|

Report

from

Europe

Euroconstruct raises annual construction growth

forecast to 1.8%

According to the latest half-yearly report issued in June

2014 by the Euroconstruct research agency, aggregated

construction output for the EU countries fell by 2.7% in

real terms in 2013 to the lowest level in 20 years (at

constant prices).

However, Euroconstruct report that the European

construction market hit bottom last year and forecast

average growth of 1.8% per year between 2014 and 2016.

This new growth rate forecast is 0.2% greater than the

previous Euroconstruct forecast in November 2013.

The rate of recovery projected by Euroconstruct is slow

given the extent of the decline in construction value in

recent years. It implies that output and capacity utilization

in the European construction sector as a whole will remain

at near-depression levels. High unemployment and debt,

low investment, tight credit, and financial fragmentation in

the Euro area will continue to dampen demand.

Europe's construction sector remains globally

significant

Even though construction growth is slow, with total value

of nearly €1.3 trillion in 2013, Europe's construction sector

remains globally significant and a very large consumer of

wood and other materials.

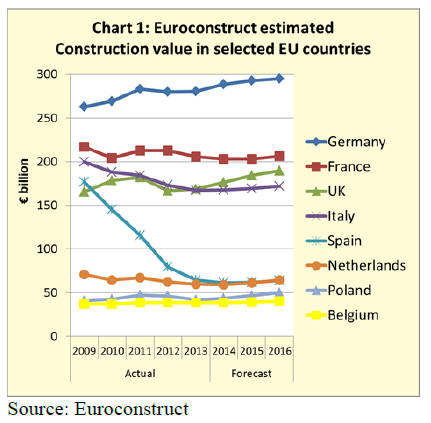

Growth in construction will vary widely between EU

countries (Chart 1). The German construction sector has

grown consistently over the last five years and is now by

far the largest in Europe. The upward trend in German

construction is expected to continue between 2014 and

2016.

Construction activity in France has been sliding since

2012 but is forecast to hit bottom in 2014 and stabilise in

2015.

Construction activity in the UK began to rebound last year

and is forecast to continue to recover well between 2014

and 2016.

Poland, Ireland, Denmark and Hungary are also among the

fast growing construction markets, all with average growth

rates expected to exceed 4% per year.

In contrast, construction output looks set to remain below

2013 levels in Spain and the Czech Republic.

Much of the growth in European construction will be

concentrated in new residential construction, but the

gradual recovery should feed through into all sub sectors.

New residential construction in total is expected to grow

by 3.2% a year between 2014 and 2016.

However residential renovation and maintenance (R&M)

is expected to grow by only 1.2% a year. This will reduce

average growth in total residential construction to 2% a

year in real terms.

Although most EU countries are clear of recession,

sluggish domestic demand growth and weak public sector

finances are likely to dampen non-residential construction

for some time. Euroconstruct expect total non-residential

construction on average to increase by 1.5% a year

between 2014 and 2016 in real terms, an upward revision

of 0.3% from the November 2013 forecast.

Total civil engineering works is now expected to grow by

1.9% a year between 2014 and 2016 in real terms,

compared to 1.5% in the previous forecast. The adjustment

is mainly a result of a brighter outlook for new civil

engineering.

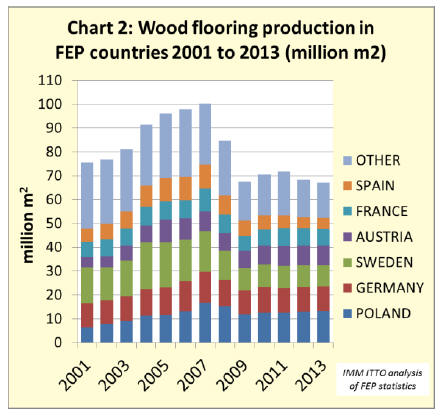

European ’real wood’ flooring production down 1.8% in

2013

Production of „real wood‟ flooring 1 in the 17 countries

covered by FEP2, the European wood flooring association,

declined by 1.8% to 67.03 million m2 in 2013 (Chart 2).

FEP estimate that total production in Europe, including

both FEP and non-FEP countries, was just over 77 million

sq.m in 2013. These figures were released by FEP at their

annual meeting in Malaga, Spain, in June.

1 The term „real wood‟ flooring is used to denote products

with a real wood face veneer which are identified

specifically as wood flooring in the trade product codes.

These products are distinct from laminated flooring which

are considered separately in this report.

2 Austria, Belgium, Czech Republic, Denmark, Finland,

France, Germany, Hungary, Italy, Netherlands, Norway,

Poland, Romania, Slovakia, Spain, Sweden and

Switzerland.

Production in Poland, Europe‟s largest wood flooring

manufacturing country, increased 2.5% to 13.28 million

sq.m in 2013. Poland now accounts for nearly 20% of all

production in FEP countries.

Production in Germany, the second largest European

manufacturing country, remained stable at 10.4 million m2

between 2012 and 2013.

However production in Sweden, the third largest

manufacturing country, declined 3.3% to 8.78 million

sq.m in 2013. There was also a 5.8% fall in production in

France to 6.9 million sq.m.

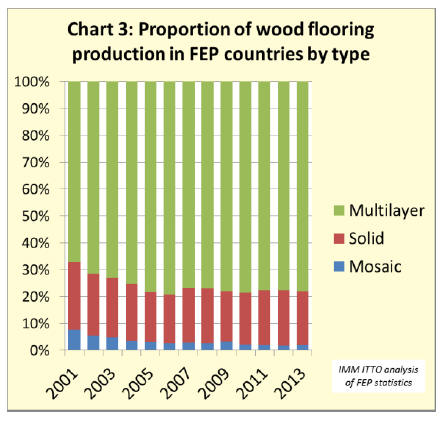

There was no change in the proportion of real wood

flooring production by product type between 2012 and

2013 (Chart 3). In both years, multilayer flooring

accounted for 78% of production, solid wood for 20% of

production and mosaic wood flooring for only 2% of

production.

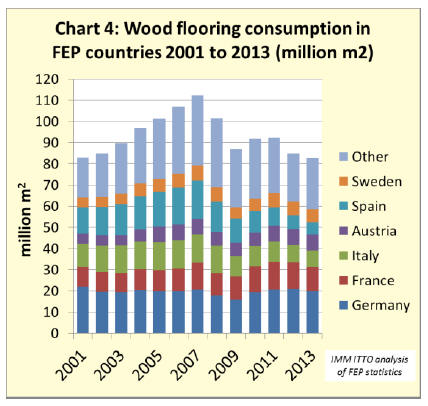

Consumption of real wood flooring in FEP countries

declined 2.6% to 82.68 million sq.m in 2013 (Chart 4).

Consumption in all the leading European markets was

falling last year.

Consumption was down 6% to 19.8 million m2 in

Germany, down 7% to 11.6 million m2 in France, and

down 5% to 7.8 million m2 in Italy.

However these losses were partially offset by rising

consumption in Austria, Denmark, Finland, Norway,

Switzerland, and Romania.

Consumption of real wood flooring per inhabitant

throughout the FEP area fell slightly from 0.22 sq.m in

2012 to 0.21 sq.m in 2013. Per capita consumption is now

highest in Switzerland (0.79 sq.m), followed by Austria

(0.77 sq.m) and Sweden (0.65 sq.m).

In contrast, per capita consumption was no more than 0.05

sq.m in Netherlands and Hungary.

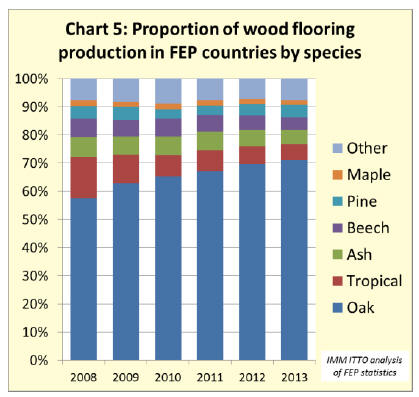

The dominance of oak in European real wood flooring

production continued to rise last year, while tropical wood

lost more ground (Chart 5). In 2013, oak accounted for

70.9% of wood flooring production in FEP countries, up

from 69.6% in 2012.

The share of tropical wood fell from 6.2% to 5.8% last

year. The share of ash (5.1%), beech (4.6%) and maple

(1.6%) were all slightly lower in 2013 than in the previous

year. However, the share of pine increased from 4.1% in

2012 to 4.4% in 2013.

At their June meeting, members of FEP reported that the

outlook for real wood flooring in Europe has improved in

2014 after nearly seven years of lingering economic and

financial crisis.

The positive trends that have emerged in northern Europe

at last seem to be filtering through into southern Europe

which was traditionally a large market for wood flooring.

However, members of FEP expressed concern about

continuing lack of access to credit following the financial

crises, particularly amongst small and medium-sized

companies that dominate the wood flooring sector.

Slowdown in rate of increase in EU wood flooring

exports

EU exports of real wood flooring have been rising in

recent years as European manufacturers focused on

diversifying overseas markets in the face of weak

domestic demand.

In 2013, around 25% of all real wood flooring

manufactured in the EU was exported to non-EU

countries. However the pace of increase in exports slowed

in the first four months of 2014 with a slowdown in

economic growth and political problems in several major

external markets.

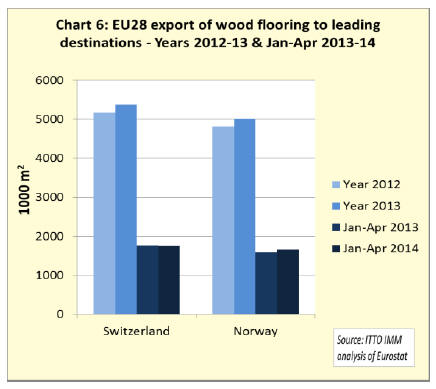

Total EU exports of wood flooring increased 4.7% to

17.78 million m2 between 2012 and 2013. There was

growth in exports to Switzerland and Norway, by far the

largest export destinations (Chart 6).

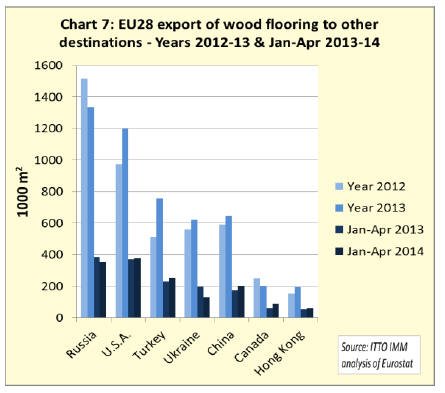

However there was also significant growth in exports to

USA, Turkey, Ukraine, China and Hong Kong in 2013

(Chart 7).

Between January and April 2014, the EU exported 5.64

million m2 of wood flooring, 1.3% more than the same

period in 2013. This year exports have continued to rise

strongly to Norway, Turkey, China and Hong Kong.

However the rate of export growth has slowed to the USA,

while exports to Switzerland and Ukraine have been

declining in 2014. Exports to Russia began to decline in

2013 and this trend has continued in 2014.

Partial recovery in EU wood flooring imports from

China

Imports of „real wood‟ flooring from outside the EU

supply around 22% of total consumption throughout the

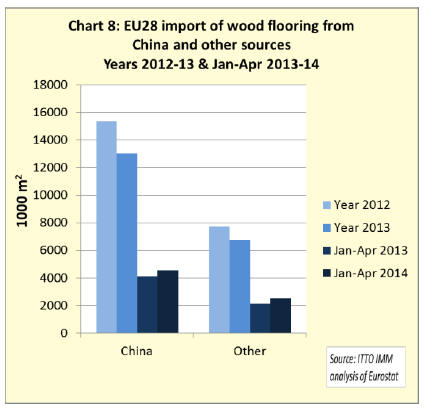

region. EU imports of real wood flooring declined 14%

from 23.1 million m2 in 2012 to 19.8 million m2 in 2013.

Imports from China, by far the largest external supplier,

fell 15% from 15.4 million m2 in 2012 to 13.0 million m2

in 2013 (Chart 8).

This was due to the combined effects of very slow

construction activity and consumer demand in Europe,

competition from Europe‟s domestic manufacturers and

alternative flooring products, rising costs in overseas

manufacturing locations, and diversion of supply to more

dynamic emerging markets.

However EU imports of real wood flooring have been

rising again this year. Between January and April 2014,

the EU imported 7.1 million m2 of real wood flooring,

13.2% up on the same period in 2013.

Imports from China were 4.6 million m2 in the first four

months of 2014, 11% more than in the same period the

previous year.

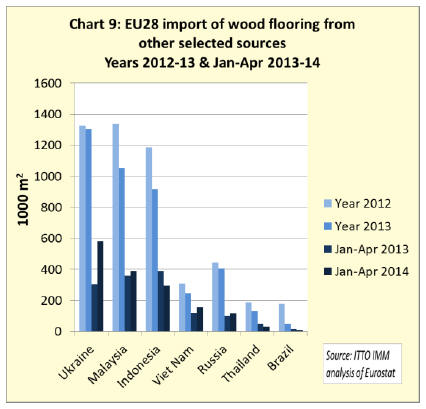

Imports have also risen from Ukraine, Malaysia, Vietnam

and Russia this year. Imports from Indonesia and Thailand

have continued to decline (Chart 9).

European laminate flooring manufacturers report slow

recovery

Europe‟s laminate flooring sector, while still dominant in

global terms, came under considerable pressure during the

global financial crises. Declining consumption combined

with overcapacity and overseas competition, particularly

from China, led to a sharp fall in prices.

This meant that retailers had to shift huge volumes of

laminate flooring in order to profit from sales. As a result

distributors have been turning to higher margin products

such as Luxury Vinyl Tiles (LVT) which are seen to offer

a better combination of quality, value and margin.

The European laminate flooring industry has responded

partly through down-sizing and partly through

development of new higher value product lines. It has also

focused marketing efforts on the specific performance and

environmental benefits of laminate flooring and on the

quality credentials of European manufacturers.

Partly as a result of these efforts, Europe‟s laminate

flooring market has become increasingly diversified. Low

end products are still available at retail prices of less than

€10 per m2. These contrast with upscale products offering

some combination of long-life guarantee, bevelled edges,

handscraping, wire brushing and exotic designs which

might be priced in excess of €25 per sq.m.

The industry‟s marketing effort has been co-ordinated by

the Association of European Producers of Laminate

Flooring (EPLF) which this year incorporated the slogan

“Quality and Innovation made in Europe” into the

association logo.

EPLF's members currently consist of 21 manufacturers

from 11 European countries. The EPLF manufacturers

supply approximately 55% of the global laminate flooring

market and over 80% of the European market.

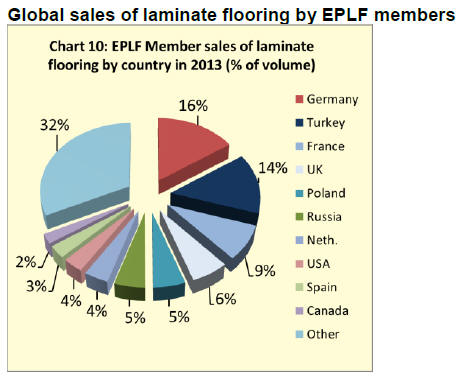

Germany is hugely dominant in the sector in Europe,

accounting for around 50% of production by EPLF

members in 2013. The second largest producer amongst

EPLF members is Turkey accounting for 15% of

production.

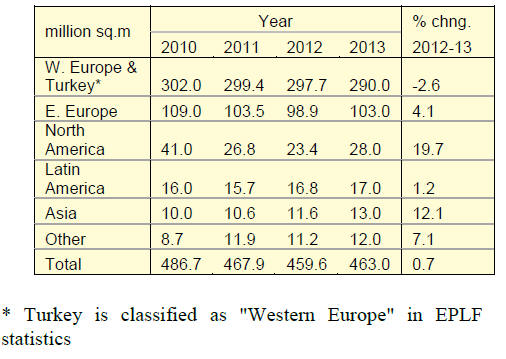

According to the latest EPLF annual report, the European

market for laminate flooring has stabilised and is just

beginning to show signs of recovery. Sales of laminate

flooring by EPLF member companies increased 0.7%

from 460m sq.m in 2012 to 463m sq.m in 2013.

Although sales declined in Western Europe and Turkey in

2013, there were gains in other regional markets (see

table).

Sales of laminate flooring in Germany, the largest single

European market for laminate flooring, fell from 76

million sq.m in 2012 to 72 million sq.m in 2013. Sales in

Turkey, the second largest market, declined from 66

million sq.m in 2012 to 65 million sq.m in 2013.

France also saw a slight decline from 40 million sq.m in

2012 to 39m sq.m in 2013. Sales to the UK were stable at

29 million sq.m in 2012 and 2013.

EPLF member sales increased in Eastern Europe in 2013.

Poland was the largest market for laminate flooring in the

region, with sales rising from 24 million sq.m in 2012 to

25 million sq.m in 2013. Sales also increased in Russia,

Romania and Ukraine last year.

As recently as 2011, North America experienced a

dramatic slump in sales of laminate flooring due to the

challenging economic situation in the USA. Sales dropped

from 41 million sq.m in 2010 to 27 million sq.m in 2011

and then to only 23 million sq.m in 2012.

In 2013, North American sales picked up once more,

rising to 28 million sq.m. Sales in the USA increased from

12 million sq.m in 2012 to 16 million sq.m in 2013. Sales

in Canada remained stable at 11 million sq.m in both 2012

and 2013.

Tough competition from Asia‟s domestic manufacturers

has meant that sales of European laminate flooring to the

region have been limited to date. European sales are

focused on higher value premium products. European

sales throughout Asia increased from 11.6 million sq.m in

2012 to 13 million sq.m in 2013.

European sales of laminate flooring in China, including

Hong Kong, increased from 3 million sq.m in 2012 to 4

million sq.m in 2013.

The volume is very small compared with the overall size

of the Chinese market which is believed to consume in

excess of 250 million sq.m of laminate flooring each year.

Challenges to European laminate flooring in Turkey

and Russia

EPLF members report a slight upward trend in total

European sales of laminate flooring in the first half of

2014.

However political issues are now creating concerns about

future prospects in Turkey and Russia which have been

key growth markets for laminate flooring in recent years.

Sales of European laminate flooring in Turkey weakened

in the first half of this year. This was partly driven by a big

fall in the value of the lira-euro exchange rate. However it

may also be a consequence of Turkey's decision in

December 2013 to start anti-dumping procedures against

German laminate flooring producers.

The decision follows complaints by Turkish flooring

producers that German manufacturers have been selling at

below production cost in Turkey. German manufacturers

have responded that their costs are lower than Turkish

competitors because they have more efficient raw material

supply chains. The Turkish government is still

investigating and has yet to publish a final decision.

EPLF members also report challenges in the Russian

market this year. Apart from the potential political fall-out

from recent events in Ukraine, European laminate flooring

manufacturers allege widespread counterfeiting of their

products in the Russian market.

EPLF claim that in Russia “the high proportion of inferiorquality

and incorrectly-declared goods imported from Asia

makes things difficult for EPLF manufacturers as it tends

to cause lasting damage to the image of laminate

flooring”. To counter this threat, EPLF has established a

"Russia task force" to work directly with Russian trade

associations and retailers to raise awareness of quality

standards and put in place procedures for brand protection.

European laminate flooring follows fashion for oak and

rusticity

EPLF report that "rusticity" remains the key theme in

current laminate flooring ranges in Europe. The rustic

"used look" appears in several varieties of products, from

construction timber styles with imitation cement traces, to

flooring that feels brushed, planed or freshly sanded.

Ultra-modern synchro-pore printing now enables more

authentic transfer of a wide variety of structures, from fine

veins and pores to deep, distinctive knots. There is still a

strong preference for larger and wider sized boards.

Oak continues to dominate wood decors with its wideranging

decorative potential, from white-washed to

smoked. However floors with the appearance of

delicately-grained ash, walnut or elm, or rich softwoods

such as spruce and larch, are also rapidly gaining in

popularity.

A considerable amount of laminate wood decor no longer

appears in its "natural" version, but rather with a discreet

white or grey haze.

Dark colours have seen a slight decline, with the new

floors of European laminate manufacturers instead

presenting a varied spectrum of natural grey and beige

tones.

This follows a trend that originated in the wider field of

interior decoration.

* The market information above has been generously provided by the

Chinese Forest Products Index Mechanism (FPI)

|