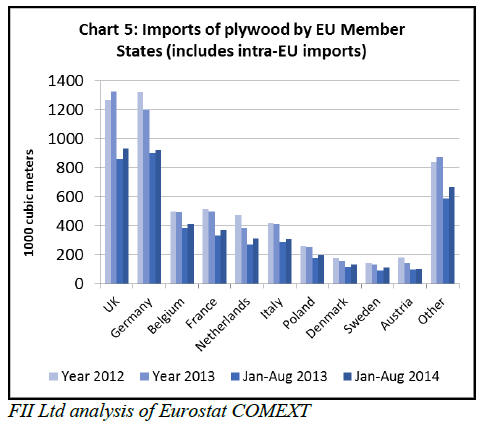

Chart 4 shows how trends in EU plywood import trade

have varied very widely between different products types

over the last four years. It highlights how tropical

hardwood plywood imports fell continuously from June

2010 to June 2013, losing share to Chinese MLH, Russian

birch and other temperate hardwood products (particularly

from Ukraine, Belarus, and Uruguay) at that time.

EU imports of Chinese MLH plywood rose sharply in the

period between November 2009 and June 2012 and then

subsided for the next 18 months as the much anticipated

recovery in European construction continued to be

delayed.

The EU rise in imports of Russian birch peaked much

earlier, in June 2011, but then subsided more slowly. In

the softwood plywood sector, Brazil lost share to other

suppliers in the period 2009 to June 2012, but has been

regaining share ever since.

Chart 4 also shows that there has been an upward trend in

imports in all plywood products types during 2014. The

pace of increase in imports this year has been particularly

rapid for Chinese MLH, Brazilian softwood and Russian

birch plywood.

Chart 5 shows that plywood imports have risen into all the

main EU markets during 2014, with particularly strong

growth in the UK.

Strong UK plywood demand

Rising plywood imports into the UK in 2014 are due both

to higher levels of construction activity and to

improvements in the supply side. UK importers report that

Chinese MLH plywood has been readily available this

year at stable prices.

Orders in the last quarter of 2014 could be shipped from

China within around four weeks. However quality

consistency remains an issue for some UK buyers of

Chinese plywood. Freight rate volatility has also been a

problem again this year. Rates tend to rise at the start of

each month and then decline sharply as shipping

companies fail to fill available space.

While plywood imports into Germany were strong in the

opening months of 2014, the market showed signs of

weakness in the second half of the year. This was

primarily due to the recent downturn in the Germany

economy. Imports have also been hindered by the German

customs decision to reclassify much of the plywood

imported from China as laminated wood.

Technically these two products are distinguished by the

direction of grain in alternate veneer layers – in plywood

the grain is crossed at right angles whereas in laminated

wood it is parallel. Plywood attracts a duty of only 7%

while laminated wood attracts a duty of 10%. In the

absence of reliable assurances that only products glued

crosswise are supplied by Chinese suppliers, some

German importers are switching back to alternative

products including European birch and softwood plywood.

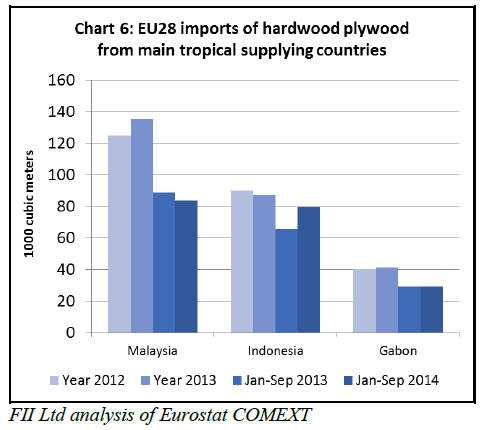

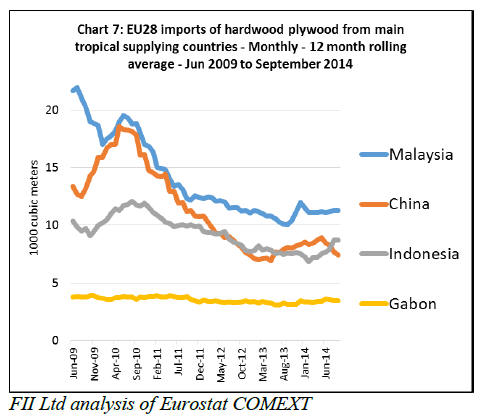

Stabilisation of tropical plywood imports

Charts 6 and 7 show how the downward trend in imports

of tropical hardwood plywood into the EU has stabilised

and even shown slight signs of recovery in 2014. Imports

from Malaysia rose sharply at the end of 2013 to beat the

increase in GSP duty from 1 January 2014 and fell away

sharply in January and February.

However they then stabilised at a slightly higher level than

the previous year in each of the 7 months from March

through to September 2014. For the full January to

September 2014 period, EU imports of Malaysian

hardwood plywood were 83,600 m3, 6% less than the

same period in 2013.

Imports from Indonesia also fell in the first two months of

2014, but then increased between March and August 2014.

In total for the first nine months of 2014, EU imports of

Indonesian hardwood plywood were 79,500 m3, 22%

more than the same period in 2013.

European imports from Indonesia have been boosted this

year by resumption of regular break bulk services in

response to volatile container freight rates. Constraints on

log supply and firm demand for Indonesian plywood in

Japan and the Middle East mean that prices for Indonesian

plywood are still too high for many European importers.

However there is consistent demand from that sector of the

market willing to pay premium prices for the quality

advantages offered by Indonesian product. European

importers report that prices for Indonesian plywood have

been steady during the second half of 2014, with only

slight price increases for specific grades of filmed

plywood.

Chart 7 highlights that EU imports of okoume plywood

from Gabon have remained low but consistent over the last

3 years. Imports from Gabon are around 3200 m3 to 3400

m3 each month with very little variation during the last 4

years. Total EU imports of plywood from Gabon in the

first 9 months of 2014 were 29,000 m3, exactly equivalent

to the same period the previous year. Much of this product

is believed to be FSC certified and derived from one large

European-owned operation in Gabon.

Okoume plywood market challenges

Despite the consistency in supply, Europe‟s market for

okoume plywood continues to suffer from weak demand.

There were early signs of improving construction and

economic activity in the first half of 2014 in the two key

markets for this product – France and the Netherlands.

However, activity and market confidence weakened again

in the second half of the year.

Since the change in Gabon‟s GSP status on 1 January

2014, plywood imported into the EU from Gabon has

attracted a 7% duty. However manufacturers of okoume

plywood in Europe have been granted an exemption and

pay no duty on okoume veneer imported from Gabon.

Even with this advantage, there is little sign of an upturn

in market demand for European produced okoume

plywood. Producers continue to report very low

profitability but are struggling to push through price

increases in the current market. The simple fact is that

Europe‟s few remaining tropical hardwood plywood

manufacturers are uncompetitive relative to overseas

suppliers.

Slight rise in tropical hardwood plywood imports from

China

Chart 7 shows that EU imports of Chinese plywood faced

with tropical hardwood were rising between April 2013

and May 2014. This seems to contradict anecdotal reports

suggesting that imposition of the EUTR from March 2013

had encouraged a partial switch away from tropical

hardwood face veneers in plywood supplied into the EU

from China.

It‟s likely that many EU importers had already made the

switch away from tropical hardwood in Chinese plywood

in advance of the March 2013 deadline. It‟s also possible

that Chinese manufacturers were being successful in

sourcing sufficient volumes of legally verified tropical

face veneers to service their European clients. However,

the slow rising trend in EU imports of tropical hardwood

plywood had reversed again by June 2014.

Russian birch plywood readily available

In the first nine months of 2014, EU imports of Russian

birch plywood were 604,000 m3, 16% more than the same

period in 2013. Demand has been particularly good in the

UK. Supplies have also been readily available.

In the last quarter 2014, lead times between ordering and

delivery into the EU were no more than around 4 weeks on

average. There is particularly good availability of filmed

plywood grades as domestic demand for this product in

Russia was weakening towards the end of the year with

the early onset of winter.

Prospects for supply in 2015 are also good with no

shortages of log supplies and the colder conditions now

prevailing in Russia expected to allow an early start to the

harvesting season.

EU domestic plywood production

The EU does not have a large domestic plywood sector,

mainly because it lacks supplies of large diameter logs

required for plywood manufacture, and production has

declined in recent years. Nevertheless the domestic

industry is still an important competitor for imported

plywood.

Latest Eurostat data shows that EU plywood production

was 3.81 million m3 in 2013, down from 4.16 million m3

in 2012 and a high of 4.55 million m3 in 2007. Each year

domestic production contributes between 50% and 55% of

the volume of plywood supplied to the EU, a proportion

that hardly changed during the decade to 2013.

Most large EU plywood manufacturers are based in

Sweden and Finland and use softwood and birch. There

are a range of smaller plywood manufacturers in southern

parts of the continent utilising temperate species such as

poplar and beech.

Delayed recovery in European construction

Future prospects for plywood market growth in Europe are

likely to be dampened by only slow recovery in the

European construction sector. The latest forecast issued by

the research organisation Euroconstruct at their November

2014 Conference suggests a slower return to growth than

forecast at their June 2014 Conference.

Euroconstruct note that after seven years of deep crisis,

during which the market lost 21% in volume, 2014 is

expected to be the first year of recovery in European

construction output. However growth this year is not

expected to exceed 1%, rising to 2.1% in 2015 and 2.2%

in the following two-year period.

The recovery has been gaining momentum in the UK and

other northern European countries outside the Eurozone.

Eastern European economies have also returned to robust

growth after a sharp slowdown in 2012-2013.

However in the Eurozone in Western Europe, Italy

remains in recession while economic problems are also

mounting in other countries. Output, wages and prices are

stagnating and levels of unemployment are at record highs

after four years of general austerity measures.

Overall economic growth is expected to remain weak,

particularly as the credit market is still very tight and the

public accounts correction is still underway. Concerns

over the risk of deflation in the Eurozone are also

mounting.

According to Euroconstruct‟s new estimates, all three

main segments within the construction market are

expected to grow slowly in the short-to-medium term. The

residential sector is still suffering. This is especially true

of new construction which, after a further 4% reduction

last year, is only expected to grow 0.1% in 2014.

However, in the medium term this sector is expected to be

the main engine for recovery. Growth in residential

construction across Europe is expected to average around

4% per year during the period 2015 to 2017. During this

period new non-residential construction is forecast to grow

by only 2% per year. Civil engineering is expected to grow

on average 2.5% per year over the next three years.

Renovation was more stable than other sectors during the

recession and levels of activity in this sector should at

least be maintained.

Construction activity is expected to grow most rapidly in

Eastern Europe over the next three years, partly driven by

increased spending of EU project funds on infra-structure.

Construction activity in France, Italy and Spain has shown

no increase in 2014. Growth in Germany is also slowing

and there are even concerns that German construction

activity could start to decline within the next two years. In

contrast, the UK is set for very strong growth.

UK residential construction is booming again (+16% new

investment in 2014) and non-residential construction is

expected to be boosted by strong demand for commercial,

industrial and educational building. New civil engineering

works are also expected to grow in the UK (+4.5%

forecast in the two-year period 2015-2016).

* The market information above has been generously provided

by the Chinese Forest Products Index Mechanism (FPI)

|