|

Report

from

Europe

European wood window market stabilised in 2010

After a major downturn in 2009, the European window

market stabilised at a low level in 2010. Wood’s share of

the overall market continues to increase. These trends are

expected to continue in 2011 due to continuing

refurbishment of windows to improve energy efficiency

across the EU. These are the results of a study carried out

by the Fenster + Fassade trade association (VFF) with the

support of Professor Dirk Hass of the

KünzelsauerInstitutfür Marketing (KIM), which was

presented at BAU 2011 in Munich.

The study reports that the overall European window

market grew by 0.4% to 125.8 million window units in

2010 (one window unit equates to 1.69 square metres).

This follows a dramatic decline of 22.4% in 2009. Of the

125.8 million window units produced in Europe during

2010, 75 million (59.6%) were in the 27 EU member

countries, 19.8 million (15.7%) in Norway, Switzerland

and Turkey, and 31 million (24.7%) in Russia and the

Ukraine.

The 0.4% increase in the European market in 2010 is

largely attributed to the market recovery in Russia and

Ukraine. After a collapse of 49.4% in 2009, the total

market in these countries grew by 21.4% last year. In

contrast, the market across the 27 EU states decreased by

6.6% in 2010 following a 10.9% decrease in 2009.

The overall decline in the EU market masks considerable

national variations. The German market has been the most

dynamic over the last two years seeing demand rise by

3.3% in 2009 and by 4.9% in 2010. This is largely due to

government support for installation of energy efficient

windows as part of Federal Government measures to

stimulate the national economy. However, government

support will be significantly lower in 2011 and the growth

in German window demand is expected to slow. With 12.6

million window units installed last year, Germany was thelargest single

window market in Europe during 2010 accounting for 16.8% of the EU

market and 10% of the

wider European market.

Other than Germany, Poland was the only growth market

for windows amongst the nine largest European countries.

A total of 6.36 million window units were installed in

Poland last year compared to 6.23 million in 2009. The

Polish market is expected to continue to grow in 2011.

Of all European countries, Spain suffered the largest

decline in demand for windows last year. The market fell

by 35% to only 5.15 million units in 2010. This follows a

18.4% decline in 2008 and 34% decline in 2009. This a

direct response to the collapse of Spain’s construction

sector in 2008-2009.

Overall the VFF report suggests that the window market

across Europe will stabilise in 2011. Demand in Germany,

the Ukraine and Russia is expected to remain steady at last

year’s higher levels. Demand in France – where

government support for energy-efficient refurbishment is

also planned – is expected to reach at least the same level

as last year. A return to growth is expected – albeit rather

slow – in Italy and the UK after three poor years. Demand

in Turkey is also expected to increase in 2011.

Market share of wood rises in the European window sector

The VFF report includes the latest available data (year

2009) for market share of different materials. This

contains some positive news for wood. In 2009, timber

windows accounted for 18% of the total window market

across Europe compared to 17% the previous year. The

share of timber-aluminium combination products also

increased from 3% to 4% over the same period. Although

PVC lost ground compared to wood in 2009, PVC still

retains a dominant position in the overall European

window market accounting for 56% in 2009 compared to

58% in 2008. Aluminium maintained its position with

22% market share in both 2008 and 2009.

The share of timber in window usage is heavily influenced

by cultural preferences and building styles in Europe.

Timber is particularly dominant in the Scandinavian

countries, with a share of over 70% in Norway, Sweden

and Finland. However, strong energy efficiency

credentials combined with improved quality and

consistency of factory finished units has meant that market

share is gradually improving outside this area.

Across much of the rest of western, central and eastern

Europe, PVC is very dominant, benefiting from cheap

prices, consistent products and a huge marketing and

distribution network. The PVC sector has also engaged in

constant innovation to improve thermal insulation,

aesthetics and improve recycling. These factors have

contributed to PVC taking the bulk of market share in the

“emerging markets” of Europe. PVC’s share is over 70%

in Russia, Poland and Turkey.

Aluminium is not strongly favoured in residential

construction and tends to do well where commercial and

public building activity is relatively important. Aluminium

has an unusually high market share in Italy (37%),

especially in the south of the country, and in Spain (70%).

Timber–aluminium’s share is particularly strong in

Switzerland (27%).

A full copy of the VFF report (229 pages) is available for

€3500 from VFF at vff@window.de, Tel:

+49(0)699550540.

Tropical wood in the European window market

Unfortunately, advance summary information made

publicly available from the VFF report provides no details

of the relative importance of different wood types in the

European window frame market. This market has been

traditionally very important for tropical hardwoods. The

main application for meranti in north-western Europe has

been window frames – in solid form and often painted in

the Netherlands and UK, and increasingly as engineered

wood in central Europe, particularly Germany. Alongside

other uses such as doors and staircases, sapele is also used

widely for window frames in the UK, Netherlands,

Belgium and Spain. A few other tropical species are in the

same European market niche. Some, such as Brazilian and

African mahogany and Brazilian cedar, were formerly

major players but have fallen away dramatically as

commercial availability has declined. A few other species

are still used under specific circumstances, for example

African sipo, where there is willingness to pay slightly

more for better quality, and Brazilian

sapupira/angelimpedra when it can be obtained at

competitive prices or FSC certified. However volumes

involved are significantly lower than for either meranti or

sapele.

Anecdotal reports from European joinery companies

suggest that meranti and sapele continue to be favoured for

their aesthetic and technical attributes at the high end of

the window market. These two species are also commonly

held in stock by large European importers and are

therefore relatively easy to source by European

manufacturers.

On the other hand, there are also obstacles in the way of

the tropical species fully benefiting from the recent

increase in market share for wood. The environmental

issue has been a constant drag on marketing, although this

is gradually being resolved through progress on tropical

forest certification and constant lobbying and marketing

efforts, notably by the Malaysian Timber Council.

Meanwhile other challenges have emerged. Through

innovation and new product development, some

alternative wood products are already moving ahead of

tropical wood in the window sector with respect to specific

technical qualities. For example, thermally-treated wood

may conform to durability class 1 and is now regularly

offered with significantly longer life guarantees than either

sapele or meranti. This is becoming more of a problem for

tropical hardwoods now with recent expansion of thermal

treatment capacity in Europe (recently estimated by

EUWID at around 330,000 cu.m per year).

The shift to quality-controlled factory-finished window

units has also gone hand in hand with a growing

preference for engineered wood products. Tropical wood’s

earlier competitiveness built heavily on ease and

adaptability of on-site use is being gradually eroded.

Malaysian and Indonesian manufacturers have adapted to

this trend through development and supply of laminated

products, which is helping to maintain position in the

market (although recent price trends have not been

particularly favourable). Lack of production capacity for

similar engineered wood products is an increasing source

of competitive disadvantage for African suppliers in the

European wood window sector. For a species like sapele

which is quite technical to machine, expanding market

share in this sector is likely to require greater availability

of semi-finished products in standard dimensions, either

glue-lamed or in solid blocks.

Conference on climate protection with new windows

EuroWindoor is hosting a conference in Brussels on 23

March 2011 on the topic of “Climate Protection with new

Windows“. EuroWindoor is a joint European lobbying

group bringing together joinery industry associations from

the timber (FEMIB), plastic (EPW), metal (FAECF) and

glass (UEMV) sectors. EuroWindoor notes that “buildings

are responsible for more than 40% of energy consumption

in Europe and thus offer great potential for energy savings.

The conference will provide in this context figures and

information on current European developments in

technical, legal and normative aspects.” The 1-day event

will take place at the offices of the North Rhine-

Westphalia state representative to the European Union,

Rue Montoyer 47 in the European quarter of Brussels. A

complete programme and registration form with rates and

conditions is available at www.eurowindoor.org or send an

email to eurowindoor-gs@eurowindoor.org. Lectures will

be held in English.

European parquet flooring market stabilises at low level

Provisional estimates issued at the Domotex 2011 trade

fair in Hannover, Germany, by the European Parquet

Federation (FEP) indicate that parquet consumption across

the EU and European Free Trade Area (EFTA) reached

around 95 million square metres in 2010, the same level as

the previous year. These figures compare to 120 million

square metres in 2007 and 112 million square metres in

2008. FEP report positive trends in Germany and France

last year, but suggest that the Spanish market remains

weak. Figures on species utilisation for 2010 are not yet

available, but in 2009 tropical wood accounted for 10.2%

of production in a sector very heavily dominated by oak

(62% of production in 2009).

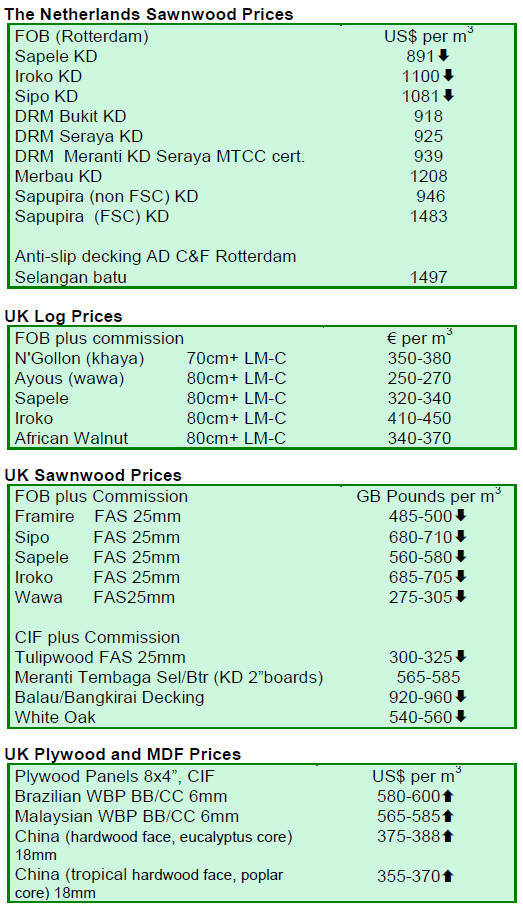

UK buyers anticipate rising plywood prices

The UK TTJ reports that talk of price rises dominates the

UK plywood market. Only a minority of traders now

believe that flat demand will take the edge off prices in the

UK as plywood exporters are pushing hard to raise FOB

rates. The pressure for higher FOB prices has been

particularly pronounced amongst Malaysian shippers keen

to cover rising log and raw material costs. Higher energy

and glue costs and labour issues are also expected to feed

through into rising hardwood plywood prices in China

after the New Year vacation.

In recent months, China has been taking an increasing

share of the UK hardwood plywood market which has

become ever more price conscious in the face of weak

consumption. According to TTJ, some importers now

believe that Malaysian products may follow in the

footsteps of Indonesian plywood and become increasingly

restricted to a small niche market. Longer term, this trend

may be countered by Malaysia’s superior ability to offer

CE-marked and environmentally certified products,

particularly once the European Illegal Timber Law (ITL)

is fully implemented from March 2013 (see below).

However, for the time-being many smaller independent

importing companies continue to buy plywood on price

with little apparent concern for either technical or

environmental standards.

Meanwhile only very small volumes of Brazilian

hardwood plywood are now entering the UK, mainly only

in larger sizes, and prices to UK buyers have risen around

10% in the last six months.

Prices for birch plywood continue to rise in the UK and

wider European market due to limited log supply and as

many traders are now carrying only low stocks. Lead

times for supply of birch plywood have been increasing.

This implies continuing opportunities for tropical

hardwood products to take a greater share of the European

market for specialist grades of film-faced plywood.

EU firmly committed to eradicating illegal wood imports

This year, the European Union is focusing heavily on

implementing and expanding the range of Voluntary

Partnership Agreements (VPAs) in support of legal

logging in major wood supplying countries. It is also

engaged in a consultation exercise to finalise

implementation regulations for the Illegal Timber Law

(ITL) which was passed into law by the EU in November

last year. These were the main messages from the

presentation by Janez Potočnik, the European

Commissioner for Environment, at the Chatham House

Illegal Logging Update meeting held in London at the end

of January.

Mr. Potočnik reported that the EU has concluded VPA

negotiations with four African countries: Ghana,

Cameroon, Congo Brazzaville and the Central African

Republic. The EU is now negotiating agreements with six

other countries: Indonesia, Vietnam, Malaysia, Liberia, the

Democratic Republic of Congo, and Gabon. The EU also

continues to receive requests for information about the

VPA process from many other countries and expects to

intensify bilateral discussions with China, Russia and

Brazil. The EU is committed to finishing VPA

negotiations with at least two more partner countries in

2011. Indonesia is likely to be among them and would be

the first to conclude a VPA in Asia.

Mr. Potočnik said that the EC will act 'without pity' in its

efforts to ensure implementation of the ITL. From the

moment the law becomes fully operational on 3 March

2013, it will be prohibited to place illegally harvested

timber on the EU market. It will also be a legal obligation

for timber traders in the EU to undertake due diligence

before placing timber on the market for the first time.

They will have to keep records of their suppliers and

customers, and make their products traceable (at least to

the extent necessary to demonstrate a negligible risk of

illegal supply). The regulation applies both to imported

and domestically harvested timber.

According to Mr. Potočnik, the regulation will have the

following consequences. Firstly, legality will become a

minimum requirement for selling timber in the EU.

Secondly, there will be a shift from high to low-risk

sources, which will favour timber from verified legal and

certified sustainable sources. Thirdly, genuine traders will

not be undercut on prices.

Svetla Atanasova, a legal expert from EC Environment

Directorate, explained that between now and March 2013,

Member States will have to develop systems for

enforcement of the ITL at national level, including

designation of competent authorities and laying down

penalties. The European Commission must also draft

supporting regulations for implementation. By 3 March

2012, the EC must finalise the product scope of the

legislation and the rules for recognition of Monitoring

Organisations. The latter are organisations like European

timber importers’ associations that will be responsible for

developing and ensuring implementation by their members

of due diligence procedures in accordance with the ITL.

By 3 June 2012, the EC must finalise detailed rules for

risk assessment and risk mitigation measures, and for the

frequency and nature of checks on Monitoring

Organisations.

In support of this process, the EC has commissioned an

external study (being undertaken by the European Forestry

Institute) to consider existing best practice for due

diligence and risk assessment. A wider stakeholder

consultation exercise is also underway and inputs from all

interested parties are now welcome. Those interested are

advised to contact:

John Bazill / Svetla Atanasova

European Commission

DG ENV.E.2 -Environmental Agreements & Trade

Tel: + 32.2.296.55.; + 32.2.299.60.93

E-mail: john.bazill@ec.europa.eu;

svetla.atanasova@ec.europa.eu

Website:

http://ec.europa.eu/environment/forests/illegal_logging.htm

Further details of the Chatham House meeting, including

copies of all presentations, are available at:

http://illegallogging.info/item_single.php?it_id=206&it=event

Related News:

|